Upon recommendation of 38th GST Council meeting held of 18.12.2019, CBIC has recently released Circular No. 129/48/2019 dated 24.12.2019, define Standard Operating Procedure to be followed in case of non-filers of GST Return under section 39, 44 and 45 of CGST Act 2017.

It provides for –

> Sending system generated massage to registered person before due date to nudge them to file return on time;

> Sending system generated mail/massage to all defaulters if return not filed within due date

> Sending electronically notice to all defaulters after 5 days to file return with in 15 days

> Allowing Proper Officer to proceed for Best Judgment Assessment if return not filed.

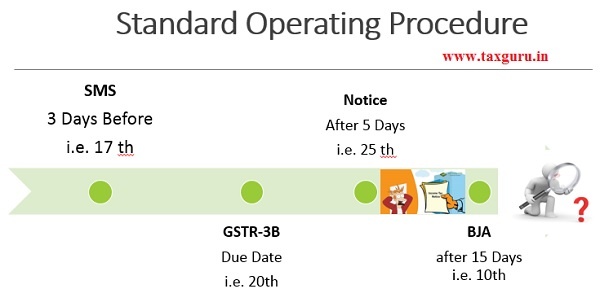

Steps of Standard Operating Procedure

- Step -1 :- 3 days before SMS shall be sent to all registered person to file GSTR-3B.

- Step -2 :- Up 5 days from due date, Mail / SMS shall be sent to all defaulters if return is not filed on due date to file return.

- Step -3 :- After 5 days, a notice [Form-GSTR 3A] shall be issued to file return with in 15 days i.e. up to 10th of next month.

- Step -4 :- After 15 days, if return is not filed, Best Judgment assessment shall be made by Proper Officer.

Best Judgment Assessment [BJA]

Under Section 62 of the CGST, the Proper Office may proceed to access tax liability to the best of his judgment taking into account all the relevant material which is available / gathered :

- Return of Outward Supply i.e. GSTR -1;

- Details of supplies auto populated i.e. GSTR -2A;

- Information available in e-way bills;

- Any other information from any other source i.e. inspection etc.

However, if defaulter furnish a valid return with 30 days of service of assessment [Form GST ASMT 13] order, the said assessment order shall be deemed to have withdrawn.

You can reach us at : somvirkataria@live.in or can call us at 9911166244

Author Bio