All Assessees are now required to file their Returns online except Super Senior Citizens are given option to submit Return in paper mode provided the Computation does not have any income chargeable under head of Profits and Gains from Business or Profession.

Changes in the ITR Requirements

The New ITR Forms have been notified vide Notification No. G.S.R. 338(E) on May 29, 2020 in exercise of the powers conferred by section 139 read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes and have made the rules further to amend the Income-tax Rules, 1962. These rules may be called the Income-tax (12th Amendment) Rules, 2020 and can be downloaded from the website of the Income Tax Department www.incometaxindia.gov.in under the head Notifications.

There are no changes in the number of forms and it’s applicability and it continues to be the same as earlier Assessment Year.

The Finance (No. 2) Act, 2019 inserted sub-section (5E) to Section 139A to allow the interchangeability of Aadhaar with PAN. The same has been implemented in the ITR’s notified. Now, the Individual person not having the PAN Number but having Aadhar Number will be able to file the Return of Income based on his Aadhar Number. The Department shall allot the PAN Number to such person in the manner prescribed. The person having Adhar Number can now apply for PAN online and the Real Time PAN Allotment by the Department has been implemented.

The Presentation covers the details and the requirements for uploading the Return of Income for AY 2021-22

Highlights

> ITR Forms have been notified vide Notification No. G.S.R. 338(E) on May 29, 2020, No Changes in the Number of Forms

> Return can be filed by using either PAN or Aadhar;

> ITR- 1 to ITR-4 can be filed using PAN or Aadhar by Individuals;

> Mandatory filing exceeding specified limit of cash deposits, foreign travel or electricity expenses;

> Time limit for claiming exemption for investments under Chapter VIA – Last date is 30thJune, 2020;

> Utility of ITR- 1 and ITR-4 released;

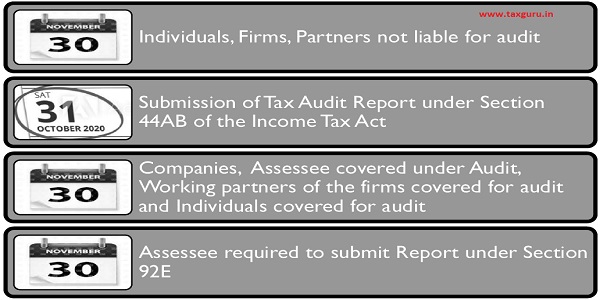

DUE DATES (AS OF NOW)

Significant Reasons for Changes in ITR

Who are exempted from e-filing

Super Senior Citizens

⇓

Not having Income from Profits & Gains of Business or Profession (Mandated from this year)

CRISP ITR-1- INDIVIDUAL & HUF (1 PAGE SIMPLIFIED FORM)

Who Can File ITR-1

- Resident Individual

- Income from Salary/Pension;

- Income from One House Property including Joint holders;

- Income from Other Sources (only positive income);

- All aggregating up to Rs. 50,00,000/-;

- Agricultural Income up to Rs. 5000/-

Who Cannot File ITR-1

- Having Dividend Income;

- Unexplained Tax Credit or Investment taxable @ 60% (Section 115BBE);

- Agriculture Income exceeding Rs. 5,000/-;

- Relief Claimed for Foreign Tax Credit;

- Having Assets/Bank Accounts out of India;

- Claiming Brought Forward Loss from earlier years;

- Individual holding Directorship in any Company;

- Individual who has Invested in Unlisted Equity Share Capital;

- Individual who has claimed deduction under Section 57 other than clause (iia);

- Individual who is assessable for whole or any part of the income on which TDS has been deducted in the hands of a person other than the assessee.

OTHER ITRS

ITR-5

- Person other than Individual, HUF, company and person filing Form ITR-7

ITR- 6

- For Companies other than companies claiming exemption under section 11

ITR-7

- Charitable Trust & Associations claiming benefit of exemption under Section 11 including such companies;

- Political Parties

- Persons including companies required to furnish return under sections 139(4A) or 139(4B) or 139(4C) or 139(4D) or 139(4E) or 139(4F)

ITR-7 (For Trust)

General Information [ITR-3,5]

certain additional details have been sought under Audit Information

![General Information [ITR-3,5]](https://taxguru.in/wp-content/uploads/2020/06/General-Information-ITR-35.jpg)

Income from Salary [ITR-1,2]

The details under Nature of Employment, Government employees have been bifurcated as Central Govt. and State Govt. employees. Also, a new option “NA”has been added to the list. This option will be beneficial for the individuals claiming Family Pension,

![Income from Salary [ITR-1,2]](https://taxguru.in/wp-content/uploads/2020/06/Income-from-Salary-ITR-12.jpg)

Income from House Property [All ITR]

In case of Let Out property to Individual, PAN or Adhar Number of the Tenant to be given.

![Income from House Property [All ITR]](https://taxguru.in/wp-content/uploads/2020/06/Income-from-House-Property-All-ITR.jpg)

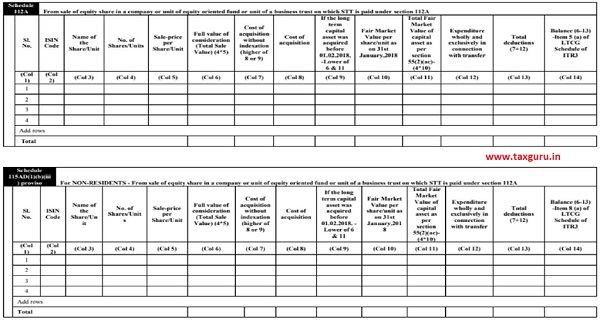

Capital Gains

Additional Reporting for Sale of Shares

Capital Gains on Sale of Property [ITR-2 TO ITR-7]

![Capital Gains on Sale of Property [ITR-2 TO ITR-7]](https://taxguru.in/wp-content/uploads/2020/06/Capital-Gains-on-Sale-of-Property-ITR-2-TO-ITR-7.jpg)

Additional Disclosure [ITR-3,5,6]

![Additional Disclosure [ITR-3,5,6]](https://taxguru.in/wp-content/uploads/2020/06/Additional-Disclosure-ITR-356.jpg)

COVID-19 Relaxations Disclosure [ALL ITR]

Schedule DI- Details of Investment”- additional statement giving the information for any investment/ deposit/ payments made during the period 01.04.2020 to 30.06.2020

Section 80D- Mediclaim [ITR- 1 TO ITR-4]

New schedule 80D inserted to calculate total eligible deduction under Section 80D for mediclaim premium with various sub heads.

Earlier 80D deduction was part of the Schedule “Part C-Deduction & Taxable Income”.

Under the new schedule assessees will now reply to the questions like:

a) Whether you or any of your family members(excluding parents) is a senior citizen?

b) Whether any of your parents is a senior citizen? and then details of premium paid under sub heads like health insurance and preventive health check up are separately asked and finally total eligible claim under Section 80D calculated.

Directorship & Shareholding Disclosure

Scope Modified [ITR-2 TO ITR-7]

SCH-PTI- Introduced [ITR2-ITR7]

![SCH-PTI- Introduced [ITR2-ITR7]](https://taxguru.in/wp-content/uploads/2020/06/SCH-PTI-Introduced-ITR2-ITR7.jpg)

Disclosure Requirements for SCHCFL [ITR-1 TO ITR-7]

![Disclosure Requirements for SCHCFL [ITR-1 TO ITR-7]](https://taxguru.in/wp-content/uploads/2020/06/Disclosure-Requirements-for-SCHCFL-ITR-1-TO-ITR-7.jpg)

Income from Life Insurance Section 115B [ITR-2 TO ITR-6]

New section “E”is added i.e. Computation of income from life insurance business referred to in section 115B

Under Computation of income from business or profession, in section “F – Intra headset off of business loss of current year”following point has been added:

Income from Life Insurance business u/s. 115B

ITR-6

- Income received from foreign company as per Section 115BD of the Income Tax Act, which is chargeable at a concessional rate, the necessary field for reporting has been incorporated in SCH-OS in ITR-6;

- Schedule SH-1 not applicable in the case of Section 8 companies and companies limited by guarantee. Start-ups are exempted from levy of Angel Tax if the conditions mentioned in DPIIT’s Notification No. GSR 127 (E) [F.NO.5 (4)/2018-SI], Dated 19-02-2019 are satisfied;

- Verifier of the Income Tax Return will now be additionally required to mention the Residential Address and the DIN Number, issued by MCA (in case of a Director).

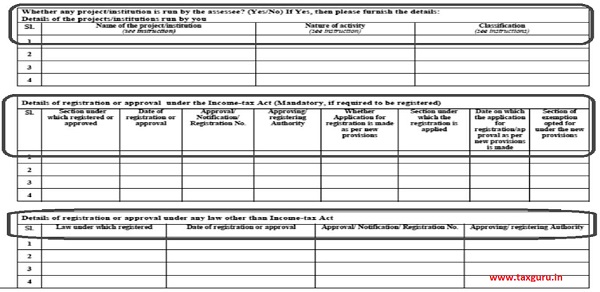

Schedule TPSA: Transfer Pricing Adjustments [ITR-3 TO ITR-7]

Changes in ITR-7

> Under basic personal information, four more declarations are added under tab

> Re-Registration of the Trust as per Finance Act, 2020, the details will be required to be given, if the Trust has done the same;

> Donation from part of Corpus etc the disclosure requirements have been enhanced

Other Changes in Fields

> Income like interest chargeable at a concessional rate on account of DTAA, the reporting of such residuary income;

> Foreign Companies reporting income from royalty or FTS are chargeable at a concessional rate.;

> If the Return is filed in response to the Notice issued by the Department, then UDIN Number is required to be quoted in the respective field;

> Companies opting for alternate Tax to select Section 1 1 5BAA and Section 115BAB;

> Section 1 1 5AB relating to taxing of units of mutual fund purchased in foreign currency by Offshore Fund at a concessional rate of 1 0%,;

> Option to select “SOP” added in ITR-5 and ITR-6 to report the property value as “NIL”;

> Reporting of disallowance under Section 40(ba) for AOP;

Removed following two points from Part B (Total Income):

- Corpus donation to other trust or institution chargeable as per Explanation 2 to section 1 1 (1)

- Deduction u/s 10AA

Added new point under Part B – Computation of tax liability on total income:

- Net tax payable on 115TD income including interest u/s 115TE (Sr.no. 12 of Schedule 115TD)

Bank Account for Refund [ITR1-ITR7]

Separate Disclosure for Bank Account in case of NRI

![Bank Account for Refund [ITR1-ITR7]](https://taxguru.in/wp-content/uploads/2020/06/Bank-Account-for-Refund-ITR1-ITR7.jpg)

Changes in Acknowledgement- ITRV

ITR V ‘Indian Income Tax Return Verification Form, without any data of the

ROI filed in Form ITR-1 (SAHAJ), ITR-2, ITR3, ITR-4 (SUGAM), ITR-5, ITR7. The Acknowledgement will state that filed but NOT verified electronically

Reasons for mistakes in calculation of Income

The accurate and complete filling up of the relevant column or detail in the Income Tax Return (ITR) form is most crucial for correct calculation of income.

In case the computation of Income or refund is different than what had been entered or what is expected, please verify the accuracy of the data entered in the ITR.

Check Points

Total Salary from all employers, irrespective of whether Form 16 has been issued or not, should be entered in Income details in ITR 1 /ITR 4S or Schedule Salary in all other ITR’s.

Interest income from fixed deposits, savings bank account etc. should be entered in Income from other Sources of ITR 1 or in Schedule OS-Income from Other Sources in all other ITR’s

CONSEQUENCES OF LATE FILING

Various Alternative Mechanisms available for e-Verification of Returns

EVC- Through Net banking

- Bank Account Linked with PAN can opt for this facility

EVC –Through Bank Account Number

- Pre-Validate your Bank Account with ITD Portal and your cell number has to be registered.

EVC –Through Demat Account Number

- Pre-Validate your Demat Account with ITD Portal and your cell number has to be registered.

EVC- Through Registered E-mail ID & Mobile Number

- Available only if your income is <= 5 lacs & Refund <= 100

EVC –Through Aadhar OTP

- Link Aadhar on ITD Portal

Avoid Last Days…

Some Useful Tips

Provisions relating to Assessments

> No adjustment under section 143(1) on account of mismatch with Form 26AS;

> No deduction of expenses even if unexplained income is determined by Assessing Officer;

> Chartered Accountants can file appeal to ITAT against the penalty order of Assessing Officer under section 271J;

> E-proceedings extended to all scrutiny assessments;

> Higher penalty for default in furnishing AIR [Section 271FA]

Stringent Action on Non-Filers

> Section 80AC introduced to extend the disallowance of deductions under Section 80H to Section RRB, if return not filed within the due date specified under Section 139(1);

> Stringent prosecution for not filing the ITR [Section 276CC

> Provides for imprisonment of up to 2 years in case a person doesn’t file the return of income;

> Exemption given if the return is furnished till end of assessment year or if the tax payable is up to Rs. 3,000- Companies excluded;

> Targets to prevent abuse of the exemption provided on the basis of amount of tax payable by shell companies or by companies holding Benami properties.

Any Further Help Required

New Call Centre Numbers

E-Assessments

Another Cause of Concern

The views stated in the material and also discussed are purely of the compiler for the discussions. It should not be used for any legal interpretation. Any decision to be taken by the user of this information is to be taken after studying the requisite provisions of the respective Act and specific applications to particular client. Neither the compiler nor the Institute will be responsible for the same. If the said information is reproduced or published in the interest of the profession, would humbly request to inform to the Compiler and the Institute about the same, before publishing the same

Compiled by CA Avinash Rawani – E-mail : avinash@carawani.com

Author Bio

I am an Australian citizen but hold OCI that says I am entitled to have all the benefits just like normal Indian citizen except voting right and holding agricultural or Farmland properties etc. Can I say that for my Tax return Form is ITR-2 with a threshold benefit of Rs.3 Lacs.Is there any specific rule for NRI?

Today I went on line through my bank to file my return. Not exactly to file but more like getting the update on all the TDS amounts showing up. The AY 21-22 was not available for selection in the drop down list.

So my question is which is the earliest date that I can file my return online?

Excellent presentation of info.

Complete, clear, logical flow…

Thanks

Really, it is very useful information for all tax payers. Thanks for your nice initiatives.

I’m a pensioner,and I have incurred a sum of more than two lakhs in foreign travel for myself and my family in FY 2019-20,which ITR should use to file my return in AY 2020-21

Dividend income is not taxable for AY 20-21, hence ITR 1 can be filed by person having dividend income.

You have mentioned that to claim exemption under 80 c (VI A) the last date is 30/06/2020. Since the last date for filing the IT returns is 30/09/2020 whether I can file the returns on 30/09/2020 which is the last date of filing the returns , since 80 C (VI A) deposit is already reported to PAO please. Clarify

Your post is very useful.You have covered all the changes made in ITRs for AY2021-2022 in a manner that any one can understand the changes made and thus avoid mistakes in filing ITR.

EXCELLENT.