Any payment or any remittance is done to a Non-resident is subject to many rules and regulations. Initially, when an individual user to make payment or remittance to Non-Resident, he was bound to furnish a certificate in a standard format specified by RBI. The purpose behind collecting the taxes at the time of the remittance is to avoid a situation where it becomes difficult or impossible to collect the tax from the NRI later.

Now in order to check and track the transactions in a well- manner, re-filling of data in the certificates is introduced.

Section 195 of the Income tax act, 1961 makes it compulsory to deduct the Income-tax from payments made to Non-Resident. The person making payment/ remittance to non – resident holds the responsibility to furnish an undertaking (in form 15CA) attested by a Chartered Accountants Certificate in Form 15CB. So when a person has to make any payment or remit any money to non-resident, the bank will have to verify the payment of tax and act accordingly.

Section 195 of the Income tax act, 1961 makes it compulsory to deduct the Income-tax from payments made to Non-Resident. The person making payment/ remittance to non – resident holds the responsibility to furnish an undertaking (in form 15CA) attested by a Chartered Accountants Certificate in Form 15CB. So when a person has to make any payment or remit any money to non-resident, the bank will have to verify the payment of tax and act accordingly.

For the deduction of tax, there are certain tax slabs, formed for different specific amounts on which tax is levied and two Forms, Form 15CA, and Form 15CB for two different cases, which has to be submitted online duly filled.

The Form 15CA has to be furnished online by a person making any remittance of foreign nature to a non-resident. The Form 15CB regulates the tax deduction as per the income tax rules and also prohibits the double tax provision. The filing of Form 15CB requires an attestation from a chartered accountant.

In Form 15CB, we are required to mention information like details of the remittee, details of the remitter, nature of remittance including royalty, salary, commission etc, Tax Residency Certificate and Bank details of the remitter from the remitter in the case of DTAA (Double Taxation Avoidance Agreement).

But there are at least 28 types of foreign remittance where you do not require any submission of Form 15CA or Form 15CB

Page Contents

What is Form 15CA?

A person making the remittance (a payment) to a Non Resident or a Foreign Company has to submit the form 15CA. This form is submitted online.

Form 15CA is a declaration of remitter which is used as a mechanism for collecting information in respect of payments which are liable to tax on behalf of recipient non-resident. This form assists the Income Tax Department in keeping eye on foreign remittances & their tax accountability. The Rule 37BB defines it as a duty of authorized dealers/banks to confirm the receptivity of such forms from the remitter.

E-filing of this form is an initiative for an effective & efficient Information Processing System which would facilitate the Income-tax Department greatly in tracking the foreign remittances accurately and effortlessly.

The Financial Institutions are now keeping a hawkeye on all such transactions and forms prior to the effectiveness of remittance. The revised Taxation Rule, 37BB, binds all the Financial Institutions to furnish Form 15CA to an income-tax authority for further proceedings after receiving it from remitter.

Applicability and parts of Form 15CA

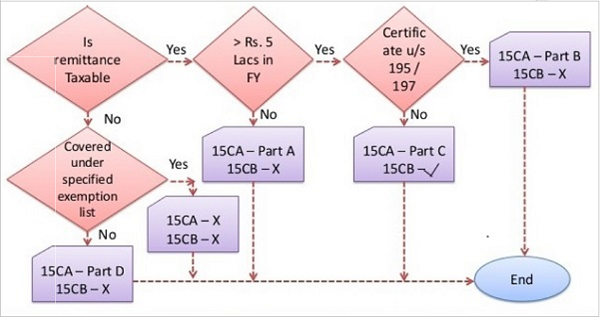

It should be kept in mind that Form 15CA is not needed to be filed when the remittance paid to a Non-resident is non taxable which interprets that the Form 15CA is filled up only when the remittance paid to a non-resident is taxable and does not surpass an amount of fifty thousand rupees and the aggregated remittance for the Financial year does not exceed two lakh fifty thousand rupees.

Note: Government has authorized the filing of 15CA/15CB via GenTDS Software.

Parts of Form 15CA

- Part A – Part A of the Form is required to be filed when the remittance amount is taxable under the income tax Act 1961 and the aggregate of remittance exceeds Five lakh rupees in that particular F.Y.

- Part B – Part B of the Form 15CA is needed to be filled when the remittance amount exceeds five lakh rupees in the F.Y. and when an order /certificate u/s 195(2)/ 195(3)/197 of Income Tax Act has been acquired from the A.O. (Whether Nil rate or Lower rate Certificate).

- Part C- Part C of the Form 15CA is needed to be filled when the remittance amount in the F.Y. exceeds Five Lakh rupees during the F.Y. and a certificate in Form No. 15CB from an accountant as stated in the description below sub-section (2) of section 288 has been obtained.

- Part D – The Part D of Form 15CA is filled when the remittance is not taxable other than payments referred to in rule 37BB(3) by the person referred to in rule 37BB(2).

Note:

- It is to mandatory to upload Form 15CB before filling Part C of Form 15CA. To present the details in Part C of Form 15CA, the acknowledgment number of e-Filed Form 15CB should be given.

- Form 15CB is to be filled only when the remittance amount exceeds Rs 5 Lakh during the F.Y. under the income tax act 1961.

- The online filing of 15CA/15CB as per XML based latest scheme generation and uploading are also compulsory.

You will receive a message on your screen and a confirmation email in your registered email account once you finish the entire process.

Filling Guidelines of Form 15CA

- The Form 15CA should be appropriately filled, signed, and submitted to the Reserve Bank of India or an authorized dealer before making the Remittance.

- The Form should be submitted duly filled, at the official website of the Tax Information Network (www.tin-nsdl.com).

- The details like PAN number, TAN number should be mentioned correctly in the Form. The complete and accurate details of the Remitter, the Remittance, and the Recipient of the Remittance should be furnished in the form.

- The Accountant for handling the form filling process and attesting the TDS Certificate should be appointed according to the definition given by Section 288 of the Income Tax Act of 1961.

What is Form 15CB?

15CB is the Tax Determination Certificate where the CA verifies the remittance with respect to the liability provisions under Section 5 and 9 of the Income Tax Act coupled with the provisions of Double Tax Avoidance Agreements. In this form, a C.A. validates the details of the payment, TDS rate and TDS deduction as per the norms mentioned in Section 195 of the Income Tax Act, if any DTAA is applicable, and other details of nature and purpose of the remittance.

Form 15CB liability could be examined by accessing the certificate obtained from a CA in the Form 15CB. The requirement of the certificate has been stated and prescribed in Section 195(6) of the Income-tax Act.

Documents required for Form 15CA and 15 CB:-

A. Details of Remitter

- Remitter’s Name

- Remitter’s Address

- Remitter’s PAN Number

- Principal Place of Business of the Remitter

- E-Mail Address and Phone No. Of Remitter

- Status of the Remitter (Firm/Company/Other)

B. Details of Remittee

- Name and Status of the Remittee

- Address of the Remittee

- Principal Place of Business

- Country of the Remittee

C. Details of the Remittance

- Country to Which Remittance Is Made

- Currency in Which Remittance Is Made

- Amount of Remittance in Indian Currency

- Proposed Date of Remittance

5. Nature of Remittance as Per Agreement (Invoice Copy to Be Asked From Client)

D Bank Details of the Remitter

- Name of Bank of the Remitter

- Name of Branch of the Bank

- BSR Code of the Bank

E. Others

- Father’s Name of the Signing Person

- Designation Of The Signing Person

Here are a few major impacts of New Rule on 15CA & 15CB in short:

Applicable since 1st October 2013

- The applicability of Part A of Form 15CA nullifies the applicability of the Form 15CB. Ex, the case of small payments.

- 28 types of payments require no information to be furnished in the form.

- For other types of payments, either an order or a certificate of the Assessing Officer u/s. 197/195(2)/195(3) must be obtained, or a certificate of the Chartered Accountant should be obtained.

-

Sub-rule (2) of the revised Rule 37BB makes the furnishing of Form 15CA to the authorized dealer before the remittance of the payment.

I am planning to buy design software from USA. The software will be downloaded online and the supplier will mail me the activation code. Do I have to inform customs regarding this purchase. My bank asked me to generate 15CA and submit filled A2 form. Request your advise.

i would like to file a 15CA and 15CB forms to get my NRO money repatriated to our US account here. We are US pp holders and have NRE accounts with the same bank . The bank has requested us to submit the the two forms

Read more at: https://taxguru.in/income-tax/efile-form-15ca-15cb.html

Copyright © Taxguru.in

My daughter is NRI for the last 10 years. She had house site in Bengaluru purchased in 2009. Now she wants to sell and repatriate the proceeds to Australia. Please inform the detailed proceedure to be followed by the purchaser and my daughter as well.

Thanks in advance

I have remitted $$$ from SBI New York to my account and some remittence to my brother’s account over time of several years. All remitted destination accounts are domestic(neither NRE or NRO) accounts in India. I got email confirmation of each of these remittance from SBI New York and even I can show that the checks were issued from my Bank account in US(tax paid before, source of funds are my salary) . Is this (email confirmation of remittance) is enough for Form 15CB? or any other proofs are required? Thanks.

I am a senior NRI living in Canada. I submitted Forms 15CB (accountant certificate) and 15CA on 13th April, 2022. The proposed date of remittance was 14th April but due to misunderstand with the bank procedures, all the documentation was finalized only in this month July. Now the bank is saying that both CB15 and CA15 are non valid because it is more than 15 days from the date of filing.

I understand that CB15 is valid for the entire financial year and CA15 is valid for each transaction in that year.

It is very difficult and very costly for me to do from Canada and courier all the documents to the bank all over again.

Appreciate your clarification.

I have wrongly enter wrong firm registration number in form 15CB now what i have to do what are the consequences sir please let me know

I am looking for professional help in preparing 15CA & 15CB to transfer funds from my NRO account at Kotak Mahindra Bank in India to my Bank Account in USA. The amount is appx Rs 12 Lakh. What would such a service cost in Rs.?

We can connect if not done

As per law 15CA is only required if the amount purported to be transferred is not taxable in the hands of the recipient provided the bank agree to it. In your case it is so . For professional help you may contact me.

I WANT TO SEND MONEY OUTSIDE INDIA FOR EDUCATION BUT I AM ASKED TO FILL IFSC CODE AND BSR CODE OF THE DESTINATION BANK IN 15 CA FORM. FOREIGN BANKS DO NOT HAVE THESE, THEY HAVE SWIFT CODES. PLS HELP ME FILL UP THE 15CA FORM

Kindly note that the Part A of Form 15CA to be filled if the aggregate remittances is less than Rs.5 Lakhs but it is stated otherwise.

Sir

As a banker how to verify the authenticity/genuineous of 15 ca and Cb submitted by Customer ??? Now a days all liabilities are fixed banker in this case we need some validation/check point against forge/fake document.?? Kindly clarify please

Good Question.! 15CA is a declaration made by the remitter is in the form of if an affidavit and he sign it saying it as true to the bes of h knowledge. 15CB is issued by a CA certifying that the amount purported to be transferred is taxable/ tax free and applicable tax has been deducted before remittance. The banker is an authorised dealer has to confirm whether the proposed remittance is valid as per FEMA by asking for evidences from customer. If foreign exchange is bought by Authorised Dealer for the proposed remittance not valid under FEMA both customer and bank has to pay penalties which is huge under FEMA.

In what cases is Form 15CA Part D required? I have income in India from Grandfathered LTCG < Do I need to fill Form 15CA Part A or Part D.

You cannot repatriate all the money in your NRO account in whatever manner it is credited. Only money repatriable can be repatriated out of NRO account.Part D is required if the proposed remittance is not chargeable to tax in India. If not chargeable to tax in India, normally no 15CB is required . But banks ask for it to keep them safe.

Dear Shiv Kumawat,

I am looking for professional help in preparing 15CA & 15CB to transfer funds from my NRO account at SBI in India to my SBI branch in Canada. The amount is appx Rs 12 Lakh. What would such a service cost in Rs.?

Are you able to provide thes

Dear Sir, let us know if you have completed this. If not we can connect and help on this

15CA part D is only required in this case if the bank agree as the amount proposed to be remitted is not chargeable to tax in India in the hands of recipient. If you could provide more details, would be of great help to assist you.

I am trying to file Form 15CA Part D to repatriate my Indian PF amount withdrawal over 5 Lakhs into my Canadian account. Can you please suggest the applicable “Purpose code as per RBI”, I am unable to find any option for Provident fund.

Sir,

I would like to transfer some money (< 5 lakh) from my Indian (NRO) account to NRE account. The money is from the fixed deposits that I started while I was working in India (10 years back). Do I need to submit Form 15CA?

Whether the limit of Rs 5 Lacs for filling information in Part A of Form 3CA is remitter wise or remittee wise i.e. a person can remit upto Rs 5 Lacs to various remittees or he can remit upto Rs 5 Lacs to different remittees.

Does bank needs Form 15CA and Form 15CB on sale of equity shares (Either short term or Long Term) by NRI under Portfolio Invesment Scheme

Subject: RBI Circular (RBI/2015-16/390 dated May 5, 2016), Clause 5A (viii) on local income credit to NRE Account of NRIs/PIOs.

Clause 5A (viii) of the Circular unequivocally states that: **QUOTE** Current income like rent, dividend, pension, interest etc. of NRIs and PIOs will be construed as a permissible credit to their NRE Account provided the Authorized Dealer is satisfied that the credit represents current income of the NRI/PIO account holder and income tax thereon has been deducted/paid/provided for, as the case may be. **UNQUOTE**

In our case, we have rented out our Commercial Building to SBI and the mutually executed Lease Agreement at the Registration Dept. clearly indicated that we are NRIs. SBI credits monthly rent to our NRO Account after deducting TDS at 30%, as applicable for NRIs. In addition, we have updated the passport plus Visa details periodically to SBI to prove our NRI Status. Our resident status is “non-resident” in ITR and our IT filing is up-to-date till FY2018-19. Due to the foregoing reasons, being SBI (Lessee, in the capacity of Authorized Dealer) itself is the payer of premises rent to an NRI (Lessor), we indisputably qualify for direct rent credits to our NRE Account. But SBI insisting on submitting Form 15CB for crediting rent to our NRE A/c. Form 15CB is used for fund transfers (repatriation) to another country.

Kindly advise whether Form 15CB is mandatory.

Banks in most cases prefer to go with 15CB to keep them safe. 15CB is required only in those cases where the proposed remittance is taxable in the hands of recipient in India and applicable tax has been deducted before remittance. Once the amount is left out of India there is no guarantee that the recipient will pay tax on such income in India if it were taxable in India. To ensure that applicable tax has been deducted/paid 15CB is issued to bank.

Dear sir

I want to know if a person import a service from outside India and service provide in ordinary resident of India but he wants the payment in Foreign Currency .Do we required to furnish 15CA/CB payment is exceeding 5lakh rs.

me and my wife jointly purchased a property from NRI. he applied for tax exemption on long term capital gain and received a certificate with TDS rate as 3% instead of standard 23%. I made all the TDS payment using my wife’s TAN number for section 195. how to handle TDS liability at my end now? can it be covered by form 15cb.?

Hello Sir,

I have a partnership firm and paying rent to NRI in NRO account in Indian currency. Whether I am require to file 15CA and 15 CB Form.

Hello Sir,

I have a query on transfering money to UK. I have money in my saving accounts and have filed my returns every year. All my savings have been from salary and no other instruments.I would like to transfer about 40 lakhs to buy a property in UK. which forma are required for me to submit

Dear Sir,

I need to know in the case of remittance against import of goods for export directly without touching Indian customs require to furnish CB15 form while making payment to the supplier?

I am NRI..I Sold immovable property in FY 2019..20 for Rs.60 lacs…i have been filing my return of indian income regularly..

I want to transfer. Rs.60 lacs to US and buy a property there..As it is self transfer do i need to file 15 CA and obtain 15CB..even though transferor and transferee is same..it is me and it is not mentioned in 28 exemptions i believe.please guide me..

Sir, I want to ask you some question, in which transaction Form 15 CA & 15 CB are require?

Hello. I am an NRI. I have an Indian PAN Card and file my ITR regularly. I have rental income in India. I want to transfer this to my UK account. Is form 15CA 15CB compulsory for this remittance. Please advise

My question is in form 15 CA field ” in case remittance ia net of taxes amount should be grossed up ” yes or no.

If net of taxes and selected as yes and net off payment being done, is right or wrong

If doing gross up and selected no right or wrong

My query related to 15ca part a. limit of Rs 5 lacs is applicable on remitter or particular foreign beneficiary in FY

Sir, I have a query regarding

1.Party(NRI) sold the property in 2016-17 and paid tax on the capital gains .Now the party wants to transfer the amount in the current year 2019.

Amount to be transferred is Rs.80L

2.Which part of form 15CA is to be issued , Part C or Part D ?

Hi

Can you please let me know the average cost a CA will charge to fill up form 15 CA?

Hello sir..

i want to transfer my gratuity amount (transfer fund) 2 lac from nro to nre so want to ask whether form 15 ca only to fill and whether Part D only to fill of the income not chargeable to tax?? and what source code to select??

whether 15 cb is also required as amount is less than 5 lac

I am NRI and having NRO and NRE Saving bank accounts and FDS in India. I want to transfer net interest income from NRO FDS after TDS to my NRE Saving Bank account in the same branch of the bank .

I am a regular income taxpayer and file a regular tax return in India. All funds available in my saving bank and bank FDs are tax paid and or provided for.

I would like to have clarity particularly on the following points:-

1. Can I transfer my net current interest income from NRO Bank FDS after TDS to my NRE account with the same Bank?

2. What procedure I should follow for this. In such cases are the certificates 15CA and/or 15CB required.?

If remittance is made to a foreign country without deducting Tax, wherein Tax is to be deducted for a particular remittance, how to rectify the same? Nowadays we read in Newspapers RBI is levying Rs. 1 Crore penalty for each default. If so whether for such lapses will penalty be levied?