As with implementing any law in a diverse and business oriented country of 1.3 billion people, GST has also had it’s fair share of ups and downs. The debate and discussions of what could have been better is a never ending one. However, over the 2 years since implementation, the country has slowly adapted to the new tax regime and the dust seems to be finally settling down. In an aid to further fastrack this process, for a while now the GST Council and Ministry of Finance have been talking about simplifying the framework of returns to help the industry better comply with the law and reduce compliance costs and burden. With this, the council has proposed to introduce a single return “GST RET – 1” which in turn will have two separate annexures “GST ANX – 1” and “GST ANX – 2”. The idea behind this change is that it replaces the need for multiple returns (GSTR – 1, 2, 3/3B) with one single return. Further, to aid MSME’s and small businesses, the Council has also proposed to introduce “GST RET – 2” or “SAHAJ” and “GST RET – 3” or “SUGAM” which provides taxpayers with the option of filing returns quarterly based on turnover and few other criteria.

While the objective and effort with this proposed change is to simplify the existing framework, am not sure if it would actually end up achieving that objective. Let’s understand each of the new returns to see how different or similar it is with the current framework.

First and foremost, let’s understand what the criterion’s to choose GST RET – 1, 2, 3 are:

- If your aggregate turnover is above Rs. 5 Crores, it is mandatory to file GST RET – 1.

- Small businesses with turnover less than Rs. 5 Crores and with only end consumers as customers (B2C) can opt to file GST RET – 2 on a quarterly basis.

- Small businesses with turnover less than Rs. 5 Crores but with both B2B and B2C Sales can opt to file GST RET – 3 on a quarterly basis.

But hold on, it’s not quite as simple. Registered taxpayers who opt for GST RET – 2 and GST RET – 3 are not allowed to take input on missing invoices. So what does this mean? Just like the envisaged framework of returns under the GST Law, the outward supplies made by the taxpayer are declared in “GST ANX – 1” (erstwhile “GSTR – 1”) and the data so declared is auto populated to the counter party in “GST ANX – 2” (erstwhile “GSTR – 2”) for claiming ITC on such supplies. So in case of taxpayers opting to file GST RET – 2 and GST RET – 3, i.e. SAHAJ and SUGAM, they would not be allowed to avail the ITC on invoices which are not uploaded by their vendor.

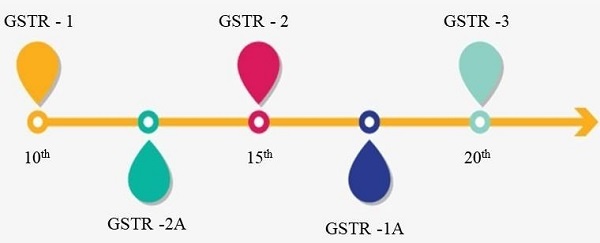

At this juncture, let’s rewind a little. The originally envisaged framework for the returns was as below:

It was mostly a fool proof plan. The supplies made by the taxpayer would be auto populated to the receiver who would claim ITC based on such details. But as we all know today, it was anything but. Among the endless list of reasons why it failed, the top ones were:

- The system was just not ready yet which caused endless chaos

- The unorganized business segment hadn’t even woken up to the new tax regime causing huge gaps in the chain of credit

- Inconsistency and endless extensions of deadlines

Let’s come back. With this background, does the new scheme of returns sound familiar? Of course it does, doesn’t it?

GSTR 1 = GST ANX 1

GSTR 2 = GST ANX 2

GSTR 3 = GST RET 1 / 2 / 3

The ideology hasn’t differed at all. We are circling back to the concept of real time uploads and matching of invoices to complete the credit chain in the system in the name of “New and Simplified Returns”. So here are a few challenges that’ll still continue to haunt the taxpayers:

- Timing difference – Due to inherent time taken in processing transactions and option of filing quarterly returns, there is a time lag in claiming ITC which leads to a need for reconciliation on a regular basis.

- Vendor Management – Regular follow up with vendors for uploading of invoices.

- Inconsistency in key fields – Prime example is invoice number. Invoice number is always accounted differently by different taxpayers. E.g. 001/ENG/2019-20 maybe accounted as 1-ENG-19-20. These issues cause hardship at the time of reconciliation.

- Availability of the system – As has always been a challenge, the robustness and readiness of the new system is a big challenge

The only ray of hope for a successful implementation of the new framework is that the GST, as a law, is slowly settling down which enables the taxpayers to pay more focus on getting this right. Only time will tell if this actually “simplifies” the process or not.

It is the same old wine albeit in a new bottle with a new label