Case Law Details

Smt. Mrunalini Kalagara Vs ITO (ITAT Hyderabad)

Hyderabad ITAT: Registered Sale Deed Triggers Capital Gains Despite Dispute; Matter Remanded Only for Correct Computation of Cost

Summary: The Hyderabad ITAT partly allowed the assessee’s appeal for statistical purposes. It held that the transfer of immovable property through a valid registered sale deed constituted a “transfer” under Section 2(47) and attracted capital gains tax under Section 45. The Tribunal rejected the assessee’s contention that no capital gains arose on the ground that the sale deed was executed under coercion and no sale consideration was actually received, observing that the assessee had acknowledged receipt of consideration in the registered sale deed and no cogent evidence was produced to support the subsequent plea, while pending criminal proceedings did not negate the taxability of capital gains. The Tribunal dismissed the assessee’s legal challenges relating to limitation, absence of DIN, non-faceless assessment, and non-issuance or non-service of notice under Section 143(2). However, it found that the Assessing Officer had adopted the cost of acquisition without explaining the basis and, since neither party could justify the computation, restored the issue of computation of long-term capital gains to the Assessing Officer for fresh verification and recomputation after providing the assessee an opportunity of being heard.

The Hyderabad ITAT held that once an immovable property is transferred through a valid registered sale deed, the transaction constitutes a “transfer” under section 2(47) and attracts capital gains taxation under section 45, notwithstanding the assessee’s claim that the sale deed was executed under coercion and that no sale consideration was actually received. The Tribunal observed that where the assessee had acknowledged receipt of consideration in the registered sale deed before the Registration Authority, a subsequent plea of non-receipt could not be accepted without cogent evidence, and pending criminal proceedings between the parties did not negate the taxability of capital gains. However, the Tribunal found that the Assessing Officer had adopted the cost of acquisition without any discernible basis, and since neither side could explain the computation, it restored the matter to the Assessing Officer for fresh verification and recomputation of the long-term capital gains after granting due opportunity to the assessee. The Tribunal also rejected the assessee’s legal challenges relating to limitation, absence of DIN, non-faceless assessment, and non-service of notice under section 143(2).

Cases Discussed:

- National Thermal Power Co. Ltd. Vs. CIT (1998) 229 ITR 383 (SC)

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal is filed by Smt. Mrunalini Kalagara (“the assessee”), feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC) (“Ld. CIT(A)”) dated 12.08.2025 for the A.Y. 2014-15.

2. The assessee has raised the following grounds of appeal:

“1. The Appellate order of the Ld. NFAC/ CIT(A) is bad and erroneous both on facts and in law.

2. On the facts and in the circumstances of the case and in law the Ld. NFAC/ CIT(A) has erred in not declaring the assessment order made by the ITO Ward-2, Khammam (JAO) u/s 143(3) r.w.s. 147 of the IT Act, 1961 as invalid and void ab initio as the assumption of jurisdiction by the JAO is improper and invalid as it is assumed in violation of CBDT Instruction No. 1 of 2011, assigning jurisdiction to the Assessing Officers based on monetary, pecuniary limitations. It ought to have considered the fact that the CBDT directions, instructions, circulars, etc., are binding on all the officers of the IT department and all the notice/ orders issued contrary to such CBDT directions, instructions, circulars are invalid.

3. On the facts and in the circumstances of the case and in law the Ld. NFAC/ CIT(A) has erred in not declaring the assessment order made by the ITO Ward-2, Khammam (JAO) u/s 143(3) r.w.s. 147 of the IT Act, 1961 as invalid and void ab initio as the same is made without issue and service of the mandatory notice u/s 143(2) of the Act. The NFAC/ CIT(A) ought to have considered that notice u/ 143(2) of the Act neither been issued nor served either physically on the assessee appellant OR through ITBA portal as claimed in the Appellate Order.

4. On the facts and in the circumstances of the case and in law the Ld. NFAC/ CIT(A) has erred in not properly considering and calculating the indexation cost of acquisition of the asset and improvements thereon in the computation of Long-term Capital Gains. He ought to have taken into consideration, the valuation report furnished by the appellant both during the assessment proceedings and also the first appellate proceedings in the computation of LTCG.

5. Such other ground OR grounds that may be urged during the hearing of the appeal.”

3. The assessee has raised the following additional grounds of appeal:

1. “On the Facts and in the circumstances of the case and in ‘raw the id. Assessing Officer erred in passing the Assessment Order with bock date after the date of statutory time limit and also in service of the same after the time limitation as prescribed in section 153(2) applicable for section 148 notices issued before OP April, 2019 and further, the Lei. NFACJCIT(A) as well hove erred in not declaring the Assessment Order cc invalid and void as the same time barred (Assessment Order served on 06-01-2020.

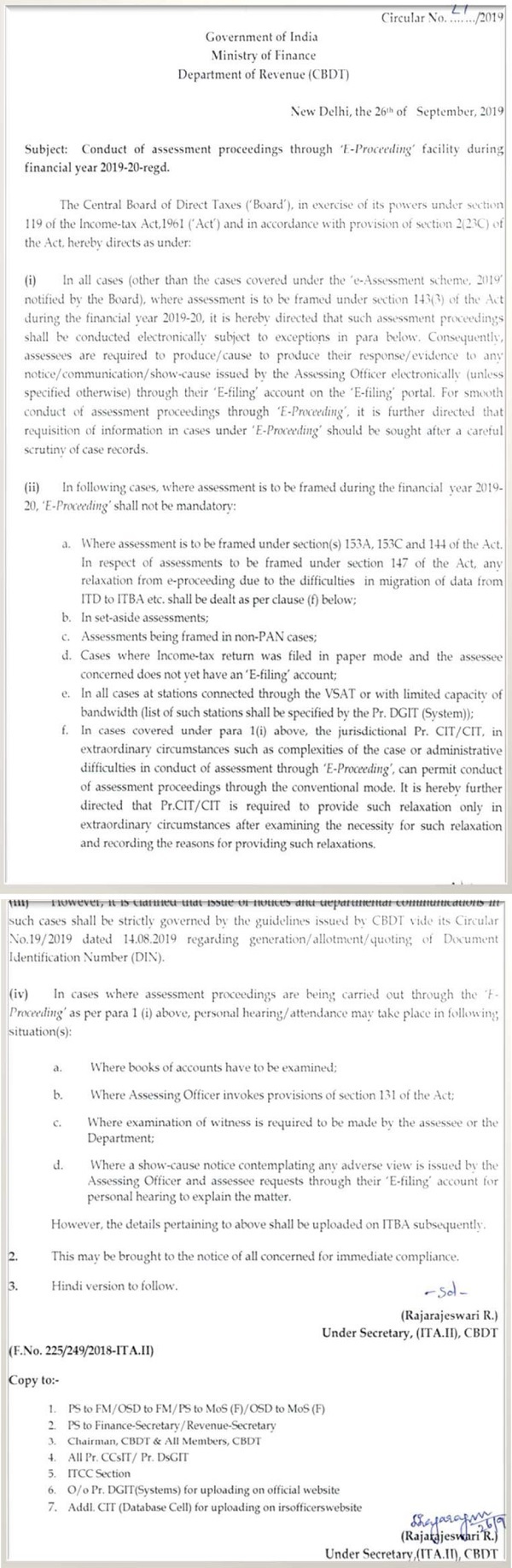

2. “On the facts and in the circumstances of the case and in law, whether the Assessment Order is valid as the Ld. Assessing Officer (JAO) hos passed the Assessment Order under section 143(3) r. w. s. 147 of the I. T. Act, 1961 in Violation of the CBOT Circular No.27 of 2019 which mandated that the Assessment proceedings must be conducted through ‘E-Proceeding’ facility during the F.Y.• 2019-20 and not in manual mode.

3. On the facts and in the circumstances of the case and in law, whether the Assessment Order is valid as the id, Assessing Officer (JAO) has passed the Assessment Order under section 143(3) r. w. s. 147 of the I. T Act, 1961 in violation of CBDT Notification No: 19 of 2019 doted 14-OS-2019 and without a computer generated ‘Document Identification Number’ (DIN) being quoted in the body of the Assessment Order”.

4. The Learned Authorized Representative (“Ld. AR”) submitted that additional grounds so filed are admissible in view of judgment rendered by the Hon’ble Supreme Court in the case of National Thermal Power Co. Ltd. Vs. CIT (1998) 229 ITR 383 (SC). As far as ground nos.1 and 3 of the additional grounds are concerned, the Learned Departmental Representative (“Ld. DR”) also did not raise any objection for admission of the additional grounds. Accordingly, the prayer for admission of additional grounds nos. 1 and 3, which are not in memorandum of appeal are being admitted for adjudication in terms of Rule 11 of the Income Tax (Appellate Tribunal) Rules, 1963 owing to the fact that objections raised in additional grounds are legal in nature for which relevant facts are stated to be emanating from the existing records.

5. Under Additional Ground No. 2, the assessee has challenged the validity of the assessment order passed by the Ld. AO on the ground that the assessment proceedings ought to have been conducted through the faceless assessment mechanism in accordance with CBDT Circular No. 27/2019 dated 26.09.2019. The Ld. AR invited our attention to the said Circular placed at page no. 29 of the paper book and submitted that the Ld. AO conducted the assessment proceedings proceedings manually contrary to the directions contained in the aforesaid Circular. It was submitted that the Circular issued by the CBDT is binding upon the departmental authorities and, therefore, any assessment framed in contravention thereof is liable to be held invalid. Accordingly, it was prayed that the additional ground be admitted and the assessment order be quashed.

5.1 Per contra, the Ld. DR submitted that the issue sought to be raised by the assessee requires verification of various factual aspects and cannot be decided merely on the basis of the material available on record. Therefore, the additional ground raised by the assessee does not deserve to be admitted.

5.2 We have heard the rival submissions and perused the material available on record. The assessee has sought admission of Additional Ground No. 2 challenging the validity of the assessment proceedings on the basis of CBDT Circular No. 27/2019 dated 26.09.2019. We have carefully gone through the aforesaid Circular, which is to the following effect:

5.3 On perusal of the above, we find that the Circular itself provides for certain exceptions and exclusions regarding the applicability of the e-proceedings scheme. Therefore, before adjudicating the legal contention raised by the assessee, it is necessary to ascertain various foundational facts, including whether the case of the assessee was covered by the e-proceedings scheme during the relevant period and whether it fell within any of the exceptions provided under the Circular. In our considered opinion, these factual aspects are not readily ascertainable from the material presently available on record. The applicability or otherwise of the Circular to the facts of the present case requires factual verification and examination of records, which are not emanating from the orders of the lower authorities or the material available before us. The Hon’ble Supreme Court in the case of National Thermal Power Co. Ltd. Vs. CIT (Supra) has held that a pure question of law arising from facts already available on record can be raised at any stage of the proceedings. However, where adjudication of the additional ground requires investigation into fresh facts not borne out from the existing record, such ground cannot be admitted merely by placing reliance upon the aforesaid decision. Since the issue raised by the assessee requires verification of factual aspects which are not emanating from the records available before us, we are of the considered view that the decision of the Hon’ble Supreme Court in the case of National Thermal Power Co. Ltd. Vs. CIT (supra) does not advance the case of the assessee in the peculiar facts and circumstances of the present case. Accordingly, Additional Ground No. 2 raised by the assessee is rejected and is not admitted for adjudication.

6. The brief facts of the case are that the assessee is an individual who filed his return of income for Assessment Year 2014-15 on 23.09.2014. From the information available with the Learned Assessing Officer (“Ld. AO”), it was noticed that during the year under consideration, the assessee had sold an immovable property for a consideration of Z1,59,00,000/- vide registered sale deed dated 23.05.2013.

However, no capital gain arising from such transfer was offered to tax in the return of income filed by the assessee. Accordingly, the case of the assessee was reopened under section 147 of the Income-tax Act, 1961 (“the Act”) and notice under section 148 of the Act was issued by the Ld. AO on 29.03.2019. In response thereto, the assessee filed a return of income on 26.04.2019 declaring total income of 24,02,780/- besides agricultural income of 270,000/-. Even in the return filed pursuant to notice under section 148 of the Act, the assessee did not disclose any capital gain arising from the sale of the aforesaid immovable property. After considering the submissions of the assessee, the Ld. AO computed the long-term capital gain arising from the transfer of the property at 291,66,655/- and made the addition accordingly in the hands of the assessee. The assessment was completed by the Ld. AO under section 143(3) read with section 147 of the Act on 31.12.2019 assessing the total income of the assessee at 295,69,430/-.

7. Aggrieved by the assessment order, the assessee preferred an appeal before the Ld. CIT(A). The Ld. CIT(A) confirmed the addition made by the Ld. AO and dismissed the appeal of the assessee.

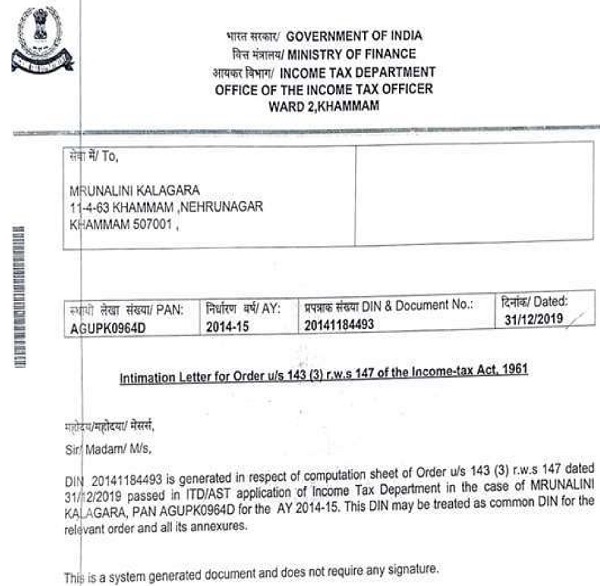

8. Aggrieved by the order of the Ld. CIT(A), the assessee is in appeal before this Tribunal. The Ld. AR submitted that under Additional Ground No. 1, the assessee has challenged the validity of the assessment order passed by the Ld. AO on the allegation that the assessment order is backdated and has in fact been passed beyond the period of limitation prescribed under the Act. The Ld. AR invited our attention to the intimation letter issued by the Ld. AO dated 31.12.2019 placed at page no.25 of the paper book and submitted that through online communication the Ld. AO had intimated only the DIN of the assessment order purportedly passed under section 143(3) read with section 147 of the Act dated 31.12.2019. It was submitted that the assessment order itself was not uploaded or communicated online on 31.12.2019. The Ld. AR further submitted that the assessment order was manually passed and a physical copy thereof was received by the authorized representative of the assessee only on 06.01.2020. According to the Ld. AR, if the assessment order had actually been passed on 31.12.2019, the same could also have been communicated electronically along with the communication of DIN. Inviting our attention to the provisions of section 153(2) of the Act, the Ld. AR submitted that the last date for passing the assessment order in the present case was 31.12.2019. Therefore, it was alleged that though the assessment order bears the date of 31.12.2019, it was in fact passed after 31.12.2019 and consequently the same is barred by limitation. Accordingly, it was prayed that the assessment order be quashed.

9. Per contra, the Ld. DR strongly opposed the contentions of the assessee. It was submitted that the assessment order was duly passed on 31.12.2019, which is evident from the communication issued by the Ld. AO through the online portal on the very same date intimating the DIN of the assessment order. The Ld. DR submitted that the allegation regarding back-dating of the assessment order is based merely on suspicion and conjectures and is not supported by any documentary evidence whatsoever. It was contended that the assessee has failed to bring any material on record to demonstrate that the assessment order was actually passed after 31.12.2019. Accordingly, the Ld. DR prayed for dismissal of the additional ground raised by the assessee.

10. We have heard the rival submissions and perused the material available on record. The solitary allegation under additional ground no.1 of the assessee is that the assessment order, though dated 31.12.2019, was actually passed after the expiry of the limitation period and has been back-dated by the Ld. AO. We find that such a serious allegation must necessarily be supported by cogent and reliable evidence. We have gone through the assessment order placed on record. On page no. 1 of the assessment order, the date of the order is specifically mentioned as 31.12.2019. We have also examined the communication issued by the Ld. AO through the online portal on 31.12.2019 and find that the DIN relating to the assessment order was duly intimated to the assessee on the very same date, namely 31.12.2019. During the course of hearing, a specific query was raised by the Bench to the Ld. AR as to whether any documentary evidence was available to substantiate the allegation that the assessment order was actually passed after 31.12.2019. However, the Ld. AR could not place on record any reliable documentary evidence in support of such allegation. The entire contention of the assessee is founded merely on the circumstance that the physical copy of the assessment order was received by the authorized representative on 06.01.2020. In our considered view, mere receipt of the physical copy on a later date cannot, by itself, lead to the conclusion that the assessment order was not passed on the date mentioned therein, particularly when contemporaneous records indicate otherwise. We find that the communication of DIN on 31.12.2019 corroborates the Revenue’s stand that the assessment order had already been passed on that date. In the absence of any contrary evidence, no adverse inference can be drawn against the Revenue merely on the basis of suspicion, surmises or conjectures.

10.1 We also deem it appropriate to observe that allegations of back-dating of judicial or quasi-judicial orders are serious in nature and ought not to be made lightly. Such allegations must be supported by credible and convincing evidence. In the present case, no such evidence has been brought on record by the assessee. Therefore, we deprecate the making of such allegations by the Ld. AR merely on the basis of suspicion and surmises without any supporting material. In view of the foregoing discussion, we find no merit in Additional Ground No. 1 raised by the assessee. Accordingly, the same is dismissed.

11. The assessee has raised Additional Ground No. 3 challenging the validity of the assessment order passed by the Ld. Assessing Officer. The Ld. AR submitted that the assessment order passed by the Ld. AO does not contain any Document Identification Number (“DIN”) on its face. Inviting our attention to the assessment order, he submitted that the absence of DIN renders the assessment order invalid in view of CBDT Notification No. 19 of 2019 dated 14.08.2019. According to the Ld. AR, the CBDT has made it mandatory that every communication issued by the Income-tax Department shall contain a valid DIN and any communication issued without DIN shall be treated as invalid. Therefore, since the impugned assessment order does not contain any DIN, the same is liable to be quashed as being non-est in the eyes of law.

12. Per contra, the Ld. DR strongly supported the orders of the lower authorities. Inviting our attention to the intimation letter dated 31.12.2019 placed at page no. 25 of the paper book, he submitted that although the DIN was not mentioned in the body of the assessment order, the Ld. AO had separately intimated the DIN corresponding to the impugned assessment order to the assessee on 31.12.2019 itself, i.e., on the very same day on which the assessment order was passed. The Ld. DR further submitted that section 292BA has been inserted by the Finance Act, 2026 with retrospective effect from 1.10.2019. As per the said provision, no assessment, reassessment or other proceeding under the Act shall be deemed to be invalid merely on account of any mistake, defect or omission relating to quoting of a computer-generated DIN, provided such assessment order or proceeding is referenced by such number in any manner. He submitted that in the present case the DIN corresponding to the impugned assessment order was duly communicated to the assessee vide letter dated 31.12.2019 and, therefore, the assessment order is fully protected by the provisions of section 292BA of the Act. Accordingly, the additional ground raised by the assessee deserves to be dismissed.

13. We have heard the rival submissions and perused the material available on record. We have gone through the letter dated 31.12.2019 placed at page no. 25 of the paper book whereby the Ld. AO had intimated the DIN corresponding to the assessment order to the assessee, the same is reproduced as under:

14. On perusal of the above, we find that a valid DIN had been generated by the Ld. AO on the very same day on which the assessment order was passed and the same was duly communicated to the assessee. We have also gone through the provisions of section 292BA of the Act, inserted by the Finance Act, 2026 with retrospective effect from 1.10.2019, which is to the following effect:

“Assessments not to be invalid on certain grounds.

292BA. Notwithstanding anything contained in any judgment, order or decree of any court, for the removal of doubts, it is hereby clarified for the purposes of section 2928 that no assessment under any of the provisions of this Act shall be invalid or shall be deemed to have been invalid on the ground of any mistake, defect or omission in respect of quoting of a computer generated Document Identification Number, if the assessment order is referenced by such number in any manner.”

14.1 On a plain reading of the provision of section 292BA of the Act, we find that it categorically provides that notwithstanding anything contained in any judgment, decree or order of any Court, no assessment, reassessment or other proceeding under the Act shall be deemed to be invalid merely by reason of any mistake, defect or omission in respect of quoting of a computer-generated DIN, if such assessment order or proceeding is referenced by such number in any manner. Thus, the legislative intent is abundantly clear that a mere defect, omission or mistake relating to quoting of DIN would not invalidate an assessment order so long as the order is referenced by such DIN in any manner. In the present case, there is no dispute regarding the fact that vide communication dated 31.12.2019, the Ld. AO had informed the assessee of the DIN corresponding to the impugned assessment order. Therefore, the assessment order stood duly referenced by a valid DIN and the requirement contemplated under the statutory framework stood substantially complied with. So far as the reliance placed by the Ld. AR on CBDT Notification No. 19 of 2019 dated 14.08.2019 is concerned, we find that the subsequently inserted section 292BA of the Act, having been enacted with retrospective effect from 1.10.2019, specifically addresses and cures defects relating to quoting of DIN. Therefore, to the extent relevant to the facts of the present case, the statutory provisions contained in section 292BA of the Act override the consequences sought to be drawn from the aforesaid CBDT Notification. Once an issue is covered by any specific Section of the Act, then the effect of CBDT Notification on the same issue becomes ineffective.

Accordingly, the reliance placed by the assessee on the said notification is misplaced and does not advance the case of the assessee. In view of the foregoing discussion, we do not find any merit in Additional Ground No. 3 raised by the assessee. Accordingly, the same is dismissed.

15. Under Ground No. 3 of the appeal, the assessee has challenged the validity of the assessment order passed by the Ld. AO on the ground that no notice under section 143(2) of the Income-tax Act, 1961 was issued or served upon the assessee. In this regard, the Ld. AR submitted that no notice under section 143(2) of the Act was either issued or served upon the assessee. It was contended that issuance and service of notice under section 143(2) of the Act is mandatory for framing an assessment under section 143(3) read with section 147 of the Act. Since no valid notice under section 143(2) of the Act was served upon the assessee, the assessment order passed by the Ld. AO is liable to be quashed as invalid and without jurisdiction.

16. Per contra, the Ld. DR placed on record a copy of the notice issued under section 143(2) of the Act dated 16.08.2019 and submitted that the Ld. AO had duly issued the statutory notice within the prescribed period. As regards the issue relating to service of notice, the Ld. DR submitted that the assessee participated in the assessment proceedings without raising any objection regarding non-service or improper service of notice. Inviting our attention to the provisions of section 292BB of the Act, the Ld. DR submitted that once the assessee has participated in the assessment proceedings and cooperated with the Ld. AO without raising any objection regarding service of notice, such objection cannot be raised for the first time at the appellate stage. Accordingly, the Ld. DR prayed that the ground raised by the assessee be dismissed.

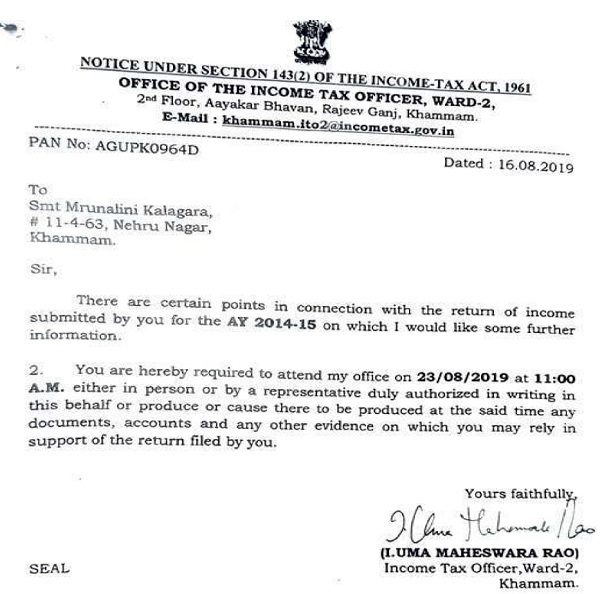

17. We have heard the rival submissions and perused the material available on record. The grievance of the assessee raised under ground no.3 is that no notice under section 143(2) of the Act was issued and served upon him. In this regard, we have gone through the copy of the notice issued by the Ld. AO under section 143(2) of the Act, which is to the following effect:

17.1 On perusal of the above, we find that the Ld. AO had issued notice under section 143(2) on 16.08.2019.

Therefore, the contention of the assessee that no notice under section 143(2) of the Act was issued is factually incorrect. As regards the issue relating to service of notice, we find merit in the contention of the Ld. DR. In this regard, we have gone through the provisions of section 292BB of the Act, which is to the following effect:

Notice deemed to be valid in certain circumstances. 292BB.

Where an assessee has appeared in any proceeding or co- operated in any inquiry relating to an assessment or reassessment, it shall be deemed that any notice under any provision of this Act, which is required to be served upon him, has been duly served upon him in time in accordance with the provisions of this Act and such assessee shall be precluded from taking any objection in any proceeding or inquiry under this Act that the notice was—

(a) not served upon him; or

(b) not served upon him in time; or

(c) served upon him in an improper manner: Provided that nothing contained in this section shall apply where the assessee has raised such objection before the completion of such assessment or reassessment.”

17.2 On a careful perusal of above, it is evident that the provisions contained in section 292BB of the Act clearly provide that where an assessee has appeared in any proceeding or cooperated in any inquiry relating to an assessment or reassessment, it shall be deemed that any notice required to be served upon him has been duly served in time and in accordance with the provisions of the Act. The only exception is where the assessee has raised an objection before the completion of the assessment proceedings regarding non-service, delayed service or improper service of notice. In the present case, no material has been placed before us to demonstrate that the assessee had raised any objection before the Ld. AO during the course of assessment proceedings regarding non-service or improper service of notice under section 143(2) of the Act. On the contrary, the assessee participated in the assessment proceedings and cooperated with the Ld. AO. Therefore, by virtue of the deeming provisions contained in section 292BB of the Act, the assessee is precluded from raising such objection for the first time before the appellate authorities. In view of the present facts and considering the provisions of section 292BB of the Act, we find no merit in the ground raised by the assessee. Accordingly, Ground No. 3 of the appeal is dismissed.

18. On merits, the Ld. AR submitted that the solitary issue arising out of the grounds of appeal relates to the addition of 291,66,655/- made on account of long-term capital gain. The Ld. AR submitted that though a sale deed in respect of the impugned property was executed, no sale consideration was actually received by the assessee. It was submitted that the sale deed was got executed under coercion and criminal proceedings in this regard are still pending before the competent Court. According to the Ld. AR, since no consideration was actually received by the assessee, no capital gain could be said to have arisen in the hands of the assessee. Accordingly, it was prayed that the addition made by the Ld. AO be deleted.

19. Per contra, the Ld. DR strongly supported the orders of the lower authorities. It was submitted that the assessee had transferred the property through a valid registered sale deed and, therefore, the transaction squarely falls within the definition of “transfer” as provided under section 2(47) of the Act. Consequently, the gain arising therefrom is chargeable to tax under section 45 of the Act. The Ld. DR submitted that the assessee himself admitted in the registered sale deed that the property was transferred for a specified consideration and, therefore, the plea that no consideration was received cannot be accepted in the absence of cogent evidence. Accordingly, the Ld. DR prayed for sustaining the addition made by the Ld. AO.

20. We have heard the rival submissions and perused the material available on record. As regards the taxability of capital gain, we find that there is no dispute about the fact that the assessee has transferred the immovable property through a valid registered sale deed. Therefore, the transaction is clearly covered within the meaning of “transfer” as defined under section 2(47) of the Act and consequently attracts the provisions of section 45 of the Act. The contention of the assessee that the sale deed was executed under coercion and that no consideration was actually received does not, by itself, negate the taxability of capital gain. During the course of hearing, a specific query was raised by the Bench to the Ld. AR as to whether the assessee had acknowledged receipt of consideration in the registered sale deed. In response, the Ld. AR fairly submitted that as per the recitals contained in the registered sale deed, the property had been transferred for a stated consideration. However, it was reiterated that no consideration was actually received by the assessee. In our considered view, once the assessee has admitted before the Registration Authority, which is a Government Authority, that the property has been transferred for a specified consideration, the subsequent plea that no consideration was received cannot be accepted in the absence of cogent and convincing material evidence. Therefore, we are unable to accept the contention of the assessee that no capital gain is chargeable merely because criminal proceedings are pending between the parties.

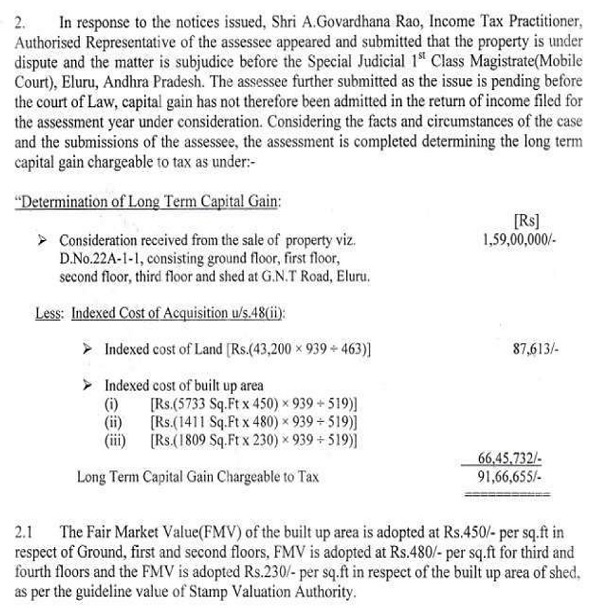

20.1 Further, we have also gone through para no. 2 of the order of the Ld. AO, which is to the following effect:

20.2 On perusal of the above, we find that while computing the long-term capital gain in the hands of the assessee, the Ld. AO has adopted the cost of acquisition of the land at 243,200/- without providing any basis or reasoning for arriving at such figure. During the course of hearing, both the parties were specifically asked to explain the basis on which the cost of acquisition was taken at 243,200/-. However, neither side could satisfactorily explain the basis for adopting the said figure. Since the correctness of the cost of acquisition goes to the root of the computation of capital gain, we are of the considered view that the matter requires fresh examination by the Ld. AO. Accordingly, while upholding the taxability of capital gain arising from the transfer of the property, we set aside the issue relating to the computation of long-term capital gain to the file of the Ld. AO with a direction to verify and re-adjudicate the working of capital gain, including the correct cost of acquisition and all other relevant components of computation, after providing adequate opportunity of being heard to the assessee. The assessee is directed to furnish all relevant documentary evidence in support of the cost of acquisition and other claims, if any. The Ld. AO shall thereafter recompute the capital gain in accordance with law. Accordingly, the ground raised by the assessee is partly allowed for statistical purposes.

21. In the result, the appeal of the assessee is partly allowed for statistical purposes.

Order pronounced in the Open Court on 8th July, 2026.

Author Bio