The transport sector is one of the most important sectors of our economy where large numbers of industry and people are connected either directly or indirectly. Most of the industries use their services for rendering their supply either in goods or services. Due to the various challenges associated with the sector, the government always allows some relaxation whether it is in the form of presumptive taxation in income tax or reverse charge mechanism for GTA. In this sector there are multiple dimensions which needs to be seen, however, in this article, I am trying to bring the difference between Goods transport agency and person who owns truck commonly known as transporter who may give transportation service either himself or through a transport agent i.e. GTA.

Page Contents

WHO IS GOODS TRANSPORT AGENT

As per the explanation in Notification no. 11/2017 central Tax rate .—”Goods transport agency” means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called.

It is important to note that for qualifying as GTA there are two important conditions

1) Provision of Service of transport of goods by road and

2) Issue of Consignment note (by whatever name called)

The word “and” between both sentences clarifies that both the conditions need to be satisfied for falling under the definition of Goods Transport Agency (GTA)

WHAT IS A CONSIGNMENT NOTE?

“Consignment Note” means a document, issued by a GTA against the receipt of goods for the purpose of transport of goods by road in a goods carriage, which is serially numbered and contains :

| • | the name of the consignor and consignee, |

| • | registration number of the goods carriage in which the goods are transported, |

| • | details of the goods transported, |

| • | details of the place of origin and destination, |

| • | Person liable to pay GST – whether consignor, consignee or the goods transport agency. |

RATES & EXEMPTION TO GTA & TRANSPORTERS

As per entry in Notification no.11/2017 Central Tax Rate the service of GTA is taxable and they have two options:

Services of goods transport agency (GTA) in relation to transportation of goods (including used household goods for personal use).

Option –I

5% – Provided that credit of input tax charged on goods and services used in supplying the service has not been taken.

Option –II

12% – Where the credit of input tax charged on goods and services used in supplying the service has been taken and the goods transport agency need to 12% on all the services of GTA supplied by it.

EXEMPTION

As per Entry 18 of Notification No.12/2017 Central Tax Rate

Services by way of transportation of goods—

| (a) | by road except the services of— | |

| (i) | a goods transportation agency; | |

| (ii) | a courier agency; |

As per the above entry transportation service of goods other than by GTA and courier agency is exempt. Hence the services of transporters who are not goods transport agent are exempt under GST. The services of truck owners who provide transport service under some other GTA (means consignment note issued by another person) are exempt from GST.

SUB-CONTRACTING IN ROAD TRANSPORTING SECTOR

There are situations where one GTA takes the help of another in the form of subcontract of work. In the industry, subcontractor GTA bills another GTA for subcontracting service and the main GTA bills the actual service receiver. It is generally seen that subcontractor person who is actually providing transportation service on behalf of other GTA, charges tax from the main contractor which actually seems to be an exempt supply. Let us elaborate on the issue and discuss in detail.

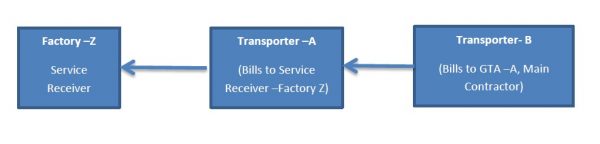

In the above transaction, Factory Z has asked bulk transportation services from “A”. Transporter “A” unable to execute it fully takes services of transporter “B” as a subcontract. It is to be noted that since the contract has been given to A, the consignment note will be issued by A and not by B.

“A” and “B” are registered entity and are availing the input tax credit (ITC) option and thereby charging 12% GST in the forward charge mechanism. In the above transaction can GTA –B can raise a taxable invoice and recover 12% tax from GTA-A. Let’s see.

As per the definition of GTA as stated above it is very clear that person who issues consignment note will be treated as goods transport agency. In the above case, “A” issues consignment note, so GTA for the transaction will “A”. Any services by way of transportation of Goods by road other than through GTA would be exempt supply as per the entry of notification as quoted in the above paragraph. In the given case “B” is providing the transportation service but not as GTA but only as a truck owner to GTA “A” which is very much covered by the exemption entry of the notification quoted above. Hence the transaction between A & B will be an exempt supply and A & Z will be the only taxable supply.

Can transporter “B” issues another consignment note for the same transaction to “A” and thereby retain the character of GTA for the transaction. A consignment note is proof of the custody of goods during the movement and transportation of goods. For a single transaction and the same movement of goods, there cannot be multiple consignment notes. Hence there will be one consignment note for movement of Goods to a place.

Now with the above discussion, we found that service of main transporter contractor “A” who issues consignment note will taxable and services of “B” will be exempt.

REVERSAL OF INPUT TAX CREDIT

Transporters who are acting as “GTA” is some cases and acting as subcontractor (merely a transporter –truck owners) need to reverse the input tax credit as per rule 42 and 43 of GST act. These transporters avail significant portion of the Input tax credit from the purchase of trucks and chassis, which is capitalized in the books of accounts. The transporters buy and sell trucks and fleets during the year based on their needs and age of the vehicle. The compliance of rule 43 for availability and reversal of ITC on capital goods becomes a very challenging task for the whole sector. As we are aware, compliance of rule 43 requires reversal of credit for 60 months from the date of invoice, which again create a need of keeping the working and reconciliation ready to justify the same.

Rule -44 of the act will also come into the picture when an asset which was capitalized and input tax credit was availed is sold off prior to completion of 5 years. All these compliances add challenges for the sector for right availment and reversal of input tax credit in light of the provision of Rule 42, 43 & 44. Transportation sector which always has been given some or other relaxation in preparing and maintain records is now facing tuff time to maintain ITC records pertaining to availment and reversal of the same.

CONCLUSION

In the industry many transporters are still not treating the subcontracted service as exempt services and thereby issuing tax invoices to the main GTA, may be knowingly or unknowingly and even skipping the reversal of credit as stated in the above paragraph. In this article, I have tried to explain the above issue of reversal of ITC for transporters who are registered, availing credit and providing services also as a subcontractor or mere like truck owners.

Author Bio

sir my question, whether B Is Register dealer and also he also do transportation, but sub contract taken from A some part of main transport contract from A, whether he has file Rcm to A and wt abt A, he has file Rcm show liability to Z factory without payment of rcm plz clarifies me

Dear sir i am sub transporter. I provide lorries to main TRANSPORT for transportation. I dnt have any registration. I give them bill for my lorries which i provide them.sir i want to know i need gst registration or not.our transactions is havey.kindly suggest me.

Can sub-contractor charges GST@12% to main transporter with LR (Consignee note)

Covered topic and issue in very lucid manner….

Keep it up

Sir Regarding GTA I have a Query :-

Suppose if I am an Transporter register under GTA where my Customer is paying the GST under Reverse Charge Mechanism on my behalf.

Many times I use other Transporters Truck who are Un-Registered under GST or don’t have GST Registration for transporation of my Customer Goods on my behalf where I am issuing the Bill to my Customer and where my Customer is paying GST under Reverse Charge Mechanism.

Point is am I eligible to pay reverse charge on such Third Party Transporter vehicle used.

If I am paying Reverse Charge on Such Services availed then Can I take GST Input Credit on such RCM Amount paid on such Third Party Customer Truck availed.

Please resolve my Query.

Regards,

MANOHAR RAI

Nice Article.Thanks Sir.as you said G.T.A Sector has become cumbersome due to present G.S.T provisions.Looking forward for such good articles.