Case Law Details

In re Samsung India Electronics Pvt. Ltd. (CAAR Delhi)

M/s Samsung India Electronics Pvt. Ltd. filed an application before the Customs Authority for Advance Rulings (CAAR), New Delhi under Section 28H of the Customs Act, 1962 seeking an advance ruling on the classification of the proposed imports of “Moving Style” and its Floor Stand. The applicant proposed classification of “Moving Style” under HSN 8471 as an Automatic Data Processing Machine (ADPM) and the Floor Stand under HSN 8473 as an accessory suitable for use solely or principally with such machines.

The applicant described “Moving Style” as a 27-inch touchscreen smart device with a detachable wheeled stand, built-in battery, Tizen operating system, quad-core processor, RAM, internal storage, Wi-Fi, Bluetooth, HDMI and USB-C connectivity, built-in speakers and microphone, app installation capability, document editing through cloud-based applications, OTT streaming, remote PC access and touchscreen, virtual keyboard and voice input functionality. The applicant contended that the device satisfied all four conditions prescribed under Note 6(A) to Chapter 84 for classification as an ADPM. It further argued that the Floor Stand was an accessory designed solely or principally for use with the device and therefore classifiable under Heading 8473. The applicant relied on judicial decisions including Ingram Micro India Pvt. Ltd., Bright Point India Pvt. Ltd., Commissioner of Central Excise, Delhi v. Insulation Electrical (P) Ltd. and Pragati Silicons Pvt. Ltd. in support of its submissions.

The jurisdictional Customs Commissionerate accepted the applicant’s eligibility and confirmed that no proceedings on the issue were pending before any customs authority, appellate forum or court. However, on merits, it disagreed with the proposed classification. According to the Commissionerate, “Moving Style” was essentially a movable interactive display panel or mobile variant of an Interactive Flat Panel, marketed and intended primarily for collaborative workspaces, education, meetings, presentations and home entertainment. It considered the embedded processor, operating system, RAM and storage to support the display functions rather than alter the product’s essential character. Relying on Chapter Notes 6(D) and 6(E) to Chapter 84, Section Note 3 of Section XVI and decisions including Commissioner of Customs, Bangalore v. N.I. Systems (India) Pvt. Ltd. and Commissioner of Customs (Import & General), New Delhi v. Integral Computer Ltd., the Commissionerate proposed classification of “Moving Style” under CTH 8528 59 00 as “Other Monitors” and the Floor Stand under Heading 8529.

During the personal hearing, the applicant reiterated that the product differed from an Interactive Flat Panel Display owing to its smaller screen size, lower resolution, lower power consumption and other technical characteristics, and described it as a large Wi-Fi-enabled tablet. Additional written submissions were also filed rebutting the Commissionerate’s comments and reiterating that the product fulfilled all conditions of Note 6(A), that Notes 6(D) and 6(E) had been incorrectly applied, and that the product should remain classified under Heading 8471.

After examining the application, technical specifications, Commissionerate’s comments, personal hearing submissions and the relevant tariff provisions, the Authority identified the principal issues as whether “Moving Style” was classifiable under Heading 8471 or Heading 8528 and whether the Floor Stand fell under Heading 8473 or Heading 8529. The Authority considered Rule 1 of the General Rules for Interpretation, Chapter Note 6 to Chapter 84, Section Note 3 of Section XVI and the relevant HSN Explanatory Notes.

The Authority observed that although “Moving Style” incorporated a processor, RAM, internal storage, operating system, application support, connectivity features and multimedia capabilities, those computing elements functioned as integral control components supporting the integrated display system. It held that the principal function of the product was to provide a touchscreen display for group presentations and collaboration rather than standalone general-purpose data processing. According to the Authority, the embedded computing components did not alter the technical identity of the product as an interactive display device. It further observed that many monitors incorporate embedded processors and operating systems while remaining classifiable under Heading 8528 where their primary purpose continues to be display. Applying Chapter Notes 6(D) and 6(E) to Chapter 84 together with Section Note 3 of Section XVI, the Authority concluded that “Moving Style” did not merit classification under Heading 8471 but was classifiable under Heading 8528. It also referred to Supreme Court decisions emphasising functional utility, predominant usage and end use in classification.

The Authority further examined the eight-digit tariff entries under Heading 8528 and concluded that the product was not a cathode ray tube monitor and was not designed for use with an automatic data processing machine under Tariff Item 8528 52 00. Accordingly, it held that “Moving Style” was classifiable under Tariff Item 8528 59 00 as “Other Monitors.” It also noted that the Port Commissionerate had taken the same view. Regarding the Floor Stand, the Authority held that Heading 8529 covered parts suitable for use solely or principally with apparatus of Headings 8524 to 8528. As the Floor Stand was suitable for use solely or principally with “Moving Style,” it was classified under Tariff Item 8529 90 90. The Authority accordingly ruled that “Moving Style” was classifiable under Tariff Item 8528 59 00 and the Floor Stand under Tariff Item 8529 90 90 of the First Schedule to the Customs Tariff Act, 1975.

FULL TEXT OF THE ORDER OF CUSTOMS AUTHORITY OF ADVANCE RULING, DELHI

M/s Samsung India Electronics Pvt. Ltd, 6th Floor, DLF Centre Sansad Marg, New Delhi, India – 110001 (herein referred to as “applicant”), having TEC No. 595032818 submitted an application dated 04.02.2026 before the Customs Authority for Advance Rulings, New Delhi (CAAR, New Delhi in short) for obtaining Advance Ruling under Section 28H of the Customs Act, 1962, to seek clarity on the classification on the import of ‘Moving Style’ to India. The application was accordingly registered under Serial No. 194/2025-26 dated 04.02.2026.

STATEMENT OF RELEVANT FACTS HAVING A BEARING ON THE QUESTION (S) ON WHICH ADVANCE RULING IS REQUIRED

1.1 Samsung India Electronics Private Limited (herein after referred to as, “Applicant” / “SIEL”) is a Company incorporated in India and having its Registered Office at 6th Floor, DLF Centre, Sansad Marg, New Delhi, India — 110001.

1.2 The Applicant intends to import ‘Moving Style’ in India for further sale. It is further stated that no processing whatsoever would be carried out on the imported goods, post importation into India.

Description & Usage of Moving Style

1.3 The Moving Style is an innovative smart device with the versatility of a computing device. Unlike traditional monitors or televisions, it is designed for mobility and interactivity, featuring a detachable stand with wheels and a built-in battery for wireless operation. This makes it ideal for dynamic environments where flexibility and portability are essential, such as collaborative workspaces, educational settings, and home entertainment.

1.4 The device is equipped with a 27-inch LCD screen that supports capacitive touch input, enabling intuitive interaction without the need for external peripherals. It runs on Samsung’s proprietary Tizen Operating Software, which allows users to install, delete, and run applications directly on the device. In addition to OTT streaming capabilities, the Moving Style supports remote access to PCs and cloud-based platforms like Microsoft 365, enabling document creation and editing for productivity tasks.

1.5 From a hardware perspective, the Moving Style integrates a quad-core processor, 4GB RAM, and I 6GB internal storage, ensuring smooth performance for both entertainment and work applications. It offers multiple connectivity options, including HDMI and USB-C ports, as well as wireless modules for Wi-Fi and Bluetooth. Built-in speakers and a microphone provide audio functionality, while the touch interface and virtual keyboard enhance usability for diverse scenarios.

1.6 This combination of advanced display technology, computing capability, and mobility positions the Moving Style as a hybrid device that bridges the gap between smart display and interactive computing systems. Its ability to stream content, run applications, and connect to external devices makes it a versatile solution for modern digital lifestyles, catering to both personal and professional needs.

1.7 The main components and specifications of the ‘Moving Style’ have been outlined below:

Main Components:

- 27-inch Display: LCD with TFT and CF substrates, liquid crystal injected into OPEN CELL, polarizer, BLU, cover glass, etc.

- Touchscreen: Detects touch through changes in capacitance; consists of glass substrate and controller IC.

- Printed Board Assembly: Printed Circuit Board with integrated components to run operating System.

- Timing Controller (TCON): Converts video signals for panel operation and controls pixel timing.

- Battery: Built-in 69WH battery; supports charging via USB-C external battery.

- Wireless Modules: Wi-Fi, hotspot, Bluetooth connectivity.

- Ports: HDMI x I, USB-C x2.

- Audio: Built-in speaker and microphone.

- Frame:

Specifications

- Operating System: Tizen Smart TV

- CPU: PONTUS-M Quad Core CA72 @ 1.7GHz

- Data Transfer Rate: Up to approx. 25.6GB/s (memory bandwidth)

- RAM: LPDDR4 64-bit 1.6GHz x 2, 4GB

- Internal Storage: eMMC I6GB

- Flash Memory: 2MB

1.8 The Moving Style provides a wide range of functionalities, including app installation and deletion, OTT streaming, and document editing through cloud-based applications. It supports wired and wireless internet connectivity, remote PC access, and screen mirroring for seamless integration with external devices. The touchscreen and virtual keyboard allow for easy navigation and text input, while voice recognition adds convenience. Designed for mobility, the screen can be mounted on or detached from its stand, enabling users to reposition it effortlessly for different use cases such as meetings, presentations, or home entertainment. The Functions and Usage of the Moving Style have been listed below:

1. App Installation/Deletion: Apps can be installed or deleted via Samsung TV Apps (Tizen OS-based app store).

2. Internet & Device Connectivity: Supports wired/wireless network via LAN or Wi-Fi; external devices can connect via HDMI, DisplayPort, Type-C; supports screen mirroring from smartphones.

3. Document Editing via Applications: Through Samsung Smart TV Workspace, remote access to Windows PC, Mac, or mobile devices; supports Microsoft 365 for cloud-based document editing.

4. Touchscreen & Virtual Keyboard: Capacitive touch input; virtual keyboard for text input via touch or remote; voice input supported.

5. Content Streaming: Real-time streaming of video/music from online platforms via network or mirroring.

6. Screen Mobility: Screen can be mounted/detached from stand; stand has wheels for easy movement; screen can stand independently.

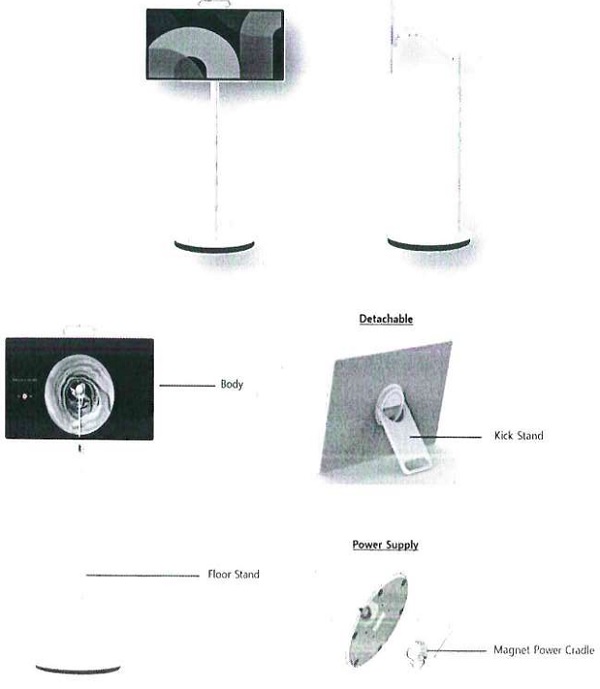

1.9 For ease of reference, the images of ‘Moving Style’ are reproduced below:

1.10. To sum up, the Moving Style is used just like a compact computer that lets users work with information, documents, apps, and online content directly on the device. It runs on its own operating system (Tizen OS) and allows users to create, edit, save, and manage documents, access files from USB or the network, and even work on cloud platforms such as Microsoft 365. The device also supports installing and deleting apps, browsing the internet, logging into remote PCs, and mirroring content from phones and laptops. It processes user inputs through the touchscreen, virtual keyboard, and voice commands, and provides outputs through its display and speakers.

Details of the Proposed Transaction

1.11 The Applicant intends to import ‘Moving Style’ in India for further sale to domestic customers.

Eligibility to file Application for Advance Ruling

1.12 Based on the criteria specified under Chapter VB, Customs Act, 1962, the following checklist has been prepared in order to prove that Applicant is eligible to file this Application, inter cilia;

| I. | Whether the Applicant holds a valid IEC Number at the date of filing this Application? | Yes |

| II. | Whether the present Application has been filed in respect of goods prior to importation in India? | Yes |

| III. | Whether the present Application is barred under Sec. 28-I (2), Customs Act? | No |

| IV. | Whether the subject-matter of the present Application is eligible to seek Advance Ruling, in terms of Sec. 28-H (2), Customs Act? | Yes |

| V. | Whether prescribed Court-fees has been paid at the time of filing the present Application | Yes |

1.13 Further, the Applicant wishes to seek an Advance Ruling for determination of HSN classification of the ‘Moving Style’ proposed to be imported into India.

1.14 In this regard, the Applicant wishes to disclose that the Company intends to regularly import `Moving Style’ Statement containing Applicant’s interpretation of law and / or facts, as the case may be, in respect of Questions on which Advance Ruling is sought?

1.15 Questions on which Advance Ruling is sought

- Question 1: Whether ‘Moving Style’ imported into India would merit classification under HSN 8471 as “Automatic Data Processing Machines and units thereof; Magnetic or optical readers, machines for transcribing data on to data media in coded form and machines for processing such data, not elsewhere specified or included”

- Question 2: Whether the Floor stand imported with the Moving Style in same or a different shipment merit classification under HSN 8473 as “Parts and accessories (other than covers, carrying cases and the like) suitable for use solely or principally with machines of headings 8470 to 8472”.

1.16 Question 1: Whether ‘Moving Style’ imported into India would merit classification under HSN 8471 as “Automatic Data Processing Machines and units thereof; Magnetic or optical readers, machines for transcribing data on to data media in coded form and machines for processing such data, not elsewhere specified or included”

Import of ‘Moving Style’ into India and its classification

1.17 The Applicant intends to import and sell ‘Moving Style’ in India. For the purposes of import, we need to determine the HSN under which the import can be made.

1.18 The mechanics of determining the classification of any product is as under:

√ World Customs Organisation (`NN/CO’) has enunciated the Harmonized Commodity Description and Coding System or Harmonized System of Tariff Nomenclature (HSN), an internationally standardized system which lays the foundation of classification of goods across the globe.

√ WCO has also issued Explanatory Notes to HSN (“Explanatory Notes”) which provides an insight into the meaning of expressions employed in the HSN and are used for easy interpretation of different commodity groups created under the HSN.

√ In India, classification under the First Schedule to the Customs Tariff Act, 1975 (also referred to as “CTA”) is governed by the General Rules for the Interpretation of the Schedule (`GM’) prescribed therein. These GRI are to be applied sequentially while determining the classification of a particular product. The First Schedule and GRI are simply a derivative of the HSN issued by the WCO.

√ Further, the Explanatory Notes to the above First Schedule of CTA provide a safe guide for interpretation of the said First Schedule and hold a high persuasive value as observed by the Hon’ble Supreme Court in Wood Craft Products Limited 11995 (77) ELT 23 (SC)].

1.19 In order to determine the rate of Customs duty applicable to particular Products which are imported into India, it is important to identify the classification of such Products under the Schedules to the CTA.

1.20 The First Schedule to CTA has 21 Sections and 98 Chapters. A Section is a group consisting of several Chapters which codify a particular class of goods. The Section notes explain the scope of various Chapters/ Headings contained in such Sections. The Chapters consist of Chapter Notes, brief description of the Products arranged in 4-digit, 6-digit and 8-digit levels. 4-digit code is referred as ‘Heading’ followed by 6-digit code referred as ‘Sub-Heading’ and 8-digit code referred as ‘Tariff Item’.

1.21 Rate of duty for a particular Product is specified at 8-digit or Tariff Item level. Thus, to determine the rate of duty on any imported Product, classification at 8-digit or Tariff Item level needs to be identified and the classification has to be determined sequentially i.e., first classification at 4-digit level (Heading) then at 6-digit level (Sub-heading) and finally at 8-digit level (Tariff Item).

1.22 In view of the above, it becomes important to analyse the GRI to determine the proper classification under the CTA. Rule 1 of GRI provides that the classification shall be determined in line with the following which needs to be followed in sequential order. The classification shall be determined according to the terms of headings and any relative Section or Chapter Notes. The relevant text is reproduced as under:

“1. The titles of Sections, Chapters and sub-chapters are provided for ease of reference only; for legal purposes, classification shall he determined according’ to the terms of the headings and any relative Section or Chapter Notes and, provided such headings or Notes do not otherwise require, according to the following provisions:”

1.23 Basis the above, Rule I of G IR, classification must be in accordance with the terms of Chapter heading and any other relevant Section and Chapter Notes.

1.24 In the event the articles cannot be classified solely on the basis of GRI I, then GRI’s 2 to 6 may be applied in order, as appropriate.

1.25 Basis the above, let us now proceed to analyse the relevant HSN classification with respect to the subject ‘Moving Style’.

Whether ‘Moving Style’ imported into India would merit classification under USN 8471 as “Automatic Data Processed Machines and units thereof Magnetic or optical readers, machines for transcribing data on to data media in coded form and machines for processing such data, not elsewhere specified or included”

1.26 Chapter 84 of the First Schedule to CTA pertains to “Nuclear reactors, boilers, machinery and mechanical appliances; parts thereof”. Further, heading 8471 covers “Automatic data processing machines and units thereof’ magnetic or optical readers, machines br transcribing data on to data media in coded form and machines for processing such data, not elsewhere specified or included”. The said entry has been reproduced below for ready reference:

| Tariff Entry | Description | |

| 8471 | AUTOMATIC DATA PROCESSING MACHINES AND UNITS THEREOF; MAGNETIC OR OPTICAL READERS, MACHINES FOR | |

| TRANSCRIBING DATA ON TO DATA MEDIA IN CODED FORM AND MACHINES FOR PROCESSING SUCH DATA, NOT ELSEWHERE SPECIFIED OR INCLUDED | ||

| 8471 30 10 | — | Personal computer |

| 8471 30 90 | — | Other |

| – | Other automatic data processing machines: | |

| 8471 41 | — | Comprising in the same housing at least a central processing unit and an input and output unit, whether or not combined: |

| 8471 41 10 | — | Micro computer |

| 8471 41 20 | — | Large or main frame computer |

| 8471 41 90 | — | Other |

| 8471 49 00 | — | Other, presented in the form of systems |

| 8471 50 00 | – | Processing units other than those of sub-headings 8471 41 or 8471 49, whether or not containing in the same housing one or two of the following types of unit: storage units, input units, output units |

| 8471 60 | – | Input or output units, whether or not containing storage units in the same housing: |

| 8471 70 | – | Storage units: |

| 8471 90 00 | – | Other |

1.27 Automatic data processing machines (`ADPM’) and their units are primarily regulated for classification purposes by Note 6 to Chapter 84. Note 6 to Chapter 84 have been reproduced below for ease of reference:

“6(A) For the purposes of heading 8471, the expression “automatic data processing machines” means machine capable of

(i) storing the processing programme or programmes and at least the data immediately necessary for the execution of the programme

(ii) being freely programmed in accordance with the requirements of the user;

(iii) performing arithmetical computations specified by the user; and

(iv) executing, without human intervention, a processing programme which requires them to modem their execution, by logical decision during the processing run;

(B) Automatic data processing machines may be in the form of systems consisting of a variable number of separate units.

(C) Subject to paragraph (D) and (E), a unit is to be regarded as being a part of an automatic data processing system if it meets all of the following conditions :

(i) it is of a kind solely or principally used in an automatic data processing system;

(ii) it is connectable to the central processing unit either directly or through one or more other units; and

(iii)it is able to accept or deliver data in a form (codes or signals) which can be used by the system.

Separately presented units of an automatic data processing machine are to be classified in heading 8471.

However, keyboards, X-Y co-ordinate input devices and disk storage units which satisfy the conditions of (ii) and (iii) above, are in all cases to be classified as units of heading 8471.

(D) Heading 8471 does not cover the following when presented separately, even if they meet all of the conditions set forth in paragraph (C) :

(i) printers, copying machines, facsimile machines, whether or not combined;

(ii) apparatus for the transmission or reception of voice, images or other data, including apparatus for communication in a wired or wireless network (such as a local or wide area network);

(iii) loudspeakers and microphones;

(iv) television cameras, digital cameras and video camera recorders;

(v) monitors and projectors, not incorporating television reception apparatus.

(E) Machines incorporating or working in conjunction with an automatic data processing machine and performing a specific function other than data processing are to be classified in the headings appropriate to their respective functions or, failing that, in residual headings.”

1.28 Further the explanatory notes to CTH 8471 provides that “The automatic data processing machines of this heading must be capable of fulfilling simultaneously the conditions laid down in Note 6(A) to this Chapter That is to say, they must be capable of:

(1) Storing the processing program or programs and at least the data immediately necessary for the execution of the program;

(2) Being freely programmed in accordance with the requirements of the user;

(3) Performing arithmetical computations specified by the user; and

(4) Executing, without human intervention, a processing program which requires them to modify their execution, by logical decision during the processing run. Thus, machines which operate only on fixed programs, i.e., programs which cannot be modified by the user, are excluded even though the user may be able to choose between a number of such fixed programs,

These machines have storage capability and also stored programs which can be changed, from job to job. “

1.29 Note 6(A) to Chapter 84 provides that, for the purposes of Heading 8471, “automatic data processing machines” are machines capable of

1. storing the processing program(s) and at least the data immediately necessary for execution of program

2. being freely programmable in accordance with the user’s requirements,

3. performing arithmetical computations specified by the user, and

4. executing, without human intervention, a processing program which requires them to modify their execution by logical decision during the processing run.

Moving Style satisfies the first condition of Note 6(A) to Chapter 84, which requires the machine to be capable of storing the processing program(s) and al least the data immediately necessary for execution:

1.30 The Moving Style is equipped with a proprietary operating system (Tizen OS) and internal storage components that enable it to store processing programs and essential data required for execution of program. Specifically, the device incorporates 16GB eMMC internal storage and 4GB LPDDR4 RAM, which together provide sufficient capacity to retain the operating system, installed applications, and data necessary for program execution. This architecture ensures that the device can run multiple applications and maintain system processes without relying on external storage.

1.31 Unlike fixed-function devices, the Moving Style supports dynamic installation and deletion of applications. Users can download productivity tools, streaming applications, and other software directly onto the device, which are then stored in its internal memory. This capability demonstrates compliance with the requirement to store processing programs and associated data.

1.32 The presence of a Quad-Core CA72 processor and integrated memory management further reinforces the device’s ability to handle stored programs efficiently. The processor executes instructions from the stored operating system and applications, while the RAM provides immediate access to data necessary for execution. This configuration mirrors the functionality of an ADPM, as defined under Heading 8471, by enabling real-time processing of user commands and application workflows.

1.33 Additionally, the Moving Style supports cloud-based services such as Microsoft 365, which require local storage of authentication data, temporary files, and cached content during operation. This interaction between local storage and remote resources highlights the device’s capability to manage both persistent and transient data essential for program execution. Therefore, the Moving Style clearly satisfies the first condition under Note 6(A) by storing processing programs and the data immediately necessary for their execution.

The second condition under Note 6(A) to Chapter 84 requires that an Automatic Data Processing Machine (ADPM) must be freely programmable in accordance with the requirements of the user.

1.34 This means the machine should allow the user to install, modify, and execute programs of their choice without artificial restrictions, beyond a fixed set of pre-installed applications.

1.35 To assess the scope of the phrase “freely programmable” better, reliance is placed on the judgment of the Hon’ble CESTAT, New Delhi in the judgment of M/s. Ingram Micro India Private Limited versus Principal Commissioner of Customs (Import), New Delhi 2022 (2) TM 308 -CESTAT New Delhi wherein while determining the classification of view board i.e., Interactive Display System the Court discussed the scope of the phrase “freely programmable in accordance with the requirements of the user”.

1.36 The Hon’ble Tribunal, while discussing the capabilities of the machine, explained that a machine which can download and install new programs in accordance with the needs and usage of the user is said to be freely programmable. Relevant extract of the judgment is produced as below for ease of reference.

“19. The goods come with a pre-installed operating system, namely, Android 7.0. The said Android version is a customized operating system for these 1FP. Further, the goods also have an OPS slot. With the use of the OPS Slot, additional hardware can be connected to the goods and the OPS Slot can also he used for installing other operating software such as Windows, etc. on the goods. Thus, the goods are machines on which the user is able to load and execute a program. In other words, the goods are capable of executing any application/ program which is stored on its memory. A user can, with the use of either Android or other operating systems, download and install new programmes in accordance with their needs and usage. Thus, goods are machines which can be freely programmed in accordance with the need of the user and hence, satisfi, condition (ii) of Chapter Note 5(A) to Chapter 84.”

1.37 It is pertinent to note that the interpretation of “freely programmable” under Note 6(A)(ii) has been consistently discussed in multiple rulings. The decision in the case of Ingram Micro India Pvt. Ltd. (supra) has become a key reference point and has been relied upon in several subsequent cases. 1.38 In the case of Bright point India Pvt Ltd. 2023 (6) TMI 657 —AAR Customs, Mumbai, it was observed that the product in question had a pre-installed operating system, that is the customized operating system for those devices. It is capable of downloading and installing new programmes in accordance with the needs of the user and executing any application/program stored on its memory. Thus, the product was freely programmable. The relevant extract has been reproduced below:

As per Note 6(A)(ii), the machine should be able to be freely programmed in accordance with the requirement of the user. From the product details submitted, it appears that these goods come with a pre-installed operating system, namely, Android, that is the customized operating system for these device. It has an OPS slot, enabling connection of additional hardware and installing other operating software such as Windows, etc. It is capable of downloading and installing new programmes in accordance with the needs of the user and executing any application/program stored on its memory. Therefore, the goods satisfy condition as per 6(A)(ii).”

1.39 In light of the preceding paragraphs, a machine is said to be freely programmable if the user can install and download new programs and delete the existing applications as per his requirements from such machine. This understanding is also backed by the I-ISN explanatory notes to heading 8471 that machines which operate only on fixed programs, i.e., programs which cannot be modified by the user, are excluded from category of A DPM.

1.40 The cumulative judicial position, as reflected in Ingram Micro (2022 (2) TMI 308 — CESTAT New Delhi), and Bright point India (2023 (6) TMI 657 — CAA R Mumbai), is that the ability to install new programs or operating systems at the user’s discretion even through controlled mechanisms like OPS slots or developer modes, has generally been treated as satisfying the “freely programmable” criterion under Note 6(A)(ii).

1.41 The Moving Style satisfies this requirement through its Tizen OS, which provides an open environment for application management. Users can install, delete, and execute applications. This includes productivity tools like Microsoft 365, OTT streaming apps, and remote access utilities. The ability to add or remove applications dynamically ensures that the device is not limited to fixed programs, but rather adapts to the user’s evolving requirements, precisely the essence of “free programmability” under Note 6(A).

1.42 Beyond app installation, the Moving Style supports remote PC access, enabling users to run programs hosted on external systems, and offers browser-based execution of web applications. This flexibility allows the device to serve multiple roles—entertainment hub or productivity workstation—based entirely on user-selected software. The presence of configurable settings, virtual keyboard, voice input, and peripheral connectivity further enhances programmability, allowing users to tailor the execution environment to their needs.

1.43 The Moving Style runs on Tizen OS, which enables users to install, delete, and execute applications at will. Beyond the preloaded system components, users can add productivity apps (e.g., cloud-based editors), streaming apps, utilities, and connectivity tools, and remove them when no longer needed. This user-directed application I ifecycle demonstrates that the device is not confined to a fixed program set; rather, it accepts new programs, replaces existing ones, and updates packages in line with the user’s operational requirements.

1.44 In addition to app installation/deletion, users can configure system and app settings, manage software updates, and apply usage policies (e.g., network, input, display preferences). These controls allow the user to adapt the execution environment to evolving requirements switching between entertainment, collaboration, and productivity profiles as needed. The capacity to alter system behavior through configurable software components, coupled with the ability to load new programs on demand, demonstrates that the Moving Style is freely programmable within the meaning of Note 6(A).

1.45 The Moving Style does not impose artificial limitations on application installation or execution. It accepts new programs, allows deletion of existing ones, and supports user-driven configuration. Therefore, it clearly meets the second condition under Note 6(A).

Moving Style equipped with embedded processors fulfil the third condition of Note 6(A) to Chapter 84, which requires the machine to be capable of performing arithmetical computations specified by the user:

1.46 These devices incorporate a processor architecture supports a wide range of instruction sets, including arithmetical and logical operations, divide and multiply instructions, and parallel arithmetic instructions.

1.47 The Moving Style is equipped with a Quad-Core CA72 processor and a fully functional operating system (Tizen OS), which together enable it to execute arithmetic and logical operations as part of its core computing functions. These operations are not limited to system-level tasks, they extend to user-specified computations performed through installed applications or cloud-based platforms. This capability aligns with the requirement that the machine must perform arithmetic computations as directed by the user.

1.48 Additionally, through integrated support for Microsoft 365 and similar productivity applications, users can create and edit spreadsheets, perform formula-based calculations, and execute data analysis tasks directly on the device. These functions involve arithmetic computations such as addition, subtraction, multiplication, division, and more complex operations like percentage calculations and conditional logic. The Device’s ability to handle these tasks demonstrates compliance with the condition that it can perform user-defined arithmetic operations.

1.49 Beyond simple arithmetic, the Moving Style can execute logical operations and data processing tasks required for application workflows, such as sorting, filtering, and conditional formatting in spreadsheets or rendering calculations in graphical applications. These processes involve arithmetic and logical computations specified by the user, reinforcing that the device meets the third criterion under Note 6(A) for classification as an ADPM.

Moving Style also satisfy the fourth condition of Note 6(A) to Chapter 84, which requires the machine to execute, without human intervention, a processing program that modifies its execution by logical decision during the processing run:

1.50 The Moving Style, powered by Tizen OS, executes multiple concurrent processes, applications, and background tasks under an event-driven architecture. Once a program is launched, the operating system’s scheduler and event loop autonomously handle interrupts, prioritize threads, and allocate memory without further human input. As runtime conditions change (e.g., network availability, battery level, or Input / Output events), the system modifies execution paths by invoking different handlers and adjusting process priorities, thereby meeting the requirement of logical decision-making during the processing run.

1.51 During OTT streaming or cloud-based document editing, the device makes autonomous decisions in response to real-time conditions—switching codecs/bitrates for streaming when bandwidth fluctuates, queuing or retrying network requests on transient failures, and regulating CPU/GPU usage or dimming the display when battery constraints are detected. These behaviors reflect conditional logic embedded in system and application code that changes execution flow (e.g., fallbacks, retries, state transitions) without user intervention, ensuring continuous, efficient operation.

1.52 Installed applications employ internal state machines and control flows that dynamically branch based on inputs and runtime outcomes—such as authentication success/failure, file Input /Output results, or permission checks. For instance, a cloud editor will automatically cache, autosave, and reconcile documents, choosing different routines depending on network state and data integrity checks; a media app will pre-buffer, re-buffer, or pause based on stream health. These branching decisions are taken by the program logic itself and modify the execution pathway as conditions evolve.

1.53 Even when the user is not actively interacting, the Moving Style processes asynchronous events (touch, audio, HDMI/USB-C hot-plug, Bluetooth/Wi-Fi signals) and responds through predefined error-handling and recovery routines—e.g., remounting devices, renegotiating protocols, or switching to offline modes. Such routines enable the program to continue or alter its course autonomously. Collectively, these mechanisms demonstrate that the Moving Style executes programs without human intervention and modifies execution by logical decision during processing, thereby satisfying Condition 4 of Note 6(A).

1.54 Accordingly, it may be inferred that the Moving Style satisfy all four conjunctive conditions under Note 6(A) to Chapter 84 to qualify as ADPM under Tariff head 8471.

1.55 A Device (classifiable as ADPM under CTH 8471 shall incorporate an input device (mouse / keyboard), a Central Processing Unit (CPU) and a Output device, (Monitor). Generally, earlier they would be presented separately but in modern day evolution, we are getting hybrid devices / computers, where all the three (input, CPU as well as display) are all integrated in a single housing. Such an integrated hybrid system shall qualify as ADPM.

1.56 its given that the principal character of the machine is a freely programmable, general-purpose computing device that can join wired/wireless networks, access/manipulate files, run OTT apps and productivity suites, and operate stand-alone with integrated input (capacitive touchscreen/virtual keyboard/voice) and output (LCD and speakers) in the same housing. In the case of Bright point (supra) it was held that such interactive systems capable of performing plethora of functions independently on standalone basis should be classified as ADPM. The relevant extract has been reproduced below for ready reference;

“It is found that the subject goods are capable of performing plethora of functions independently on standalone basis and these devices are much more than mere display devices. In fact, display is only one of the features of the goods and cannot be construed to be its only function, much less its principal function. Also, the subject goods satisfy all the conditions laid down under Note 6(A) of Chapter 84, thereby validating the expression “automatic data processing machine”. Thus, ‘ Interactive Display System (View Board)’ models mentioned in para 1 merit classification under Heading 8471 and more specifically under sub-heading 84714190 of the first schedule to the Customs Tariff Act, 1975., “

1.57 Basis the above discussion, the Moving Style under consideration appear to be classifiable as other ADP machines under subheading 8471 41 which covers other ADP machines; comprising in the same housing at least a central processing unit and an input and output unit, whether or not combined. For the device under consideration, the LCD screen satisfies the requirement for output and the touch scrccn satisfies the requirement for input apart from the CI’U inbuilt into the device. Therefore, the subject goods appear to be classifiable under subheading 847141 and more specifically under subheading 8471 41 90 as “Other automatic data processing machines: Comprising in the same housing at least a central processing unit and an input and output unit, whether or not combined: Other”.

1.58 Further, attention is drawn to the Tariff structure which introduces further decisive provisions, Note 6(D) and Note 6(E) to Chapter 84, which must also be considered.

1.59 Note 6(D) to Chapter 84 explicitly provides that Heading 8471 does not cover certain goods when presented separately, even if they meet all the conditions set forth in Note 6(C). Among the listed exclusions are:

“(i) printers, copying machines, facsimile machines, whether or not combined;

(ii) apparatus for the transmission or reception of voice, images or other data, including apparatus for communication in a wired or wireless network Ouch as a local or wide area network);

(iii) loudspeakers and microphones;

(iv) television cameras, digital cameras and video camera recorders;

(v) monitors and projectors, not incorporating television reception apparatus.”

1.60 The Moving Style, as described, is not presented as any of these standalone articles, rather, it is an integrated, freely programmable ADPM running Tizen operating system with CPU, RAM, storage, touch input, and application execution capability.

1.61 The Moving Style is not a printer, copier, or fax machine, nor is it presented as such. It is a touch-enabled smart device that combines display and computing capabilities. While the device includes Wi-Fi and Bluetooth modules for connectivity, it is not presented as a communication apparatus as well. These modules serve to support the general-purpose ADP environment for functions such as app downloads and cloud access, rather than defining a standalone telecom function. Similarly, although the device contains integrated speakers and a microphone, it is not presented as loudspeakers or microphones, rather these components are integral I/O elements that enable voice input and multimedia playback within the ADP framework. The Moving Style is also not a camera or camcorder; it is a touchscreen ADP device with no independent camera module as its defining feature.

1.62 The Moving Style is also not presented merely as a monitor/projector. It integrates an OS (Tizen), CPU (Quad-core), RAM (4GB), eMMC (16GB), and allows app installation/deletion and web/cloud execution, which exceeds the scope of a passive display. Its touch interface, virtual keyboard, and voice input further underscore that it is an ADP machine, not a standalone monitor. Thus, the Moving Style is not presented separately as any of the items listed in Note 6(D), and is instead an integrated, freely programmable ADP device, therefore, the exclusion of Note 6(D) does not apply to Moving Style and thus does not exclude it from Heading 8471.

1.63 Now, attention is invited to Note 6(E) to Chapter 84 which provides that “Machines incorporating or working in conjunction with an automatic data processing machine and performing a specific function other than data processing are to be classified in the headings appropriate to their respective functions or, failing that, in residual headings.”

1.64 This provision establishes the specific function principle, meaning that if a machine integrates ADP capability but its primary function is something other than general-purpose data processing, classification must follow the heading that corresponds to that specific function.

1.65 Note 6(E) provides that machines incorporating or working in conjunction with an ADP machine, but performing a specific function other than data processing, must be classified by that specific function (or, failing that, in a residual heading). In practice, this exclusion targets devices whose principal purpose is single-function, non-ADP work like printing, measuring, recording, etc, where an embedded processor or attached computer is merely incidental and subordinate to that function. The test, therefore, is whether the machine’s defining character is a distinct operational function (other than data processing), or whether it is a general-purpose, freely programmable ADP platform whose functions are software-defined and user-selected.

1.66 The Moving Style is used just like a compact computer that lets users work with information, documents, apps, and online content directly on the device. It runs on its own operating system (Tizen OS) and allows users to create, edit, save, and manage documents, access files from USB or the network, and even work on cloud platforms such as Microsoft 365. The device also supports installing and deleting apps, browsing the internet, logging into remote PCs, and mirroring content from phones and laptops. It processes user inputs through the touchscreen, virtual keyboard, and voice commands, and provides outputs through its display and speakers. These everyday functions like typing documents, opening spreadsheets, editing files, running apps, and working online show that the Moving Style is doing active data processing, not just displaying information. Since the users can perform a wide range of computing tasks on it independently, the Moving Style functions as an ADP machine, rather than merely a display device.

1.67 The Product operates as a freely programmable, general-purpose computing device that processes data in its own operating environment (Tizen OS) using an integrated CPU, RAM, and internal storage to run user-selected applications, manipulate files, and execute cloud/web workloads. In other words, the Product utilizes its own operating system that enables document creation saving deleting, and editing, content import/export via USB/network, and also apps can be installed and deleted. Further, a user can remotely access PC and edit PC data and edit documents through cloud-based applications such as Office 365.

1.68 Taken together, these capabilities demonstrate the following ADPM characteristics:

- Continuous data input through touch, voice, virtual keyboard and peripheral ports;

- Data processing through local apps and browser-based / remote applications), and

- Data output through on-screen rendering and audio

1.69 All the above functions are performed stand-alone without reliance on an external ADP host. The device’s support for installation/deletion of applications, document editing, networked content exchange, and runtime handling of program logic (e.g., in browser and streaming clients) evidences the four functional hallmarks of automatic data processing rather than any other fixed / specific function, thereby establishing that Moving Style qualifies as an ADPM under Heading 8471.

1.70 The Moving Style is designed as a freely programmable ADP device. It runs on Tizen OS and users can install and delete applications, execute cloud/web apps, and perform a wide range of ADP tasks (document creation/editing, remote PC access). These features demonstrate that the Device’s core function is general data processing under user control, not a predefined non-ADP task. Its touchscreen, virtual keyboard, voice input, Wi-Fi/Bluetooth, HDMI/USB-C ports all serve as Input / Output pathways for diverse applications rather than binding the device to a single specific function.

1.71 While the device supports OTT streaming and functions as a display, these are application domains executed within the ADP environment not standalone specific hardware functions that displace the classification under ADPM. Streaming relies on software clients, adaptive logic, and network services; it is user-selected and software-driven, just like document editing or remote access. These capabilities do not recharacterize the product as a specific-function audiovisual apparatus. Instead, they show the breadth of tasks a general-purpose ADP machine can perform. Consequently, Note 6(6) does not divert classification away from Heading 8471.

1.72 Reliance is placed on the case of Bright point India Pvt. Ltd. (supra) wherein the Authority emphasized that classification must follow GR1 Rule 1 and that Heading 8471 covers ADPM which meet all four conditions of Note 6(A). In assessing the View Board, CAAR found that the goods have an in-built CPU, RAM, a pre-installed operating system (Android 7.0), and an OPS slot enabling installation of other operating software (e.g., Windows); therefore the device stores programs and data (Note 6(A)(i)), is freely programmable (Note 6(A)(ii)), performs arithmetic computations specified by the user (Note 6(A)(iii)), and executes programs with logical decisions without human intervention (Note 6(A)(iv)).

1.73 CAAR concluded that the View Board is “much more than mere display devices” and that display is only one feature, not the principal function; the product is an ADP machine itself rather than a unit of an ADP system or a monitor under 8528. The Authority explicitly noted that, in standalone configuration, these devices join wired/wireless networks, access/manipulate files, and perform general computing tasks (browsing, email, office editing), thereby ‘fitting Heading 8471 41 90 (comprising in the same housing at least a CPU and input/output units).

1.74 Likewise, in the case of Ingram Micro (supra), it was held that Interactive Flat Panels, despite large screens, are ADP machines: they have CPU, RAM, storage, Android OS, can download/install programs, perform computations, and execute programs with logical decisions, meeting the requirements of Note 6(A) and therefore falling under 8471 41 90;

1.75 Given the above, we are of the view that the subject goods are appropriately classifiable under HSN 8471 as “Automatic Data Processing Machines and units thereof; Magnetic or optical readers, machines for transcribing data on to data media in coded form and machines for processing such data, not elsewhere specified or included”. and more specifically under subheading 8471 41 90 as “Other automatic data processing machines: Comprising in the same housing at least a central processing unit and an input and output unit, whether or not combined: Other”.

Question 2: Whether the Floor stand imported with the Moving Style in the same or different shipment merit classification under HSN 8473 as “Parts and accessories (other than covers, carrying cases and the like) suitable for use solely or principally with machines of headings 8470 to 8472”.

1.76 The Applicant intends to import and sell the Moving Style in India. For such purposes, the Applicant proposes to import the Moving Style along with its ‘Stand’ into India, where the main device and the stand would be imported simultaneously, in a single shipment. The Moving Style comprises of 2 main components, namely: (1) Main Device and (2) Stand. It is stated that the Stand comes with a pre-defined mounting arrangement, where the main unit of the Moving Style is placed to be used in standing / movable form. The use of Stand is optional, depending on the needs of customer. In cases, where the Moving Style is required to be installed in standing or mobile form, the use of Stand is essential to the intended use. Further, no additional processing is required whatsoever for the Moving Style in its complete form to come into existence. Further, the function of the Moving Style is to perform data processing functions through its built-in CPU, OS and memory, and to enable the user to run applications and process information through an interactive display interface.

1.77 The Stand supplied with the Moving style is a dedicated support and mobility structure that forms part of the product package. The Stand is a standard supplied component along with the Main unit. It is intended to function as a floor-standing movable base for the screen. The Main Unit can be mounted onto the stand or detached from it, and that the stand includes wheels at its bottom surface to enable the user to move the screen easily from one location to another. This indicates that the stand’s primary purpose is to provide stable support and mobility for the Moving style display in a “stand-up / movable” configuration.

1.78 The product literature also clarifies that the stand is not necessary for basic “upright placement” of the screen in all circumstances. Specifically, it states that the screen itself has a built-in support (a self-standing support/kickstand), allowing the screen to be placed and fixed in a standing position even without attaching it to the wheeled stand. This reinforces that the stand is an optional convenience accessory for mobility and placement and is not required for the device’s core operation.

1.79 The Stand is described as the mounting/mobility base used to attach/detach the Moving style screen and move it via wheels. It is not a universal stand compatible with multiple brands or models; instead, it is presented as the stand supplied with and intended for the Moving style rather than as a generic/common stand.

1.80 Attention is invited to the case of Commissioner of Central Excise, Delhi v. Insulation Electrical (P) Ltd, wherein the Hon’ble Supreme Court has drawn a clear distinction between a “part” and an “accessory” by applying the test of essentiality, i.e., whether the main article can function without the item in question. While deciding whether seat slider/rail assemblies are “parts” of seats or “accessories,” the Court approved the reasoning that where the seat remains complete and functional without such mechanisms, they cannot be treated as parts. The Court observed that these mechanisms are “only adjuncts… merely to improve the efficiency and convenience of the seat and does not form part of the seat,” and that “A ‘part’ is an essential component of the whole without which the whole cannot function.” The Supreme Court in the end concluded that the items in dispute were not “parts” because the principal article (the seat) could function even without them; they merely facilitated comfort and convenience. Specifically, the Court affirmed that the seat is “complete in themselves without these mechanisms” and therefore the items “can at best be termed as accessories.”

1.81 In the case of Pragali Silicons Pvt. Ltd. v. Commissioner of C. Ex., Delhi, the Supreme Court elaborated the meaning of “accessory” and clarified that an accessory is not required to be essential for the functioning of the main product. The Court noted that “an ‘accessory’ by its very definition is something supplementary or subordinate in nature and need not be essential for the actual functioning of the product.” This definition is important because it recognizes that even where an item is not indispensable, it may still be classifiable as an accessory if it adds convenience, effectiveness, or value to the main article. The Supreme Court also approved the broader test (drawn from earlier precedents) that an accessory is something that adds to the “convenience or effectiveness” of another product, even if the product can function without it. The judgment includes the understanding that an accessory is an “article or device that adds to convenience or effectiveness of, but is not essential to, main machinery,” and that the ordinary/common purpose and use can guide this determination.

1.82 Applying the above judicial principles, the stand supplied for The Moving style should be treated as an accessory. The Moving style is a complete smart device capable of performing its core functions (data processing, app execution, OTT streaming, productivity tasks) independent of the stand; the stand primarily enables the “stand-up/movable” convenience and improves placement and usability. Under the Supreme Court’s settled tests, where the main product is complete and functional without the item, the item cannot be a part” (essential component), and at best is an accessory that enhances convenience/effectiveness.

1.83 Now, for determining the HSN classification, the Rule 1 of GIR provides basis for classification of an imported good. The classification shall be determined according to the terms of headings and any relative Section or Chapter Notes. The relevant text is reproduced as under:

“1. The titles of Sections, Chapters and sub-chapters are provided fir ease of reference only; fir legal purposes, classification shall he determined according to the terms of headings and any relative Section or Chapter Notes and, provided such headings or Notes do not otherwise require, according to the following provisions:”

1.84 Reference is drawn to the Heading 8473; the text of such Heading reads as under:

| 8473 | PARTS AND ACCESSORIES (OTHER THAN COVERS, CARRYING CASES AND THE LIKE) SUITABLE FOR USE SOLELY OR PRINCIPALLY WITH MACHINES OF HEADINGS 8470 TO 8472 |

1.85 Thus, upon plain reading of text of 1-leading 8473, accessories which are designed for use solely or principally with machine classifiable under Headings 8470 — 8472, would be classifiable under the Heading 8473.

1.86 Therefore, per Rule 1 of GIR, it can be concluded that accessories which are designed for use solely or principally with machine classifiable under Headings 8470 — 8472, would always be classifiable under the Heading 8473.

1.87 In the aforesaid Paragraphs, it has been concluded that the Moving style would merit classification as an ADPM classifiable under the I-ISN 8471 4190.

1.88 The Stand is an accessory to the Moving style, provided the Customer desires to use the stand option. Further, it is designed to function solely / principally with the Moving style’. In this regard, the Explanatory Notes of Heading 8473 would be germane. The relevant text is reproduced as under:

“But the heading excludes covers, carrying cases and felt pads; these are classified in their appropriate headings. It also excludes articles of furniture (e.g., cupboards and tables) whether or not specially designed fir office use (heading 94.03).

However, stands for machines of headings 84.70 to 84.72 not normally usable except with the machines in question, remain in this heading.”

1.89 Thus, basis the Explanatory Note to Heading 8473, a stand would be covered under this heading where it is not normally usable except with the machine in question. By analogy and applying the same interpretative principle, where a stand is designed solely / principally for use with an ADP machine classifiable under Heading 8471, it would be appropriately classifiable as an accessory suitable for use solely or principally with such machine under Heading 8473.

1.90 In the present case, the Stand has been designed to be used solely / principally with the Moving Style. Therefore, the Stand, when imported on a standalone basis, would be classified as a part/accessory suitable for use solely or principally with a machine of Heading 8471, under HSN 8473 (typically under the residual sub-heading for parts and accessories of ADPM, i.e., 8473 30 99 “Other”, as applicable under the Indian Tariff.

Conclusion

1.91 The ‘Moving Style’ is classifiable under the HSN 8471 as “Automatic Data Processing Machines and units thereof; Magnetic or optical readers, machines for transcribing data on to data media in coded form and machines for processing such data, not elsewhere specified or included” A.1.1. and more specifically under subheading 8471 41 90 as “Other automatic data processing machines: Comprising in the same housing at least a central processing unit and an input and output unit, whether or not combined: Other”.

1.92 The ‘Stand’ is appropriately classifiable as an accessory suitable for use solely or principally with the Moving style ADP machine under Heading 8473 (Parts and accessories of the machines of heading 8471), as it is not an essential “part” without which the Moving style cannot function, but a supplementary item that enhances usability (stand-up/mobility) and is designed for principal use with the Moving style. Accordingly, the Stand would be classifiable under HSN 8473 (typically under the residual entry for parts/accessories of machines of heading 8471, i.e., 8473 30 99 — “Other”, as applicable under the Indian Tariff).

1.93 It is thus humbly prayed that an adjudication may be pronounced in respect of all of the aforesaid Questions submitted to the Customs Authority for Advance Rulings, in terms of Chapter VB, Customs Act

2. Comments of Custom Port Commissionerate:

2.1 As per the provision of CAAR Regulation, 2021, the complete application of the applicant was provided to the concerned Custom Port, and requested to furnish the requisite comments in the instant matter. The port authority vide their letter dated 08.05.2026 furnished their comments, which are reproduced as under:

In this regard, necessary comments are as follows:

(i) Eligibility of the applicant, in terms of Section 28-E (c) of the Customs Act, 1962, to seek such advance ruling.

Yes, M/s Samsung India Electronics Private Limited is a valid applicant within the meaning of Section 28E (c) (i) of the Customs Act, 1962, having IEC Code No. 595032818.

(ii) Applicability of proviso (1) of Section 28-1(2) of the Customs Act, 1962, regarding the question raised in the application.

As per records available in the Section, no such case of the applicant is pending with any officer of the Customs, other Appellate Tribunal or any Court under the proviso of Section 28(1) (2) of the Customs Act, 1962.

(iii) Specify whether the claim of the applicant regarding the nature of the activity, i.e. it is ongoing/proposed, is correct;

As per the submissions made by the applicant, Importer intends to import ‘Moving Style’ into India.

(iv) Comments on the merit of the question raised in the application, along with all materials in support thereof;

A. Nature of activity proposed to be undertaken- Importer intends to import ‘Moving Style’ into India for further sale. It has been further submitted no processing whatsoever would be carried out on the imported goods, post importation into India.

B. Question of Law or fact;

a. Whether ‘Moving Style’ Imported into India would merit classification under HSN 8471 as Automatic Data Processing Machines and units thereof; Magnetic or optical readers, machines for transcribing data on to data media in coded form and machines for processing such data, not elsewhere specified or included”

b. Whether the Floor stand Imported with the Moving Style In same or a different shipment merit classification under HSN 8473 as Parts and accessories (other than covers, carrying cases and the like) suitable for use solely or principal with machines of headings 8470 to 8472″,

Comments in respect of aforementioned questions a & b-

The subject item “Moving Style’ is described by Samsung as a LCD touchscreen with cover glass, Detachable screen, wheeled floor stand, built-in battery, Quad-core processor, RAM, internal storage, Tizen OS (Samsung’s smart TV/platform OS). It is having connectivity facility such as HDMI, USB-C, Wi-Fi, Bluetooth, screen mirror infect. It can Install/delete apps via Tizen app store, stream OTT, video/music playback. It is having built-in speakers & microphone.

Intended Use of the said product: Collaborative workspaces, educational settings, home entertainment, meetings, presentations mobility. “Next-Gen Office Display Solution” with

Hence, it is explicitly positioned as a hybrid smart device bridging a smart display and interactive computing system.

In view of the above, the subject item seems to be a movable interactive display panel (Interactive Flat Panel) which is rightly classifiable under CTH 8528.

Moving Style is not a conventional laptop or desktop PC. It is a mobile variant of an Interactive Flat Panel Display (IFPD). The addition of wheels does not change its essential character as an interactive display unit for group viewing and collaboration.

Relevant Tariff Headings for the subject item-

CTH 8471 (claimed by the importer): Automatic data processing machines and units thereof… not elsewhere specified or included.

CTH 8528 (Department’s view): Monitors and projectors, not incorporating television reception apparatus… (including 8528 59 00- Other monitors).

As per chapter note 6(D) to Chapter 84, heading 8471 does not cover monitors and projectors not incorporating television reception apparatus when presented separately even if they meet ADP conditions.

Further as per Note 6(E): Machines incorporating or working in conjunction with an ADP machine and performing a specific function other than data processing are classified in the headings appropriate to their respective (principal) functions (or residual headings).

Heading 8528-Monitors and projectors, not incorporating television reception apparatus… 8528.52-Capable of directly connecting to… ADP of 84.71 8528.59 – Other (other monitors).

The principal function of subject goods is display interactive presentation (touchscreen output for groups), not standalone general-purpose data processing like a PC. Computing elements (processor, OS, RAM) enable the display/interaction but do not override this.

Section XVI, Note 3: Unless the context otherwise requires, composite machines consisting of two or more machines fitted to form a whole and other machines designed for the purpose of performing two or more complementary or alternative functions are to be classified as if consisting only of that component or as being that machine which performs the principal function. “The principle function of the subject item is to interact through display and hence classifiable under sub-heading 8528.

Importer emphasizes that Tizen OS, quad-core processor, RAM/storage, app installation, document editing, etc meets Note 6(A) criteria for ADPM (storing programs, freely programmable, arithmetic, logical decisions).

However, many “monitors” or interactive panels have embedded processors/OS for smart features (e.g., Android TVs, smart displays) but remain classified under 8528 when the primary purpose is display/output. Even though the functions of an ADP machines are inbuilt, the subject goods viz. Interactive Display Unit/ Interactive Flat/Intelligent Panel cannot be considered as a simple input or output device and is to be identified with its primary function of display by applying Note 6 (E) of Chapter 84.

On similar issue, the decisions held by Apex Court and Hon’ble Tribunal are referred as under:

a. Hon’ble Supreme Court in the case of Commissioner of Customs, Bangalore Vs. N.1. Systems (India) P. Ltd. 2010 (256) ELT 173 (SC) wherein Hon’ble Court held that, “…PXI Controller which was a computer based instrumentation product and capable of being controlled by a Personal Computer/Laptop but is not a PC/laptop-principal function of controllers is executing control algorithms for real-time monitoring and control of devices-controller performs functions in addition to data processing – what is imported is a system containing an ADPM and if the contention of the importer herein is accepted, it would mean that every machine, that contains an element of ADP would be classifiable as an ADP machine under Chapter 84 which would completely obliterate the specific function test and the concept of functional unit. Hon’ble Court upheld the classification of the department and held that goods were rightly classified under Chapter 90…” The same principle applies to this case.

b. Hon’ble CESTAT, New Delhi in the case of Commissioner of Customs (Import & General), New Delhi Vs. Integral Computer Ltd. – 2016 (337) ELT 580 (Tri-Del) dated 07.04.2016 wherein Hon’ble Tribunal has held that, “Interactive Electronic White Board” is a teaching device mainly used for class room teaching or in conferences and meetings and work and gets the display function by combined action with a computer and projector cannot be considered as a simple input or output device and is to be identified with its primary function of display and has classified the goods under sub-heading 8528 5100 Le. other monitors (now CTH 85285900)”. The issue is squarely covered in the present case.

Conclusion

The device is marketed and used as a movable interactive panel, not a general-purpose computer. It bridges “smart display and interactive computing” but remains display-centric. Hence, ‘Moving Style’ is a type of Interactive Flat/Intelligent Panel (mobile variant). As per Chapter Notes 6(D) & 6(E), Section Note 3, principal function test, it merits classification under CTH 8528 59 00 (“other monitors”), not 8471 and parts of the same are classifiable under CTI–1 8529. Importer’s submission over-emphasizes embedded computing while ignoring the display-centric design, use case, and explicit exclusions in the tariff notes.

(v) Whether the question raised is pending before any Officer of Customs, the Appellate Tribunal or any Court:

As per records available in the Section, no such case of the applicant is pending with any officer of the Customs, other Appellate Tribunal or any Court.

3. Personal Hearing:

Personal hearing in the matter was conducted on 08.06.2026 wherein the authorized representatives of the applicant i.e. Ms. Divya Bhushan, Ms. Ekta Ghildiyal and Mr. Abhishek Kumar Singhania, attended the same and reiterated the same which were already submitted with the application of the applicant. The representatives submitted that the subject product is distinguishable from an Interactive Flat Panel Display (IFPD) on account of several technical characteristics, including its smaller screen size (27 inches), resolution lower than 4K, absence of high-quality built-in speakers, and lower power consumption. The representatives further contended that the product is essentially a large-sized Wi-Fi-enabled tablet and emphasized that the aforesaid specifications are intrinsic characteristics of the product and will remain unchanged. The representatives also filed additional written submissions in rebuttal to the comments Furnished by the Port Commissionerate.

In response to a query regarding previous imports of the subject goods, the representatives informed the Authority that importation of the product has already commenced through Chennai Port. The representatives undertook to furnish the relevant 13111 of Entry for the Authority’s consideration.

No representative appeared on behalf of the Department.

4. Additional Submissions of the Applicant:

4.1 Under the instructions and on behalf of the Applicant viz, Samsung India Electronics Private Limited, the present Additional Submissions have been filed.

4.2 For the sake of brevity, the entire facts stated in the Application are not stated. However, the Applicant craves leave to refer & rely upon the Statement of Facts & Grounds raised in the Application. The same may be treated as part of these additional submissions.

4.3 The Applicant intends to import ‘Moving Style’ into India for further sale. It is further stated that no processing whatsoever would he carried out on the imported goods, post importation into India.

4.4 The concerned Jurisdictional Office (hereinafter referred to as ‘Department’) has offered comments via letter dated 08 May 2026, on the Advance Ruling Application filed by the Applicant.

4.5 The case of Department is summarised as under:

(i) The Port has examined the nature and functionality of the product “Moving Style” and has described it as a device comprising an LCD touchscreen, detachable screen, wheeled floor stand, built-in battery, processor, RAM, internal storage and operating system, along with connectivity features such as HDMI, USB-C, Wi-Fi and Bluetooth. The Port notes that the product supports app installation, OTT streaming, playback functions, and includes built-in speakers and microphone. Based on the intended usage in collaborative workspaces, educational settings, home entertainment, meetings and presentations, the Department has characterised the product as a “hybrid smart device” bridging a smart display and interactive computing system.

(ii) Acknowledging and accepting the aforementioned embedded computing features, the Port is of the view that the subject goods are essentially a “movable interactive display panel” or “interactive flat panel”, and not a conventional laptop or desktop computer. The Department has emphasized that the addition of mobility through wheels or embedded processing capability does not alter the essential nature of the product as a display-oriented device. Accordingly, it has been stated that the goods are more appropriately classifiable under Heading 8528 as “other monitors”, rather than under Heading 8471 as claimed by the Applicant.

(iii) The Port has placed reliance on Chapter Note 6(D) and 6(E) to Chapter 84 to support its classification view. It has stated that Note 6(D) excludes monitors from Heading 8471 even if they satisfy conditions of ADP machines, and Note 6(E) provides that machines performing a specific function other than data processing should be classified according to their principal function. Applying these provisions, the Department has concluded that the principal function of the product is display and not general-purpose data processing.

(iv) The Department has further stated that although the product contains elements such as processor, operating system, RAM and storage, these are only supportive of the display and interaction functions and do not override the core character of the product. It has observed that several modern display devices incorporate smart features or embedded computing but continue to remain classified as monitors where their primary purpose remains display centric.

(v) In support of its position, the Port has relied on judicial precedents including the decision of the Hon’ble Supreme Court in Commissioner of Customs v. N.I. Systems (India) Pvt Ltd. and the decision of the Hon’ble CESTAT in Integral Computer Ltd., to contend that the presence of data processing capability does not automatically render a product classifiable as an ADP machine, and that classification should be based on the principal function of the goods.

(vi) Based on the above reasoning, the Department has concluded that the subject goods merit classification under CTH 8528 59 00 as “other monitors”, and accordingly, any parts or accessories associated with the product would be classifiable under Heading 8529 instead of Heading 8473 as claimed by the Applicant.

4.6 The Applicant respectfully disagrees with the comments filed by the Department. Further, the Applicant craves the leave of the Hon’ble Authority to file Additional Submissions, in rebuttal to the comments filed by Department. It is requested that such Additional Submissions may be taken on record and be treated as part of the original Application.

A. Response to Comments received from Port

A.1. Fundamental flaw in the Department’s characterisation of the product

A.1.1.The Department has proceeded on an entirely erroneous factual premise by characterizing the subject goods and pre judging the classification outcome under Heading 8528. Such characterisation is not borne out from the technical specifications, functionality, and usage of the product as placed on record by the Applicant. The product in question is not merely a dis. . device enhanced with certain smart features, but is, in substance and design, a self-contained, standalone computing machine capable of independent data processing, execution of applications, and user-driven programmability without any reliance on external computing infrastructure.

A.1.2. It is submitted that the Department has selectively focused on the presence of a display screen while ignoring the core computational architecture of the device, including its embedded processor, operating system (Tizen OS), memory, storage, and execution environment. This selective analysis leads to a distorted understanding of the product and directly impacts the application of the correct tariff entry. The process of classification of any good is such that goods must be assessed in their entirety, considering all their essential characteristics, and not on the basis of a singular feature. Therefore, the initial premise adopted by the Department is fundamentally flawed and vitiates the entire reasoning.

A.2. Conclusive satisfaction of Note 6(A) to Chapter 84

A.2.1. The classification under Heading 8471 is primarily governed by Note 6(A) to Chapter 84, which lays down four cumulative and exhaustive conditions for a device to qualify as an ADPM. The Applicant has already demonstrated in detail that the subject goods unequivocally satisfy all four conditions, and notably, the Department has not disputed this factual position in its comments.

A.2.2. The Moving Style is equipped with internal storage and memory enabling it to store operating programs and data required for execution. It operates on Tizen OS, which allows for installation, deletion, and execution of applications, thereby fulfilling the requirement of being freely programmable. Further, the device performs arithmetic and logical operations through applications such as spreadsheets, browsers, and productivity tools, thereby satisfying the computational requirement.

A.2.3. Additionally, the device executes processing programs autonomously and is capable of modifying execution paths based on logical decisions during runtime, such as adaptive streaming, background processing, and application-based workflows. These functional cities clearly establish compliance with the fourth conditions under Note 6(A). Since all four conditions are cumulatively satisfied, the product must be classified under Heading 847 I , and no further subjective assessment is required as the product satisfies conditions of Note 6(A), it qualifies as an ADM as a matter of law, and any attempt to reclassify it under another heading without any justification is impermissible.