Deduction of taxes at source has been an integral part in the history of Indian Income Tax. However the concept of TDS has also been incorporated in the GST Act(s). The basic concept remains the same that is withholding a certain percentage of amount as tax before paying the contract value to the supplier in order to maintain a trail of transactions and avoid evasion of taxes. However applicability and other provisions regarding TDS in GST are completely different from Income Tax. Also the two are completely unrelated in all aspects.

Provisions for Tax deducted at source under GST has been provided in Section 51 of the CGST Act 2017 ;

51. (1) notwithstanding anything to the contrary contained in this Act, the Government may mandate,––

(a) a department or establishment of the Central Government or State Government; or

(b) Local authority; or

(c) Governmental agencies; or

(d) Such persons or category of persons as may be notified by the Government on the recommendations of the Council,

(hereafter in this section referred to as “the deductor”), to deduct tax at the rate of one percent. from the payment made or credited to the supplier (hereafter in this section referred to as “the deductee”) of taxable goods or services or both, where the total value of such supply, under a contract, exceeds two lakh and fifty thousand rupees:

Provided that no deduction shall be made if the location of the supplier and the place of supply is in a State or Union territory which is different from the State or as the case may be, Union territory of registration of the recipient.

Explanation.––For the purpose of deduction of tax specified above, the value of supply shall be taken as the amount excluding the central tax, State tax, Union territory tax, integrated tax and cess indicated in the invoice.

Applicability of the section:

⇒ This section shall apply to the above mentioned categories of persons w.e.f. 01/10/2018 for both interstate and intra state supplies

Non-Applicability of the section:

Following are the situations where Tax deduction is not required:

a) Total value of taxable supply ≤ Rs. 2.5 Lakh under a contract.

b) Contract value > Rs. 2.5 Lakh for both taxable supply and exempted supply, but the value of taxable supply under the said contract ≤ Rs. 2.5 Lakh.

c) Receipt of services which are exempted.

d) Receipt of goods which are exempted.

e) Goods on which GST is not leviable. For example petrol, diesel, petroleum crude, natural gas, aviation turbine fuel (ATF) and alcohol for human consumption.

f) Where a supplier had issued an invoice for any sale of goods in respect of which tax was required to be deducted at source under the VAT Law before 01.07.2017, but where payment for such sale is made on or after 01.07.2017 [Section 142(13) refers].

g) Where the location of the supplier and place of supply is in a State(s)/UT(s) which is different from the State / UT where the deductor is registered. **See Note below

h) All activities or transactions specified in Schedule III of the CGST/SGST /UTGST Acts 2017, irrespective of the value.

i) Where the payment relates to a tax invoice that has been issued before 01.10.2018.

j) Where any amount was paid in advance prior to 01.10.2018 and the tax invoice has been issued on or after 01.10.18, to the extent of advance payment made before 01.10.2018.

k) Where the tax is to be paid on reverse charge by the recipient i.e. the deductee.

l) Where the payment is made to an unregistered supplier.

m) Where the payment relates to “Cess” component.

**As provided above, that no deduction shall be made if the location of the supplier and the place of supply is in a State or Union territory which is different from the State or as the case may be, Union territory of registration of the recipient.

To understand this better, let us consider the following situations:

Situation 1: Location of Supplier: Assam

Location of Recipient: Assam

Place of Supply : Assam

Solution: Tax to be deducted (CGST +Assam SGST/UTGST)

Situation 2: Location of Supplier: Meghalaya

Location of Recipient: Assam

Place of Supply : Assam

Solution: Tax to be deducted (IGST)

Situation 3: Location of Supplier: Assam

Location of Recipient: Meghalaya

Place of Supply : Assam

Solution: No Tax to be deducted

Applicable Rate:

A total tax of 2% has to be deducted as per the provisions of the section, bifurcation of which is as under:

Intra State Supply IGST @ 2%

Inter State Supply CGST @ 1% and SGST/UTGST/UTGST@ 1%

Threshold Limit:

As per the said section, tax at source is to be deducted only if the value of a contract exceeds Rs. 2,50,000.However the contract value defined should be exclusive of GST.

For better understand of the definition of the contract value, let us consider certain situations.

Situation 1: A PSU has entered into a contract with a supplier, the value of which is Rs.236000 (including GST of 36000)

Solution: No requirement of GST-TDS.

Situation 2: A PSU has entered into a contract with a supplier, the value of which is Rs.306800 (including GST of 46800)

Solution: GST to be deducted @ 2% (CGST(1%)+SGST/UTGST(1%) or IGST(2%) will depend on the location) on Rs.260000 i.e. the contract value excluding the GST amount.

Situation 3: A PSU has entered into a contract with a supplier, the value of which is Rs.472000 (including GST of Rs. 72000), however payment is made on 8 individual invoices of RS.59000(including GST of Rs.9000)

Solution: GST to be deducted @ 2% (CGST(1%)+SGST/UTGST(1%) or IGST(2%) will depend on the location) on Rs.260000 i.e. the contract value excluding the GST amount. No significance of individual invoices being less than the threshold amount.

TDS on Advance payments:

Tax is required to be deducted on advance payments also, if the contract value exceeds the threshold limit as provided.

Transitional Provisions:

TDS provisions under GST are applicable w.e.f . 01.10.2018. There will not be any retrospective effect of the same

As such, the under mentioned situations come into picture:

- If an invoice is issued on 01.09.2018, but payment is made on 04.11.2018, TDS provisions shall not apply irrespective of the value of contract.

- If an invoice is issued on 01.11.2018 amounting to Rs.10 lakhs, but advance payment is made on 04.07.2018 for Rs.2 lakhs, TDS provisions shall apply to the balance amount of 8 lakhs only, i.e. no retrospective effect

Procedural aspects:

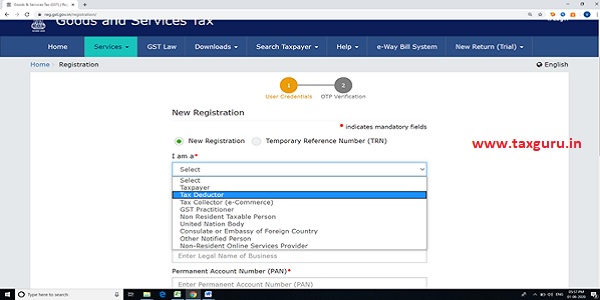

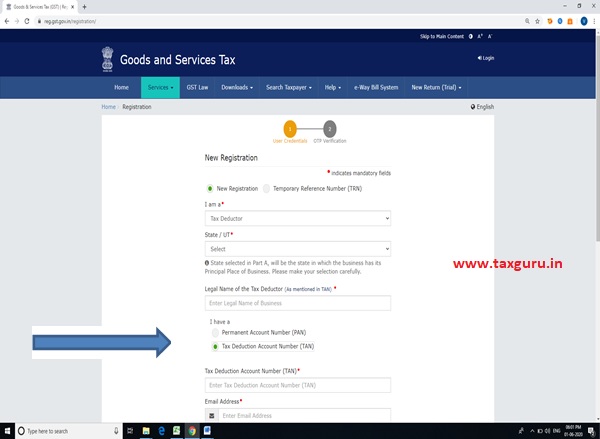

Registration Requirement and Procedure: Any person required to deduct TDS under section 51 shall take mandatory registration as “Tax Deductor”. This registration shall be over and above the registration as Tax Payer i.e. A deductor in GST will be required to get registered and obtain a GSTIN as a TDS deductor even if he is separately registered as a supplier.

I am a “Tax Deductor” needs to be selected from the drop down list.

Registration as tax deductor can be PAN based or TAN based as the case may be. However on a plain reading, if the assessee fulfils the criteria of tax deduction under Section 51 of CGST Act, it will definitely be a Tax Deductor in Income Tax also. Therefore registration under GST -TDS are mostly TAN based.

However in cases where the assessee has both PAN and TAN, it is his discretion as to take registration based on PAN or TAN.

Documents Required for Application for Registration as Tax Deductor

| Document Name | Document Type | Document Size |

| Proof of Drawing and Disbursing Officer | ||

| Photo of the Drawing and Disbursing Officer | JPG | 100 KB |

| Proof of Appointment of Authorised Signatory | ||

| Photo of the Authorised Signatory | JPG | 100 KB |

| Letter of Authorisation/ Copy of Resolution passed by BoD/ Managing Committee and Acceptance letter | JPG, PDF | 100 KB |

| Proof of Principal Place of business | ||

| Own:

Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

JPG, PDF | Property Tax Receipt – 100 KB

Municipal Khata copy – 100 KB Electricity bill copy – 100 KB Rent/ Lease agreement – 2 MB Consent Letter – 100 KB Rent receipt with NOC (In case of no/expired agreement) – 1 MB Legal ownership document – 1 MB |

| Leased:

Rent/ Lease agreement OR Rent receipt with NOC (In case of no/expired agreement) AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

JPG, PDF | |

| Rented:

Rent/ Lease agreement OR Rent receipt with NOC (In case of no/expired agreement) AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

JPG, PDF | |

| Consent:

Consent letter AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

JPG, PDF | |

| Shared:

Consent letter AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

JPG, PDF | |

| Others:

Legal ownership document |

JPG, PDF | |

Table Source: www.gst.gov.in

Form for registration: GST REG-07.

Form for certificate of registration: GST REG-06.

Challan generation for depositing the deducted tax

The deductor has to generate a challan in the portal at www.gst.gov.in and deposit the tax so deducted through e-payment mode [Net Banking/Debit-Credit card/NEFT-RTGS] or OTC Mode [Cash/Cheque/DD].

Tax deposited by challan would get credited in the electronic cash ledger of the deductor

Refund of Tax: Any excess amount is deducted and paid to the government; a refund can be claimed as this was erroneously deposited

However, if the deducted amount is already added to the electronic cash ledger of the supplier, the amount so added cannot be got back as a refund by the deductor. Deductee can claim a refund of tax subject to refund provisions of the act.

Return Filing: A return in Form GSTR-7 is required to be filed by the 10th of the succeeding month in which such tax deduction is made.

Say, a PSU has made a payment of Rs.300000 on 14th September 2019, and deducted the due tax, the amount so deducted has to be paid and return to be filed in GSTR-07 on or before 10th of October 2019.GSTR-7 can be filed in both online and offline mode.

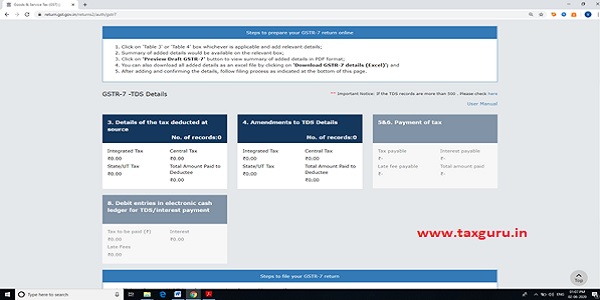

Contents of GSTR-7

1. GSTIN of the deductor (Table 1)

2. Business Details (Table 2): This table consists of the following details:

3. Details of the tax deducted at source (Table 3): This table consists of the following details:

- GSTIN of the deductee

- Trade Name/Legal name of the deductee

- Amount paid to deductee on which tax is deducted.

- Amount of tax deducted at source (CGST, SGST, IGST)

4. Amendments to TDS Details (Table4): Amendments in respect of previous tax periods needs to be entered in this table. On entering the financial year, month and GSTIN of the deductee , the record entered earlier shall pop up and the required amendments can be made. Also any modification in the record rejected by deductee has to be done in this table. An important point to be noted here is that until an action is taken ( modification made) in any record rejected by the deductee, portal will not allow the deductor to file his return for the next period. Therefore necessary modifications will have to be made first in this table.

5. Payment of Tax (Table 5 & 6): Here details of tax, interest and fee balance in cash ledger is provided along with details of Tax, Interest and fee payable according to the details entered in the previous tables. The deductor and therefor set of his liability or create new challan and make necessary payment as required.

7. Debit entries in electronic cash ledger for TDS/interest payment (Table 8): This table is not required to be filled manually; shall be populated after payment of tax along with debit entry number and debit entry date.

Nil Return Requirement: Unlike the monthly returns for GST Taxpayers, GSTR-7 need not be filed if there is no deduction of tax during any particular month.

Issue of TDS Certificate in GSTR 7A: After filing FORM GSTR-07 on or before 10th of every month, deductor is required to issue a TDS certificate in FORM GSTR-7A giving details of the GSTIN of the supplier (deductee), invoice details, value of supply made and tax deducted thereon within five days.

Some important aspects about GSTR 7A:

- Time limit as mentioned above

- It can be downloaded from the GST Portal; Services>User Services>View/Download Certificate Option

- The deductee has to accept/reject the details filed by the deductor in his GSTR 7. GSTR 7A can be downloaded only if the deductee has accepted the details. In case of rejection, the deductor will have to make the necessary corrections before filing the return for the next month

- No signature is required since it is a system generated certificate

- Only one certificate will be generated for each GSTIN containing details about all supplies on which tax has been deducted during the month

- GSTR 7A can be downloaded only after the deductee has accepted the same

- No bulk download option is available i.e. deductor has to download each certificate separately for all GSTIN

Claim of Tax Credit by Deductee: The amount of TDS appears as a credit in the electronic cash ledger of the deductee and can be used by him while filing his monthly return in GSTR 3B. The detail of TDS deducted is available electronically to each of the deductees in Form GSTR 2A after the due date of filing of Form GSTR 7.

Provisions related to Penalty:

TDS not deducted or deducted but not deposited to the Government Account: Interest to be paid along with TDS amount; else the amount shall be determined and recovered as per law.

Delay in filing of GSTR 7: In such a case, the deductor is liable to pay interest not exceeding 18% p.a. along with TDS amount and a late fee of Rs.200/ day (SGST/UTGST-Rs.100 and CGST-Rs.100), subject to a maximum of Rs.5000 each under SGST/ UTGST and CGST Act. However no late fee is applicable for delay in filing of NIL returns.

Delay in issue of TDS Certificate i.e. GSTR 7A: In this case, the deductor is liable to pay a late fee of Rs.200/ day (SGST/UTGST-Rs.100 and CGST-Rs.100), subject to a maximum of Rs 5,000 each under SGST/UTGST and CGST Act.

Author Bio