The objective of this document is to summarize all the tax concessions, applicable w.e.f FY 2019-20, announced by Finance Minister, Nirmala Sitharaman with intent to boost the economy and to promote ‘Make-in-India’.

Highlights of Tax Concessions by Finance Minister press Conference on 20 Sep 2019

1. Tax Concessions for Existing Domestic Companies.

1.1. Option has been given to existing domestic companies to pay corporate tax @22% and the same are not required to pay MAT

1.2. MAT has been reduced from 18.5% to 15% for companies which continue to avail tax exemptions/incentives

2. Tax Concessions for New Domestic Companies.

Option has been given to pay corporate tax @15% to domestic companies incorporated on or after 01-Oct-2019 making fresh investment in manufacturing and the same are not required to pay MAT

3. Enhanced surcharge of 25%/37% shall not be applicable on tax payable on capital gains arising from transfer of certain securities.

4. No tax on buy back of shares in the hands of listed companies announced buy-back of shares prior to 05-July-2019

5. Going forward the amount spent by corporate on incubators run by public sector undertakings (PSUs) shall also be considered as part of CSR expenditure.

1. Tax Concessions for Existing Domestic Companies

1.1. Option has been given to existing domestic companies to pay corporate tax @22% and the same are not required to pay MAT

- To promote growth and investment in India, an option has been given to all existing domestic companies to pay corporate tax @ 22%.

- Thereby, the effective tax rate shall be 25.17% (i.e. tax inclusive of surcharge & cess).

- The companies who opt for 22% tax rate shall not avail tax incentives or exemptions (such as tax holiday for start ups, exemptions to SEZ etc..,) under any other provisions of the Act.

- However, they can opt for 22% tax rate after the expiry of tax holiday or exemption period. Till such period they shall be liable to pay tax @ 25%/30%.

- Option once exercised can’t be withdrawn.

- Also, companies who opt for 22% tax rate are not required to pay minimum alternate tax (MAT)

1.2. MAT has been reduced from 18.5% to 15% for companies which continue to avail tax exemptions/incentives

2. Tax Concessions for New Domestic Companies.

Option has been given to pay corporate tax @15% to domestic companies incorporated on or after 01-Oct-2019 making fresh investment in manufacturing and the same are not required to pay MAT

- To attract fresh investment in manufacturing and to boost “Make-in-India”, an option has been given to domestic companies incorporated on or after 1st October, 2019 to pay corporate tax @ 15%.

- Thereby, the effective tax rate shall be 17.01% (i.e. tax inclusive of surcharge & cess).

- Companies should be incorporated by making fresh investment in manufacturing activity and production should be commenced on or before 31st March, 2023.

- However, these companies shall not avail tax incentives or exemptions under any other provisions of the Act.

- Also, these companies are not required to pay minimum alternate tax (MAT)

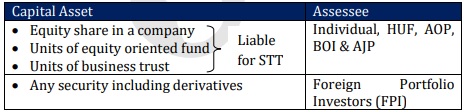

3. Enhanced surcharge of 25%/37% shall not be applicable on tax payable on capital gains arising from transfer of certain securities

To stabilize the flow of funds into the capital market, Central Government withdraws enhanced surcharge from the FY 2019-20 (AY 2020-21) on tax payable on transfer of capital assets as mentioned below:

4. No tax on buy back of shares in the hands of listed companies announced buy-back of shares prior to 05-July-2019

4. No tax on buy back of shares in the hands of listed companies announced buy-back of shares prior to 05-July-2019

5. Going forward the amount spent by corporate on incubators run by public sector undertakings (PSUs) shall also be considered as part of CSR expenditure

Thank you for the patient reading. Hope this document has added value to your knowledge.

For feedback or comments, please write to jnr@cajvk.in

Disclaimer:

This document had been written to provide updates under Income Tax in a simple manner. The author shall not be responsible for any of the decision made based on the contents of this document.