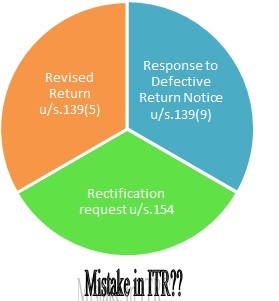

Filing of Rectification request under section 154 of Income Tax Act

Income Tax Return filed by the taxpayer is processed by Centralised Processing Centre (CPC) and intimation under section 143(1) is sent to the assessee based on the details disclosed by the taxpayer in his/her ITR and system based rules for processing of ITR deployed at the CPC of Income Tax Department. In case, if the taxpayer wants to seek rectification of a mistake in an order or intimation, which is apparent from the record, then the taxpayer can seek ‘Rectification under Section 154’. With the use of technology, filing of rectification request is now online, paperless and faceless. There are multiple reasons for filing rectification request (sometimes called as Rectified ITR). In this article, we will be discussing about Section 154, how to file rectification request, reasons & types of rectification, Revised Return, Defective Return, various timelines and other aspects relating to rectification.

1. Options available to rectify mistakes in Income Tax Return filing /Order/Intimation

First of all, let’s see the multiple options to rectify the mistake/correction in ITR already filed. But each option is independent & has its own timeline, applicability norms & limitation. Let’s discuss as follow-

First of all, let’s see the multiple options to rectify the mistake/correction in ITR already filed. But each option is independent & has its own timeline, applicability norms & limitation. Let’s discuss as follow-

1.1 Revised Return u/s.139 (5)

If any person, having furnished a return under sub-section (1) or sub-section (4), discovers any omission or any wrong statement therein, he may furnish a revised return at any time before the end of the relevant assessment year or before the completion of the assessment, whichever is earlier.

1.2 Response to Defective Return Notice u/s. 139(9)

Where the Assessing Officer considers that the return of income furnished by the assessee is defective, he may intimate the defect to the assessee and give him an opportunity to rectify the defect within a period of fifteen days from the date of such intimation or within such further period which, on an  application made in this behalf, the Assessing Officer may, in his discretion, allow; and if the defect is not rectified within the said period of fifteen days or, as the case may be, the further period so allowed, then, notwithstanding anything contained in any other provision of this Act, the return shall be treated as an invalid return and the provisions of this Act shall apply as if the assessee had failed to furnish the return.

application made in this behalf, the Assessing Officer may, in his discretion, allow; and if the defect is not rectified within the said period of fifteen days or, as the case may be, the further period so allowed, then, notwithstanding anything contained in any other provision of this Act, the return shall be treated as an invalid return and the provisions of this Act shall apply as if the assessee had failed to furnish the return.

Provided that where the assessee rectifies the defect after the expiry of the said period of fifteen days or the further period allowed, but before the assessment is made, the Assessing Officer may condone the delay and treat the return as a valid return.

Hence any defect in ITR filing, as communicated by CPC, can be rectified by filing ITR under this section.

1.3 Rectification Request u/s. 154(1)

As per provisions of section 154, With a view to rectifying any “mistake apparent from the record” an income- tax authority referred to in section 116 may,—

(a) amend any order passed by it under the provisions of this Act ;

(b) amend any intimation or deemed intimation under sub-section (1) of section 143;

(c) amend any intimation under sub-section (1) of section 200A;

(d) amend any intimation under sub-section (1) of section 206CB.

Important Point to Note:-

- There are two limbs which is required to be fulfilled to make an order rectifiable. These are cumulative satisfaction of conditions and absence of one satisfaction is sufficient for disqualification of order.

- Mistake

- Apparent from records

- An illustrative list of mistakes which can be rectified are as under:

- Any Arithmetical, Clerical error

- Misreading of any provision of law

- Application of wrong provision of law

- Non-allowance of tax credit on the ground that same is not reflecting in 26AS whereas section 205 clearly enforce bar against direct demand on assessee.

- Non-following of jurisdictional high court judgment.

- Rectification request should not be filed for change in Gross Total Income & Chapter VIA deductions

- There should NOT be any revision in Income or new claims of deduction/ exemption made in the Rectification request, as this would lead to rejection or delay in processing by CPC.

- This facility is only provided by Income Tax Department for correcting mistakes. In case you wish to make changes in Income or make new claims, a Revised Income Tax Return should be filed as per the Income Tax Act, 1961.

2. Sue-Moto Rectification V/s. Rectification Request

As per provisions of section 154, Income Tax authority concerned—

(a) may make an amendment under sub-section (1) of its own motion, (Sue-Moto Rectification by AO)

(b) shall make such amendment for rectifying any such mistake which has been brought to its notice by the assessee or by the deductor or by the collector, and where the authority concerned is the Commissioner (Appeals), by the Assessing Officer also (Rectification Request by Assessee/Deductor).

3. Timelines for Rectification Request

Amendment under section 154 can’t be made after the expiry of four years from the end of the financial year in which the order sought to be amended was passed.

4. Timelines for Processing of Rectification Request

When an application for amendment under section 154 is made by the assessee or by the deductor or by the collector, the authority shall pass an order, within a period of six months from the end of the month in which the application is received by it,—

(a) making the amendment; or

(b) refusing to allow the claim.

5. Important aspects relating to rectification request

- Rectification request can be filed only if, Income Tax Return for the Assessment Year have already been processed u/s.143(1) by CPC

- Only one rectification Per CPC Order for an Assessment Year can be filed, unless and until the Rectification Return Request is withdrawn / processed.

- In case of person was audited u/s.44AB in the year under consideration, it is mandatory to digitally sign the rectified ITR as well.

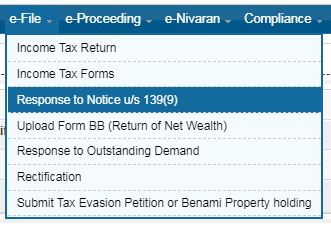

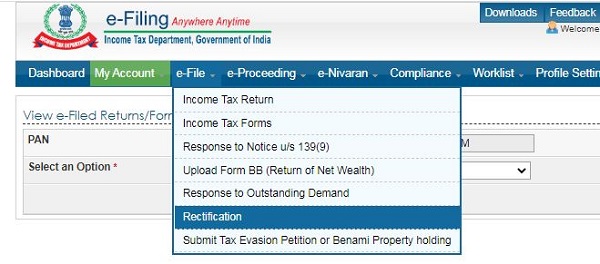

6. Steps for online filing of request for rectification u/s.154

Following steps need to be followed for e-filing of Rectification Request u/s.154

1. Logon to ‘e-Filing’ Portal www.incometaxindiaefiling.gov.in

2. Go to the ‘e-File’ menu located at upper-left side of the page > Click ‘Rectification’

3. Choose the options of ‘Order/Intimation to be rectified’ and ‘Assessment Year’ from the drop down list > Click ‘Continue’

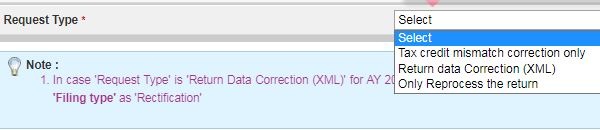

4. Select any one of the following options of ‘Request Type’ from drop down list.

Detailed discussion on rectification request types is given in point no.7 of the article.

5. Click Submit to complete the rectification request. A Success message will be displayed and a mail confirming the submission of rectification request will be sent to the user’s registered mail id.

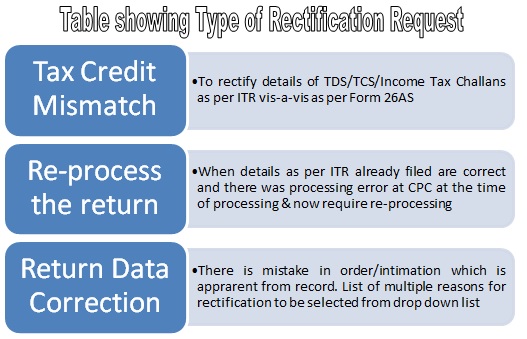

7. Types of Rectification Requests

In the Income Tax E-filing Portal, rectification request is categorized into 3 types as follows-

7.1 Tax Credit Mismatch

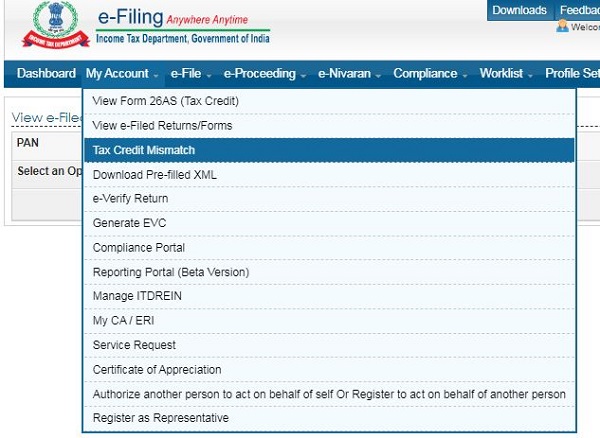

Taxpayer can view Tax Credit Mismatch by following steps:-

- Logon to ‘e-Filing’ Portal incometaxindiaefiling.gov.in

- Go to the ‘My Account’ menu located at upper-left side of the page

- Click ‘Tax Credit Mismatch’

- Select ‘Assessment Year’

Above highlighted Item is Menu used for checking Tax Credit Mismatch

- Taxpayer can view both Form 26AS and Tax Credit Mismatch under ‘My Account’ on e-filing portal.

- Kindly reconcile ITR with Form 26AS before submitting rectification request.

|

After reconciling mismatch in Tax Credit, Kindly file rectification request as given in Point No.6 above. After selecting rectification request type as ‘Tax credit mismatch correction only’ – following check boxes will be displayed.

-

- TDS on Salary Details

- TDS on Other than Salary Details

- TDS on transfer of Immovable property/Rent

- TCS Details

- IT Details

- You may select the check box for which data needs to be corrected.

- You can add a maximum of 10 entries for each of the selections.

- No upload of an Income Tax Return XML file is required.

- However, In case of large number of entries of Tax Credit, ‘Return Data Correction/Upload XML’ option is to be opted instead of this option.

7.2 Reprocess the return

- On selecting this option, user needs to just submit the rectification request, without any modification in ITR Form.

![]()

- This option is generally considered if there was no mismatch/mistake in ITR Form, and there was processing error at CPC (or) details of TDS/TCS/IT as per Original ITR filed were already correct, however at the time of processing of ITR, tax credit was not available in Form 26AS due to non filing/incorrect filing of TDS Return by deductor, however the same have been rectified now and Tax Credit duly shown in Form 26AS as per ITR Filed.

- User can check & verify the Form 26AS details under My Account

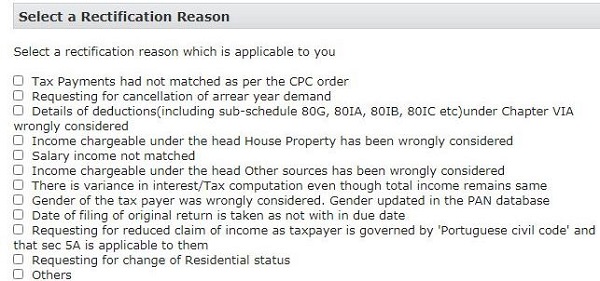

7.3 Return Data Correction / Upload XML Option

Taxpayer need to select one of reasons for Return Data Correction option of rectification u/s.154.

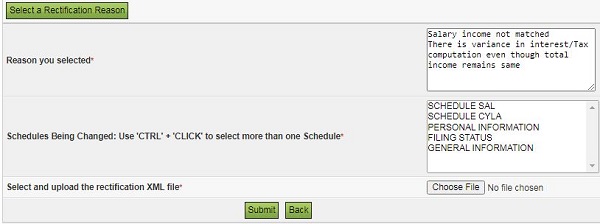

The complete Income Tax Return should be e-Filed and NOT just the schedules/ fields that need change/correction. Taxpayer need to prepare XML File of Rectified ITR and upload in this menu for rectification, after selecting the appropriate ‘Rectification Reason’ as above-

Select ‘Schedules being changed’ by using ‘Control + Click’ to select the multiple schedules & Click on Submit.

8. Update regarding online enabling of Rectification request for A.Y.2020-2021

- The facility to file rectification for Asst Year 2020-21 on the 143(1) intimations issued by CPC Bengaluru, is now enabled for “Return data correction” & “Only Reprocess the return”. The rectification facility for “Tax credit mismatch correction” will be enabled soon. (Update dated 11/01/2021)

- As per Remarks given on e-filing Portal of Income Tax (screenshot taken on 31/01/2021), till the time facility to rectify Tax Credit Mismatch is enabled, the same can be rectified through ‘TDS/TCS/IT Schedules’ through ‘Return Data Correction/XML Upload’ option.

9. Probable Reasons of Mistakes in ITR & there resolution

Before filing rectification request, kindly carefully review the Common Error Guide and the typical causes of error to prepare an accurate rectification request and thereby ensure that you get a proper resolution from CPC in the form of rectification order. For every variation between what you have computed as your tax liability and your refund and what was finally the outcome of processing at CPC there is a logical explanation and therefore, a possible resolution. Refer article published by Taxguru Team as per following link-

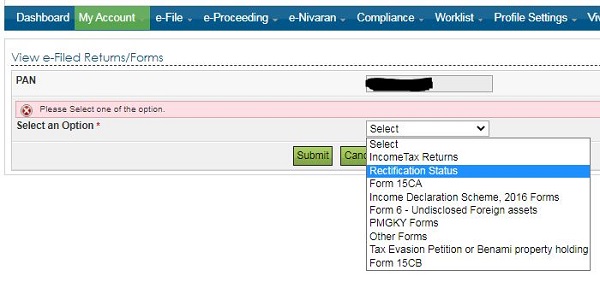

10. View Status of Rectification Request

To View the submitted Rectification Request:

- Logon to ‘e-Filing’ Portal incometaxindiaefiling.gov.in

- Go to the ‘My Account’ menu located at upper-left side of the page

- Click ‘View e-Filed Returns/Forms’

- Click ‘Submit’

- Select ‘Rectification Status’ from drop down list

11. Withdrawal of Rectification Request

You can withdraw a rectification request within same day of filing, by following steps:-

- Go to My Account

- View e-filed Returns/Forms

- Rectification Status > To Withdraw

********

Article Contributed by: CA. Sagar Gambhir | FCA, DISA (ICAI), DIRM (ICAI) | casagargambhir@gmail.com

Author can be reached at casagargambhir@gmail.com for any queries, issues & recommendations relating to article.

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author Bio

Fantastic article Sir… I get the following error when I upload xml file in Return Data Correction menu, since I got notice u/s 154 for my ITR for AY20-21

Error: Failed to fetch Data.

How to resolve Sir.

Regards, Rajendra Prasad 9841087606

In my salary schedule, I put all the salary under one box instead of breking it up in basic, hra and so on. As a result I received demand notice u/s 143(1). Do I have to file revised return or rectification will work? Also, do I have to pay the tax even if I apply for rectification?

Sir,

How does one file a rectification application to correct a mistake in the order u/s 143(3) passed by the NEAC.

My understanding is that once the final faceless order is passed, all electronic records are passed on to the jurisdictional AO.

In which case logically the rectification application ought to be physically/e-mail filed with the AO. Am I correct? Thanks.

Yes. Reference in this regard is invited to paragraph 5(xx)(c) of the E-Assessment Scheme, 2019 notified by the Central Government, which stipulates that the NEAC, after completion of assessment, is required to transfer all the electronic records of the case to the Assessing Officer having jurisdiction over such case for, inter-alia, rectification of mistake under Sec.154.

Corrigendum. Paragraph 5(xxvi) of the Faceless Assessment Scheme, 2019 stipulates that the National e-assessment Centre shall, after completion of assessment, transfer all the electronic records of the case to the Assessing Officer having jurisdiction over the said case for such action as may be required under the Act.

Does this mean that after an order is passed by NEAC, rectification application should be filed before concerned assessing officer having jurisdiction over the assessee?

This is very well written article. Thanks.

I AM ” C.A. PROFESSIONAL” IN PRACTICE IN MUMBAI .

THE AUTHOR , CA SAGAR GAMBHIR HAS WRIITEN A GOOD ARTICLE EXPLAINING THE DETAILS OF MISTAKES / RECTIFICATION PROCEDURE IN MINITE DETAILS.

A VERY USEFUL ARTICLE.

CONGRATS SAGAR , AND BEST LUCK .

Write up of Mr CA Sagar Gambhir on section 154 of IT Act 1961 is commendable ( by a very young person), my all good wishes and congratulations to him.