The Finance Minister while presenting the Finance Bill, 2019, stated that existing system of scrutiny assessments in the income tax department involves a high level of personal interaction between the taxpayer and the tax department, which leads to certain undesirable practices on the part of tax officials. To eliminate such instances and bring more transparency in the assessment system, a scheme of faceless assessment is launched in phased manner. This new scheme of assessment is a significant game-changing moment in direct taxation assessment and litigation.

Finance Act, 2018 has brought new enabling Section 143(3A) to effect a PAN India E-Assessment. Thereafter, CBDT releases E-assessment Scheme, 2019 vide N/N 61/ 2019 dated 12-Sep-19 providing for its scope, procedure, powers etc. Also, 58,322 cases has been selected after launch of scheme for scrutiny assessment for AY 2018-19.

- 1. What is E-Assessment Scheme, 2019?

- 2. Whether the Scheme is applicable for all type of assessments under Income Tax Act, 1961?

- 3. E-assessment Scheme prevail over contradicting provisions of Income Tax Act, 1961

- 4. E-assessment Centres

- 5. Communication

- 6. Procedure for E-assessment

- 7. Role of Jurisdictional Assessing Officer

- 8. Appeal against assessment order

- 9. Delivery and Service of Electronic Record

- 10. Personal Appearance by the assessee

- 11. Comment on Validity of Jurisdiction and Service of Notice

- 12. Comment on Recent Case Law by Madras High Court

- 13. Comment on Complexities involved

Page Contents

- 1. What is E-Assessment Scheme, 2019?

- 2. Whether the Scheme is applicable for all type of assessments under Income Tax Act, 1961?

- 3. E-assessment Scheme prevail over contradicting provisions of Income Tax Act, 1961

- 4. E-assessment Centres

- 5. Communication

- 6. Procedure for E-assessment

- 7. Role of Jurisdictional Assessing Officer

- 8. Appeal against assessment order

- 9. Delivery and Service of Electronic Record

- 10. Personal Appearance by the assessee

- 11. Comment on Validity of Jurisdiction and Service of Notice

- 12. Comment on Recent Case Law by Madras High Court

- 13. Comment on Complexities involved

1. What is E-Assessment Scheme, 2019?

It is a scheme made in accordance with Section 143(3A) of Income Tax Act, focused towards eliminating the physical appearance and interface between the assessing officer and the assesse so as to impart greater efficiency, transparency, and accountability in assessment procedures.

2. Whether the Scheme is applicable for all type of assessments under Income Tax Act, 1961?

No. The scheme obtains its powers from Section 143(3A) of Income Tax Act, which clearly states that scheme is applicable for assessment under Section 143(3) of Income Tax Act, 1961. Thus, as of now, the Scheme is not applicable for assessment under Section 147/ 148 (Income escaping assessment), Section 153A/ 153C (Search or requisition), Section 271/ 270A (Penalty assessment) etc.

3. E-assessment Scheme prevail over contradicting provisions of Income Tax Act, 1961

3. E-assessment Scheme prevail over contradicting provisions of Income Tax Act, 1961

Section 143(3B) of Income Tax Act, 1961 empowers Central Government for purpose of giving effect to scheme, to direct that any provisions of the Act shall not apply or shall apply with such exceptions, modifications and adaptations as may be specified. Accordingly, the Central Government has issued N/N 62/ 2019 dated 12-Sep-19 which entails the supremacy of Scheme over various provisions of Income Tax Act including Section 120 (Jurisdiction), Section 282/ 283/ 284 (Service of Notice), Chapter XXI (Penalty) etc.

4. E-assessment Centres

CBDT may set up following units/ centre for smooth conduct of e-assessment proceedings and specify their respective jurisdiction:

- National e-assessment Centre (NeAC): To facilitate conduct of e-assessment proceedings in a centralised manner

- Regional e-assessment Centre (ReAC): To facilitate conduct of e-assessment proceedings in the cadre controlling region of Principal Chief Commissioner

- Assessment Units (AU): To perform function of making assessment

- Verification Units (VU): To perform function of verification, including enquiry, cross verification, examination of books/ witnesses etc.

- Technical Units (TU): To perform function of technical assistance, including advice on legal, accounting, IT, valuation etc.

- Review Units (RU): To review draft assessment order

5. Communication

All communication among AU, VU, TU, RU, assesse or any other person shall be done through NeAC with respect to information or documents or evidence or any other details and thus, no communication is directly done between them.

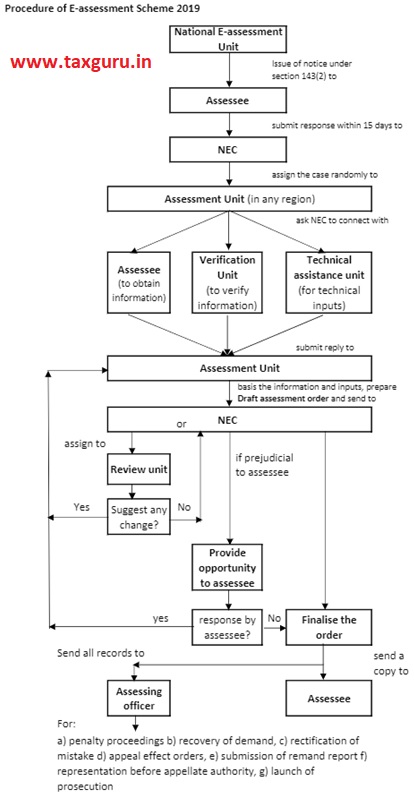

6. Procedure for E-assessment

- NeAC shall serve mandatory notice u/s. 143(2) of Income Tax Act, 1961 to taxpayer specifying the issue for selection of his case for assessment.

- Taxpayer may file response to NeAC within 15 days from the date of receipt of notice.

- NeAC shall assign case to specific assessment unit in any one ReAC through automated allocation system.

- Assessment unit may make request to NeAC for:

(a) obtaining such further information, documents or evidence from the assesse or any other person, as it may specify;

(b) conducting of certain enquiry or verification by verification unit; and

(c) seeking technical assistance from the technical unit;

- Upon receipt of such request from AU, NeAC shall issue appropriate notice etc. to assessee or any other person or assign request to verification unit/ technical unit, as the case may be.

- Assessment unit shall after taking into account all relevant material available on record, make in writing, a draft assessment order and send a copy of such order to NeAC.

- Assessment unit shall provide details of penalty proceedings to be initated therein, if any, while making draft assessment order.

- NeAC shall examine the draft assessment order in accordance with Risk Management Strategy specified by the Board, including by way of an automated examination tool, whereupon, it may decide to:

(a) finalise the assessment as per the draft assessment order and serve a copy of such order and notice for initiating penalty proceedings, if any, to the assessee, alongwith the demand notice, specifying the sum payable by, or refund of any amount due to, the assessee on the basis of such assessment;or

(b) provide an opportunity to the assessee, in case a modification is proposed, by serving a noticecalling upon him to show cause as to why the assessment should not be completed as per the draftassessment order; or

(c) assign the draft assessment order to a review unit, for conducting review of such order.

- Review Unit shall conduct review of draft assessment order, whereupon it may decide to:

- Concur with draft assessment order; or

- Suggest such modification, as it may deem fit and send it to NeAC, which in turn shall send it to Assessment Unit

- Assessment unit shall after considering the modifications, send the final draft assessment order to NeAC

- The assessee may, in case where SCN is issued, furnish response to NeAC on or before the date and time specified in the notice.

- NeAC shall finalise order where no response to SCN is received.

- Where response is received, it shall be send to Assessment Unit, which in turn, after taking into account such response, may make revised draft assessment order to NeAC.

- The NeAC shall, upon receiving the revised draft assessment order,-

(a) in case no modification prejudicial to the interest of the assessee is proposed, finalise the assessment as per the specified procedure; or

(b) in case a modification prejudicial to the interest of the assessee is proposed with reference to the draftassessment order,provide an opportunity to the assessee,

(c) the response furnished by the assessee shall be dealt with as per the prescribed procedure

7. Role of Jurisdictional Assessing Officer

- NeAC may at any stage of the assessment, if considered necessary, transfer the case to the Assessing Officer having jurisdiction

- Also, where assessment is completed electronically, NeAC shall transfer all electronic records pertaining to case to jurisdictional AO for:

√ Imposition of penalty

√ Collection and recovery of demand

√ Rectification of mistake

√ Giving effect to appellate orders

√ Submission of remand report etc. or any representation to be made before CIT(A), ITAT or Courts

√ Proposal seeking sanction for launch of prosecution and filing of complaint before the Court

8. Appeal against assessment order

Appeal against E-assessment order shall lie with Commissioner (Appeals) having jurisdiction over the jurisdictional AO.

9. Delivery and Service of Electronic Record

- Every notice or order or any other electronic communication under this Schemeshall be delivered to the addressee, being the assessee, by way of-

(a) placing an authenticated copy thereof in the assessee’s registered account; or

(b) sending an authenticated copy thereof to the registered email address of the assessee or his authorised representative; or

(c) uploading an authenticated copy on the assessee’s Mobile App; and followed by a real time alert.

- Every notice or order or any other electronic communication under this Scheme shall be delivered to the addressee, being any other person, by sending an authenticated copy thereof to the registered email address of such person, followedby a real time alert.

- The Assessee shall file his response to any notice or order or any other electronic communication, under this Scheme, through his registered account, and once an acknowledgement is sent by the National e-assessment Centre containing thehash result generated upon successful submission of response, the response shall be deemed to be authenticated.

- The time and place of dispatch and receipt of electronic record shall be determined in accordance with the provisions of section 13 of the Information Technology Act, 2000 (21 of 2000).

10. Personal Appearance by the assessee

- A person shall not be required to appear either personally or through authorised representative in connection with any proceedings under the Scheme.

- Where modification is proposed in draft assessment order and opportunity is provided to taxpayer, the taxpayer or authorised representative shall be entitled to seek personal hearing so as to make his oral submissions and such hearing shall be conducted exclusively through video conferencing.

- Further, NeAC has the power to transfer the case at any time to the jurisdictional AO, if considers necessary.

11. Comment on Validity of Jurisdiction and Service of Notice

As per existing provisions of Income Tax Act, 1961, jurisdiction over assessee resides with local Income Tax Authority and service of notice can be made through various modes as prescribed. However, this scheme over-rules such provisions and gains much liberty and power in terms of exercise of jurisdiction and validity of service of notice. The assessment can be done by any officer allocated through System and further, service of notice can be done at various addresses on record. To enable so, Section 143(3B) has been introduced by Finance Act, 2018 and further notification has been brought by Central Government in Sep’19.

12. Comment on Recent Case Law by Madras High Court

The Madras High Court in the case of Salem Sree Ramavilas Chit Company Vs DCIT [W.P. No. 1732 of 2020] has opined that the faceless tax-assessment system “can lead to erroneous assessement, if officers are not able to understand the transactions and statement of accounts of an assessee without a personal hearing”. At the same time, the Hon’ble Court has said that “it is laudable steps taken by the Income Tax Department to pave way for an objective assessment without human interaction”.

The Hon’ble Court finally made observations and held as follows:

“In my view, the petitioner has prima-facie demonstrated that the assessment proceeding has resulted in distorted conclusion of facts.” It sets aside the department’s order and asked the AO to pass fresh order within 60 days.

In view of above judgment and inherent shortcoming in E-assessment scheme, it may face further litigation in times to come.

13. Comment on Complexities involved

As all communication flows in the form of electronic records, filing of bulky submission files may pose challenge before the taxpayer as well as tax authorities. Taxpayer may be required to prepare, scan and upload various submission/ supporting documents and on the other hand, tax authorities may face problem in verification of such electronic files.

Also, as assessee has the power to make oral submissions through video conference etc., the success of the scheme will depend mainly on the availability of video conferencing facility including telecommunication application software which supports video telephony. Board may set-up these facilities as earliest to ensure smooth functioning of the Scheme.

Disclaimer: All efforts have been made to avoid errors or omissions. The information provided is for general informational purposes only. All the contents are merely views expressed by the authors. While it is tried to keep the information up-to-date and correct, there are no representations or warranties, express or implied, about the completeness, accuracy, reliability or suitability with respect to the information or related graphics contained for any purpose. Authors will not be responsible for any damage or loss to any one, of any kind, in any manner.

What is the date of its applicability

In case, order is passed without initiation of penalty, whether jurisdictional A.O. can commence penalty proceeding?

whether e-assessment is applicable for income escaping assessment?

Is it applicable for penalty assessment ?

Well explained. Thank you.