Case Law Details

DCIT Vs Vinod Gupta (ITAT Delhi)

Delhi ITAT Applies Ojjus Medicare: Section 153C Assessment Beyond Six Years Quashed

The Delhi ITAT dismissed the Revenue’s appeal and upheld the CIT(A)’s order annulling the assessment made under section 153C against Vinod Gupta for AY 2014-15, holding that the assessment was barred by limitation and fell outside the permissible six-year period prescribed under the law.

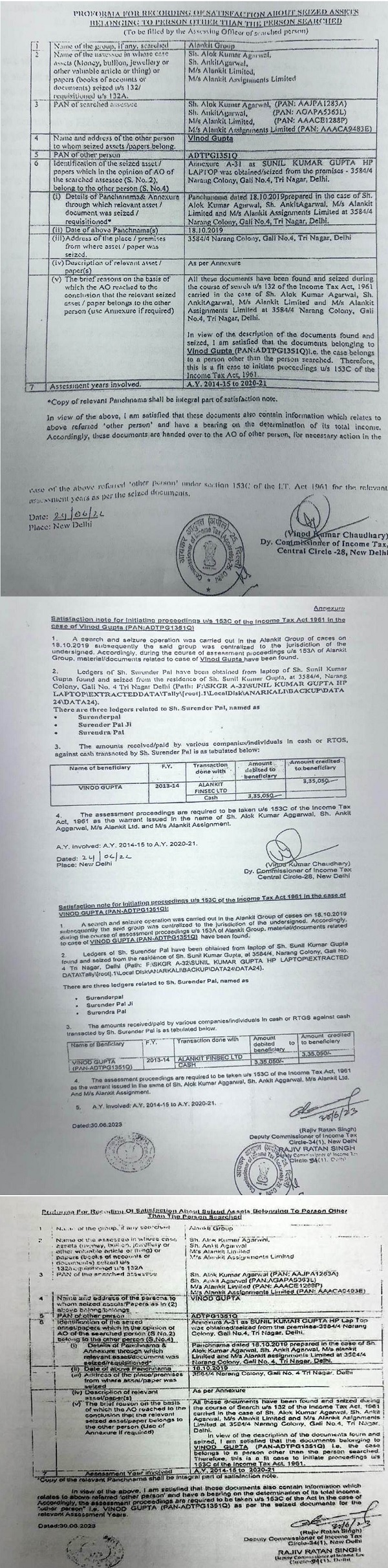

The case arose from a search conducted on the Alankit Group. Certain documents allegedly belonging to the assessee were found during the search, and a satisfaction note under section 153C was recorded on 24.06.2022. Based on these documents, proceedings were initiated against the assessee for AY 2014-15.

The CIT(A), relying on the Delhi High Court decision in PCIT v. Ojjus Medicare Pvt. Ltd., examined the date on which the seized material was handed over and the satisfaction note was recorded. Since these events occurred during FY 2022-23 (relevant to AY 2023-24), the six assessment years that could validly be covered under section 153C were only AYs 2017-18 to 2022-23. AY 2014-15 fell outside this six-year block.

The appellate authority further noted that the satisfaction note itself reflected alleged transactions aggregating only about ₹3.35 lakh, far below the statutory threshold of ₹50 lakh required for invoking the extended period beyond six years. Therefore, the conditions necessary for reopening older years were not satisfied.

The Tribunal found that the Revenue was unable to point out any factual or legal error in the CIT(A)’s reasoning. Following the ratio laid down in Ojjus Medicare, it held that AY 2014-15 could not be brought within the ambit of section 153C proceedings and that the assessment order passed under section 153C had no legal foundation.

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal is preferred by the revenue against the order dated 19.08.2025 of Ld. Commissioner of Income Tax (A)-25, Delhi (hereinafter referred to as the First Appellate Authority or ‘the ld. FAA’ for short) in DIN No : ITBA/APL/M/250/2025-26/1079726362(1) arising out of the assessment order dated 28.03.2024 u/s 153C of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) passed by DCIT, CC-28, Delhi for AY: 2014 -15.

2. On hearing ld. DR has basically relied the ground by which department has challenged the impugned order of ld. CIT(A) wherein after taking into consideration the decision of Delhi High Court in the case of PCIT v. Ojjus Medicare Pvt. Ltd. (2024)465 ITR 101, the ld. CIT(A) has quashed the assessment order. On going through relevant part of the impugned order and para 15 to 19 we observe that following factual and legal aspects have been considered:

“15. The period of six assessment years as per the aforesaid decisions of the Hon’ble jurisdictional High Court of Delhi thus means six years prior to the assessment year in which the seized material was handed over to the AO of the ’other’ (non-searched) person/satisfaction note u/s 153C was recorded by the concerned AO. As per record, the Satisfaction note was recorded by the AO on 24.06.2022, on which date the seized documents were also handed over to the AO of the other person (appellant) by the AO of the searched person/s. This date falls in the F.Y. 2022-23 relevant to AY 2023-24. Therefore, by this yardstick, six years period as referred to in section 153C(1) of the Act would be from AY 2017-18 to 2022-23.

16. To ascertain whether the income escaping assessment in the relevant assessment year or the aggregate of the assessment years amounted to or was likely to amount to Rs. S0 Lakhs or more, the copy of the satisfaction note drawn as seen from record was perused, as reproduced below:

17. From the above, it is seen that the aggregate of the income having escaped assessment for the relevant assessment years’, ie. AY 2016-17 (FY 2015-16), AY 2015-16 (FY 2014-15) and (impugned) AY 2014-15 (FY 2013-14) as per the satisfaction note recorded falls short of Rs. 50 lakhs.

17.1 Following the ratio of decision as per the Hon’ble jurisdictional High Court in the case of Ojjus Medicare (supra), there is nothing in the satisfaction note to show that the income, represented in the form of asset which has escaped assessment, amounted to or was likely to amount to Rs. 50 Lakhs or more in the relevant assessment year” or in aggregate in the ‘relevant assessment years” in the case of the appellant under consideration.

18. Thus, the condition spelt out in the statute and as interpreted by the Hon’ble Courts for permitting reopening beyond six years was not fulfilled in the instant case. The case of the impugned A.Y. 2014-15 falls beyond the period of six years preceding the assessment year relevant to the previous year in which the satisfaction note was drawn / seized documents were handed over to the appellant’s AO. The period of six years that could be reopened by the AO thus terminates with the AY 2017-18. The contention of the appellant therefore bears merit.

19. Relying on the above-mentioned case laws and respectfully following the judgment of the Hon’ble jurisdictional High Court in the case of Ojjus Medicare (P.) Ltd (supra), it is seen that A.Y. 2014-15 is not covered within six AYs as per section 153C of the Act and the condition/s for assessing it as part of the relevant assessment years was not existent. The notice issued for the instant assessment year, AY 2014-15 would thus fall beyond the ambit of six AYs’ as provided under section 153C read with section 153A, and hence the impugned assessment order dated 28.03.2024 passed u/s 153C of the Act for the instant AY 2014-15 in pursuance of such notice would not survive, having no legs to stand, and is thus annulled.”

3. In the light of aforesaid circumstances as the ld. DR was unable to cite any proposition of law or fact to counter the conclusions settled by ld. CIT(A), we find no substance in the appeal of department the appeal is dismissed.

Order pronounced in the open court on 03.06.2026

Author Bio