Case Law Details

Amit Dokwal Vs ITO (ITAT Hyderabad)

SEO Title : Addition Deleted on Cash Deposits Already Offered as Section 44AD Turnover: ITAT Hyderabad

Material Facts

The assessee, an individual engaged in the business of trading in agricultural produce, challenged the order of the Commissioner of Income Tax (Appeals), NFAC, dated 08.12.2025 for Assessment Year 2013-14. The Assessing Officer initiated reassessment proceedings under Sections 147 and 148 after receiving information regarding cash deposits in the assessee’s bank account. During reassessment, the Assessing Officer treated cash deposits of ₹42,40,000 as unexplained money under Section 69A and completed the assessment under Sections 147 read with 144B, determining the total income at ₹54,78,270. The CIT(A) confirmed the addition.

Procedural History

The assessee appealed against the assessment order before the CIT(A), who upheld the addition of ₹42,40,000 under Section 69A. Aggrieved by that decision, the assessee filed an appeal before the ITAT Hyderabad.

Legal Issues

- Whether the addition of ₹42,40,000 under Section 69A was sustainable when the same amount had already been disclosed as business turnover and offered to tax under Section 44AD.

- Whether the cash deposits could be separately taxed as unexplained money after acceptance of the returned business turnover.

Relevant Statutory Provisions

- Section 44AD

- Section 69A

- Sections 147, 148 and 144B

- Section 115BBE

- Sections 234A, 234B and 234C

- Sections 271(1)(c) and 271F

Assessee’s Submissions

The assessee submitted that he was engaged in trading agricultural produce and produced a Gram Panchayat licence in support of the business activity. It was contended that the cash deposits of ₹42,40,000 represented business sale proceeds and had already been disclosed as business turnover in the return of income. Income of ₹3,39,300 was offered on such turnover under Section 44AD.

The assessee argued that by treating the same amount as unexplained money under Section 69A, the Assessing Officer subjected the same receipt to double taxation. It was further submitted that an assessee opting for presumptive taxation under Section 44AD was not required to maintain books of account or produce purchase and sale bills. Reliance was placed on the decision in CIT Vs. Surinder Pal Anand (192 Taxman 264).

Revenue’s Submissions

The Revenue contended that the assessee failed to substantiate the actual purchase and sale transactions or establish the nexus between the cash deposits and the alleged business activity. It argued that merely offering income under Section 44AD did not automatically establish that all cash deposits represented business receipts and, therefore, the addition under Section 69A was justified.

Tribunal’s Observations and Findings

The Tribunal observed that merely declaring income under Section 44AD does not relieve an assessee from establishing that receipts deposited in the bank account relate to business activities. It held that the decision in CIT Vs. Surinder Pal Anand did not dispense with the requirement of establishing the source of gross business receipts. According to the Tribunal, the judgment only provides that individual cash deposits need not be separately explained once they are found to have nexus with accepted business receipts.

The Tribunal noted that the Gram Panchayat licence supported the assessee’s claim of carrying on agricultural produce business, although it did not by itself establish the volume of transactions. It also examined the assessment order and found that the Assessing Officer had accepted the return of income in which the amount of ₹42,40,000 had already been disclosed as business turnover under Section 44AD and the returned income had not been disturbed.

The Tribunal held that once the Assessing Officer had accepted the turnover disclosed under Section 44AD, the very same amount could not again be assessed as unexplained money under Section 69A. It observed that such treatment resulted in taxing the same receipt twice. The Tribunal further recorded that the Revenue had not produced any material to show that the impugned cash deposits were over and above the turnover already disclosed in the return of income.

Final Ruling

The ITAT Hyderabad directed the Assessing Officer to delete the addition of ₹42,40,000 made under Section 69A, holding that the cash deposits had already been accepted as part of the business turnover disclosed under Section 44AD. The appeal of the assessee was allowed.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal is filed by Shri Amit Dokwal (“the assessee), feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi (“Ld. CIT(A)”) dated 08.12.2025 for the A.Y.2013-14.

2. The assessee has raised the following grounds of appeal:

1. The Ld. CIT(A) has erred CIT(A),NFAC erred on fats and in law while dismissing the appeal.

2. The Ld.CIT(A) ought to have observe the fact that the issuance of notice u/s.148 is bad in law.

3. The Ld. CIT(A) ought to have observed that the Ld. AO has failed in the reasons recorded in respect of escapement of income do not establish any tangible material between the material relied upon and the alleged escapement of income. Hence, the assumption of AO under section 147 and the reassessment proceedings are bad in law and liable to be quashed.

4. The Ld. CIT(A) grossly erred in appreciating the facts of the case of the appellant.

5. The Ld. CIT(A) NFAC erred in upholding the additions Rs.42,40,000/- u/s. 69A of the act.

6.

a. The Ld. CIT(A) ought to have appreciated the assessment order under section 147 r.w.s 1448 of the act dated 17.03.2022 is invalid.

b. The Ld, CIT(A) ought to have appreciated that the addition of Rs.42,40,000/- cannot be made in respect of which the proceeding under section 147 of the act were not initiated, since no addition has been made in respect of cash deposits of Rs.1,80,60,000 on which the proceedings were initiated.

c. The Ld. CIT(A) ought to have appreciated that the addition of Rs.42,40,000/• which was not part of the reasons to believe, cannot be made since the reasons recorded by the AO to reopen the assessment were not found valid.

d. The Ld. CIT(A) ought to have appreciated income inrespect of cash deposits Rs.1 ,80,60,000/. which was the basis of the formation of the “reasons to believe” is not assessed to reassessed, it would not be open to the AO to independently Assess only the income of Rs.42,40,000/-which has come to the notice subsequently in the course of the proceedings u/s.147 of the Act.

e. The Ld. CIT(A) ought to have appreciated that the AO in clear terms has express his satisfaction with regard to the cash deposit of Rs.1,80,60,000/• at para no.6 of the assessment order, the amount being the basis of the reassessment proceedings u/s.147 of the Act.

7. Without prejudice to other grounds, the Ld.CIT(A) ought to have appreciated that the amount of Rs.1,80,60,000/- mentioned in the reasons for reopening of assessment is not correct since multiple amounts are wrongly repeated in arriving at it.

8. The Ld. CIT(A) ought to have observed that once the return of income is accepted, only presumptive income can be taxed but not all the gross receipts, which results in double taxation.

9. The 14, CIT(A) ought to have observed that the receipts earned were out of cash sales at local markets where no formal bills or invoices are ordinarily issued, and such receipts have been already been considered in the return of income u/s.44AD and the same has been accepted earlier, now the same cannot be treated as unexplained.

10. The Appellant craves to add/leave/alter/modify any other ground of appeal at the time of hearing.

3. The brief facts of the case are that the assessee is an individual who had not filed any return of income for Assessment Year 2013-14. On the basis of information available with the Department, the Learned Assessing Officer (“Ld. AO”) found that the assessee had deposited cash in his bank account during the year under consideration. Accordingly, reassessment proceedings were initiated in the case of the assessee under section 147 of the Income-tax Act, 1961 (“the Act”) and notice under section 148 dated 30.03.2021 was issued by the Ld. AO to the assessee. During the reassessment proceedings, the Ld. AO observed that the assessee had deposited cash aggregating to ₹42,40,000/- in his bank account during the year under consideration. Being not satisfied with the explanation furnished by the assessee regarding the source of such deposits, the Ld. AO treated the cash deposits of ₹42,40,000/- as unexplained money under section 69A of the Act and added the same to the income of the assessee. Accordingly, the assessment was completed by the Ld. AO under section 147 read with section 144B of the Act vide order dated 17.03.2022 by making an addition of ₹42,40,000/- under section 69A of the Act and assessing the total income of the assessee at ₹54,78,270/-.

4. Aggrieved by the assessment order, the assessee preferred an appeal before the Ld. CIT(A). The Ld. CIT(A), however, confirmed the addition made by the Ld. AO and dismissed the appeal of the assessee.

5. Aggrieved by the order of the Ld. CIT (A), the assessee is in appeal before the Tribunal. The Learned Authorized Representative (“Ld. AR”) submitted that the assessee is engaged in the business of trading in agricultural produce. In support of the said contention, he invited our attention to the license issued by the Gram Panchayat in the name of the assessee placed at page nos. 53 to 55 of the paper book. The Ld. AR submitted that during the year under consideration the assessee had undertaken purchase and sale of agricultural produce and the cash deposits aggregating to ₹42,40,000/- represented sale proceeds received in cash from such business activities. Inviting our attention to the computation of income placed at page no. 40 of the paper book, the Ld. AR submitted that the assessee had disclosed the cash deposits of ₹42,40,000/- as business turnover and offered income of ₹3,39,300/- thereon under section 44AD of the Act. The Ld. AR submitted that despite the assessee having already disclosed the said amount as business turnover and offered income thereon, the Ld. AO again treated the same amount as unexplained money under section 69A of the Act, resulting in double taxation of the same receipt. The Ld. AR further submitted that since the assessee had opted for presumptive taxation under section 44AD of the Act, he was not required to maintain books of account or produce purchase and sale bills. In support of this contention, reliance was placed on the decision of the Hon’ble Punjab & Haryana High Court in the case of CIT Vs. Surinder Pal Anand (192 Taxman 264). It was submitted that under similar circumstances the Hon’ble High Court held that an assessee declaring income under section 44AD of the Act is not obliged to explain each and every cash deposit appearing in the bank account. Accordingly, the Ld. AR prayed that the addition made under section 69A of the Act be deleted.

6. Per contra, the Learned Departmental Representative (“Ld. DR”) relied upon the orders of the lower authorities. He submitted that the assessee merely claimed to be engaged in the business of trading in agricultural produce but failed to substantiate the same by producing any evidence regarding actual purchase and sale transactions. It was contended that the assessee had failed to establish the nexus between the cash deposits and the alleged business activity. The Ld. DR submitted that merely offering income under section 44AD of the Act does not automatically establish that all cash deposits in the bank account represent business receipts. Therefore, according to the Ld. DR, the lower authorities were justified in treating the impugned deposits as unexplained money under section 69A of the Act.

7. We have heard the rival submissions and perused the material available on record including the case law relied upon. The solitary issue involved in the present appeal relates to the addition of ₹42,40,000/- made under section 69A of the Act on account of cash deposits in the bank account of the assessee. We find merit in the contention of the Ld. DR that merely because the assessee has declared income under section 44AD of the Act, he is not absolved from establishing that the receipts deposited in the bank account are relatable to his business activities. Therefore, the contention of the assessee that filing a return under section 44AD of the Act by itself dispenses with the requirement of substantiating the nature of receipts cannot be accepted. We have carefully gone through para no. 8 of the decision of the Hon’ble Punjab & Haryana High Court in the case of CIT Vs. Surinder Pal Anand (Supra) relied upon by the assessee, which is to the following effect:

“8. Once under the special provision, exemption from maintaining of books of account has been provided and presumptive tax at the rate of 8 per cent of the gross receipt itself is the basis for determining the taxable income, the assessee was not under obligation to explain individual entry of cash deposit in the bank unless such entry had no nexus with the gross receipts. The stand of the assessee before the Commissioner of Income-tax (Appeals) and the ITAT that the said amount of Rs. 14,95,300 was on account of business receipts had been accepted. Learned counsel for the appellant with reference to any material on record, could not show that the cash deposits amounting to Rs. 14,95,300 were unexplained or undisclosed income of the assessee.”

8. On perusal of the above, we find that the Hon’ble High Court held that where income is declared under section 44AD of the Act, the assessee is not required to explain each individual entry of cash deposit in the bank account, provided such deposits have nexus with the gross receipts of the business. The Hon’ble High Court observed that once the receipts are accepted as business receipts, each individual deposit need not be separately explained. However, in our considered opinion, the aforesaid judgment does not lay down a proposition that an assessee declaring income under section 44AD of the Act is completely relieved from establishing the source of the gross receipts themselves. The Hon’ble High Court has never held that the assessee is not required to justify the business receipts or establish the business activity by producing supporting evidence wherever required. The ratio of the said decision is confined to the proposition that individual cash deposits need not be separately explained once they are found to have nexus with the business receipts.

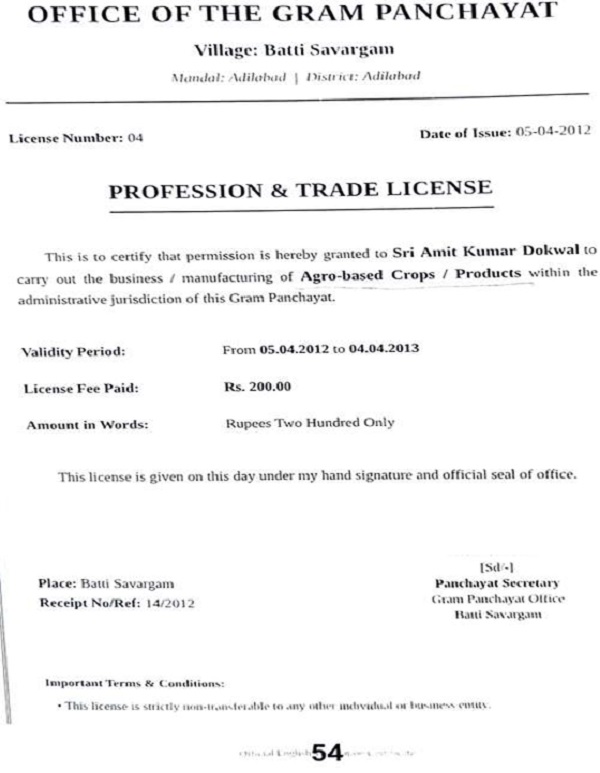

9. In the present case, the assessee has placed on record a license issued by the Gram Panchayat authorizing him to engage in ago-based crop products business, placed at page nos. 53 to 55 of the paper book. The English translation of the copy of the license place at page no. 54 of the paper book is reproduced as under:

10. On perusal of the above, we find that the claim of the assessee regarding engagement in agricultural produce business cannot be out rightly rejected. At the same time, we agree that the license by itself may not conclusively establish the volume of business transactions undertaken during the relevant year. Be that as it may, we have also gone through para no. 7 of the order of the Ld. AO, which is to the following effect:

7. In view of the above it is cleared that the assessee not submitted desired documents/papers/evidences in support of cash deposits and justification/clarification as desired time to time. Therefore, considering the facts and circumstances the case unexplained cash deposits amount of Rs. 42,40,000/- is hereby added back u/s 69A of the I.T. Act read with section 115BBE. The total income of the assessee re-compute as under:

1. Income Shown in original return filed on 30/04/2021 : 12,38,270/-

2. Add:- As discussed in Para 7 : 42,40,000/-

3. Total Income : 54,78,270/-

R/o : 54,78,270/-

Assessed as above. Give credit for prepaid taxes after due verification. Issue necessary forms, give credit of prepaid taxes and charge interest u/s 234A, 234B, and 234C as per the provision of the Income Tax Act, 1961. Assessment order is being passed u/s 147 r.w.s. 144 read with section 144B of the Income-tax Act. Penalty proceeding u/s 271(1)(c) as the assessee failed to explain cash deposit, hence concealed the particulars of income and 271F also initiated separately.

11. On perusal of the above, we find that the Ld. AO has accepted the return of income filed by the assessee wherein the amount of ₹42,40,000/- was disclosed as business turnover and income therefrom was offered by the assessee under section 44AD of the Act. The returned income has not been disturbed by the Ld. AO. Once the Ld. AO has accepted the turnover disclosed by the assessee under section 44AD of the Act, the very same amount could not again be treated as unexplained money under section 69A of the Act. Such an action results in taxing the same receipt twice, firstly as business turnover forming part of the returned income and secondly as unexplained money under section 69A of the Act. It is a settled principle that the same receipt cannot be subjected to tax twice under different provisions of the Act. In the present case, no material has been brought on record by the Revenue to demonstrate that the impugned cash deposits are over and above the turnover already disclosed by the assessee in the return of income. Therefore, after considering the entirety of facts and circumstances of the case, we are of the considered opinion that once the cash deposits of ₹42,40,000/- have been accepted as forming part of the business turnover disclosed by the assessee under section 44AD of the Act, no separate addition under section 69A of the Act can survive in respect of the very same amount. Accordingly, we direct the Ld. AO to delete the addition of ₹42,40,000/- made under section 69A of the Act.

12. In the result, the appeal of the assessee is allowed.

Order pronounced in the Open Court on 3 rd July, 2026.

Author Bio