Section 80G of the Income Tax Act, 1961 enables an assessee to claim deduction for donation made by him to certain organizations. This deduction is subject to certain conditions. The motive of Government of India behind introduction of 80G deduction is to encourage donation towards worthy causes. Under 80G, the amount donated to notified funds or institutions can be claimed as deduction at the time of filing income tax return. Only donations made to institutions registered under section 80G or to the funds prescribed therein can qualify as deduction.

Who is eligible for deduction u/s 80G?

Deduction is allowed to all the assessees (Resident or Non- Resident) who makes an eligible donation under section 80G to notified funds or institutions except for following two donations:

1. Deduction is allowed where assessee is a Resident –

In case of donation made to Clean Ganga Fund, set up by the Central Government, deduction is allowed where such assessee is a resident.

2. Deduction is allowed where assessee is a Company –

Any sum paid by the assessee, being a Company, in the previous year as donations to the Indian Olympic Association or to any other association or institution established in India, as the Central Government may specify in this behalf for –

(i) the development of infrastructure for sports and games; or

(ii) the sponsorship of sports and games, in India

How much is the deduction available?

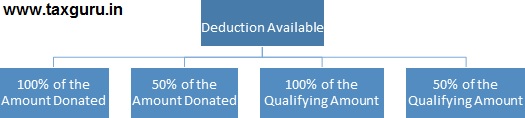

- Deduction allowed shall be 100% or 50% of the amount donated if donation has been given to any of the below mentioned institutions or funds:

| Sr. No. | Donations Eligible for Deduction | %age Deduction allowed |

| 1 | The Prime Minister’s National Relief Fund | 100% |

| 2 | The Prime Minister’s Armenia Earthquake Relief Fund | 100% |

| 3 | The Prime Minister’s Citizen Assistance And Relief in Emergency Situations Fund (PM CARES FUND) | 100% |

| 4 | The National Foundation for Communal Harmony | 100% |

| 5 | The National Defence Fund | 100% |

| 6 | The National Children’s Fund | 100% |

| 7 | The Africa Fund | 100% |

| 8 | A University or any educational institution of national eminence as may be approved by the prescribed authority in this behalf | 100% |

| 9 | The Chief Minister’s Earthquake Relief Fund, Maharashtra | 100% |

| 10 | The Andhra Pradesh Chief Minister’s Cyclone Relief Fund, 1996 | 100% |

| 11 | Any fund set up by the State Government of Gujarat for providing relief to the victims of earthquake | 100% |

| 12 | The Chief Minister’s Relief Fund | 100% |

| 13 | The Lieutenant Governor’s Relief Fund in respect of any Union territory | 100% |

| 14 | Zila Saksharta Samiti | 100% |

| 15 | The National Blood Transfusion Council | 100% |

| 16 | The State Blood Transfusion Council. | 100% |

| 17 | The National Illness Assistance Fund | 100% |

| 18 | The Army Central Welfare Fund | 100% |

| 19 | The Air Force Central Welfare Fund | 100% |

| 20 | The Indian Naval Benevolent Fund | 100% |

| 21 | The National Sports Fund | 100% |

| 22 | The National Cultural Fund | 100% |

| 23 | The Fund for Technology Development and Application | 100% |

| 24 | Any fund set up by a State Government to provide medical relief to the poor | 100% |

| 25 | The National Trust for Welfare of Persons suffering with Autism, Cerebral Palsy, Mental Retardation and Multiple Disabilities | 100% |

| 26 | Swachh Bharat Kosh | 100% |

| 27 | Clean Ganga Fund | 100% |

| 28 | National Fund for Control of Drugs | 100% |

| 29 | The Jawaharlal Nehru Memorial Fund | 50% |

| 30 | The Indira Gandhi Memorial Trust | 50% |

| 31 | The Rajiv Gandhi Foundation | 50% |

| 32 | The Prime Minister’s Drought Relief Fund | 50% |

- Deduction allowed shall be 100% or 50% of the Qualifying amount if donation has been given to other institutions or funds notified under section 80G:

If the donation has been given to any other institution or fund notified under section 80G, deduction allowed shall be 50% of the qualifying amount.

However, deduction allowed shall be 100% of the qualifying amount if the donation has been given to Government/local authority/other notified institution for the purpose of promoting family planning.

The other institutions which may be notified under this section may be charitable organisation or social organisation or religious organisation or other similar organisation.

What is Qualifying Amount?

Qualifying Amount = 10% of the adjusted gross total income or the donation (except donation to the above mentioned 32 funds) given, whichever is less.

What is Adjusted gross total income?

| Particulars | Amount |

| Gross Total Income | XXXX |

| Long term capital Gains (including LTCG u/s 112A) | (XXXX) |

| Short term capital Gains u/s 111A | (XXXX) |

| All Deduction under section 80C to 80U except section 80G | (XXXX) |

| Adjusted Gross Total Income | XXXX |

Whether to donate in cash, kind or any other mode?

- No deduction is allowed under this section, if the donation is made in kind.

- Donation of any sum upto two thousand rupees can be paid in cash or any mode other than cash.

- Donation of any sum exceeding two thousand rupees has to be paid by any mode other than cash to claim deduction.

Certificate of Donation

The Donor will receive a Certificate of Donation from the fund or institution. The certificate would be there in Form No. 10BE containing the particulars of Donee, Donor and the donation made.

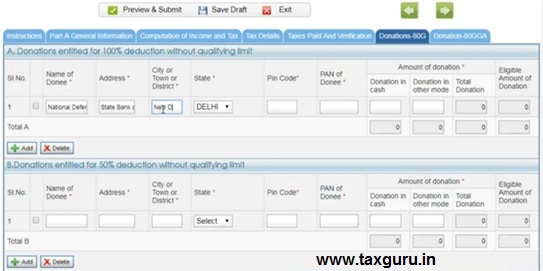

Details to be furnished while filing Income Tax Return

For claiming deduction u/s 80G, one need to submit following details in ITR:

- Name of Donee

- Address of Donee

- PAN Number of Donee

- Amount of Donation made in the relevant Financial Year

About the Author

Author is Amit Jindal, ACA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.