Show Cause Notice Under GST- a complete analysis

What is Notice?

Notice” is used in the sense of “observe” or “warning”, to bring someone to the attention of. o On the other hand, the word “Notification” is used in the sense of “announcement” o Whenever our Clients get notice, we have to refer the Notifications. o Notices under GST are communications by the GST Authorities. A notice so issued, depending upon the purpose or action required from the taxpayer, can be called by different names, such as, Show-cause notice (SCN), Scrutiny Notice or Demand Notice.

Also Read: Show Cause Notice Under GST – Relevant case laws

Concept of Show Cause Notice

In the erstwhile Central indirect tax laws, concept of cause notice was in existence. Accordingly, provisions have been made for issue of show cause notice for recovery of demand under the relevant act. (for example Section 11of central Excise Act, Section 73 of Service tax law, Custom act etc. Therefore, it is not new for those who dealing in those acts. However, so far as State vat act it is new for the concerned. Of course, SCN being served on dealer before making ex-party assessment orders and for giving opportunity of being heard before taking any decision or order under vat acts. Show cause notice (in short SCN) has great significance in adjudication proceeding for mandatory compliance of principle of natural justice.

Show cause notice is mandatory requirement for raising any demand under GST act 2017 except payment of interest u/s 50 and assessment of non-filer of returns u/s 62 of the act. SCN is the foundation on which adjudicating authority has to build up case. It is the document served on the taxable person asking him to explain with reason as to why a particular course of action should not be taken against him. It must be speaking and well-reasoned. Issuance of show cause notice should be with open mind. Taxable person should be of clear view that it is only proposal and his reply will be considered before taking any decision

Issue of SCN is not only to make aware taxable person against whom the action is intended to be taken but must contain brief facts of case and grounds relied upon for proposed action and language in precision, the reading of which makes person understand the case that he has to defend . It should not be issued on assumptions and presumptions.

Allegations and finding in SCN should be supported by documentary evidences.

In SCN there should be prima facie opinion and not final opinion or conclusions. Primary purpose of SCN is only to put aggrieved person on the notice of the facts and necessary ingredients of charge so as to enable him effectively meet it. If adjudication order passed without issue of SCN order will be liable to set aside being contravention of statutory provisions and violation of principle of natural justice.

REASONS FOR GST NOTICES

1. Delay in filing of GSTR-1 and GSTR-3B consecutively for more than six months;

2. Mismatch in details reported between GSTR-1 and GSTR-3B;

3. Mismatch declaration in GSTR-1 and E-way bill portal;

4. Liable but has failed to obtain GST registration;

5. Mismatch of ITC claims found between GSTR-3B & GSTR-2A/2B

6. Non-payment/ Short-payment of GST liability;

7. Wrong availment of ITC/ Refund wrongly claimed;

8. Anti-profiteering cases;

9. non-furnishing of information return, within the time limit specified.

10.Failure to raise E-invoiceing

11.E-invoice and E-way bill amount does not tally and matched

Where SCN is required to be issued under CGST Act, 2017:

- Section 10 – Wrongful availment of Composition scheme

- Section 21 – recovery of credit distributed in excess by ISD

- Section 35 – failure to record supply of goods or services

- Section 50 – Interest on delayed payment

- Section 51 – Tax deduction at source in default

- Section 52 – Tax collection at source in default

- Section 63 – Discrepancy found in scrutiny of returns

- Section 65 – Detection of tax not paid or short paid during Audit

- Section 66 – Detection of tax not paid or short paid during special Audit

LIST OF CASES WHERE NOTICES ARE ISSUED

| Sl. No. | Notice in Form | Relating to | Action required |

| 1 | REG-03 | Registration related information (New or amendment) | Reply in REG-04 within 7 working days |

| 2 | REG-17 | SCN ‘’why the registration not be cancelled | Reply in REG-18 within 7 working days |

| 3 | REG-23 | SCN for revocation of cancellation of registration | Reply in REG-24 within 7 working days |

| 4 | GSTR-3A | Default notice to non-filers of GST returns | File GST returns (1/3B/4/8) within 15 days |

| 5 | CMP-05 | SCN non- eligibility to be a Composition dealer | Reply in CMP-06 within 15 days |

| 6 | RFD-08 | SCN on rejection of GST refund made | Reply in RFD-09 within 15 days |

| 7 | PCT-03 | SCN for misconduct by the GST Practitioner | Reply within SCN prescribed time limit |

| 8 | ASMT-02 | Addl. Information for Provisional assessment | Reply in ASMT-03 within 15 days |

| 9 | ASMT-06 | Addl. Information for final assessment | Reply in ASMT-03 within 15 days |

| 10 | ASMT-10 | Intimation of discrepancy in GST return after scrutiny | Reply in ASMT-11 within SCN time or

30 days |

| 11 | ASMT-14 | SCN – Assessment u/s.63 (BJ) | Personal appearance within 15 days |

| 12 | ADT-01 | Notice for conducting Audit u/s.65 | Attendance within time prescribed in the Notice |

| 13 | RVN-01 | Notice by Revisional Authority | Reply or Appear, with DRC-03 before 7

working days |

| 14 | DRC-01 | SCN for tax demand | Reply in DRC-06 within 30 days of the

Notice |

| 15 | DRC-10 | Notice for Auction of goods | Pay thro DRC-09 and appear as per the

Notice |

Specific provisions have been made to issue SCN before passing any adjudication order under GST act 2017.

The Proper Officer is required to issue SCN in the above referred proceedings under respective section in prescribed forms within prescribed time limit to start adjudication proceedings, on prima facie satisfaction of specified ingredients So far proceedings under section 73 or 74 it is mandatory to issue detailed SCN to person chargeable with tax along with summary of notice in FORM – GST -DRC-01.

It should contain brief facts of case, ground relied upon and amount of tax and interest . It should be issued within prescribed time limit u/s 73 (2) and 74 (2) . It is clearly provided in section 75 (7) that amount of tax, interest and penalty demanded in the order shall not be in excess of amount specified in notice and no demand shall be confirmed on the grounds other than grounds specified in the notice. However he has a discretion to reduce the amount of tax , interest on merit after considering representation to SCN .

Basic Features of a valid SCN

SCN is the foundation for Adjudication

- SCN can be issued only after a proper enquiry

- SCN should be in writing and unambiguous

- Intimation of demand to precede SCN

- Show Cause Notice must be a proper notice and not any communication

- Proper Service of SCN

Validity and legality of the SCN:

SCN can only be issued electronically on the common portal – Shri Shyam Baba Edible Oils Vs CCE (MP High Court) 2020-TIOL-2016-HC-MP-GST

It is trite principle of law that when a particular procedure is prescribed to perform a particular act then all other procedures/modes except the one prescribed are excluded -This principle becomes all the more stringent when statutorily prescribed.

DIN to be quoted on all communications (including emails): To be treated as invalid and deemed to have never been issued – Circular No. 122/ 2019 & Circular No. 128/ 2019.Pre- communication of the demand under Rule 142 – Similar to Pre-SCN consultation under the erstwhile laws – Amadeus India Pvt. Ltd – Del HC & Back Office IT Solutions; Notice must be clear and specific, vague allegations without containing all the details cannot be a valid notice – Brindavan Beverages 2007 (213) E.L.T. 487 (S.C.)

“The show cause notice is the foundation on which the department has to build up its case. If the allegations in the show cause notice are not specific and are on the contrary vague, lack details and/or unintelligible that is sufficient to hold that the notice was not given proper opportunity to meet the allegations indicated in the show cause notice.”

Service of Notice:

SECTION 169. Service of notice in certain circumstances. — (1) Any decision, order, summons, notice or other communication under this Act or the rules made thereunder shall be served by any one of the following methods, namely :—

(a) by giving or tendering it directly or by a messenger including a courier to the addressee or the taxable person or to his manager or authorised representative or an advocate or a tax practitioner holding authority to appear in the proceedings on behalf of the taxable person or to a person regularly employed by him in connection with the business, or to any adult member of family residing with the taxable person; or

(b) by registered post or speed post or courier with acknowledgement due, to the person for whom it is intended or his authorised representative, if any, at his last known place of business or residence; or

(c) by sending a communication to his e-mail address provided at the time of registration or as amended from time to time; or

(d) by making it available on the common portal; or

(e) by publication in a newspaper circulating in the locality in which the taxable person or the person to whom it is issued is last known to have resided, carried on business or personally worked for gain; or

(f) if none of the modes aforesaid is practicable, by affixing it in some conspicuous place at his last known place of business or residence and if such mode is not practicable for any reason, then by affixing a copy thereof on the notice board of the office of the concerned officer or authority who or which passed such decision or order or issued such summons or notice.

(2) Every decision, order, summons, notice or any communication shall be deemed to have been served on the date on which it is tendered or published or a copy thereof is affixed in the manner provided in sub-section (1).

(3) When such decision, order, summons, notice or any communication is sent by registered post or speed post, it shall be deemed to have been received by the addressee at the expiry of the period normally taken by such post in transit unless the contrary is proved. Service of Notice

Rule 142 –

(1) The proper officer shall serve, along with the

(a) notice issued under section 52 or section 73 or section 74 or section 76 or section 122 or section 123 or sec 124 or section 125 or section 127 or section 129 or section 130, a summary thereof electronically in FORM GSTDRC-01,

(b) statement under sub-section (3) of section 73 or sub-section (3) of section 74, a summary thereof electronically in FORM GST DRC-02, specifying therein the details of the amount payable.

(5) A summary of the order issued under section 52 or section 62 or section 63 or section 64 or section 73 or section 74 or section 75 or section 76 or section 122 or section123 or section 124 or section 125 or section 127 or section 129 or section 130 shall be uploaded electronically in FORM GST DRC-07*, specifying therein the amount of tax, interest and penalty payable by the person chargeable with tax.

- M/s Shri Shyam Baba Edible Oils vs The Chief Commissioner and another (W.P. No. 16131/2020)

6.1 A bare perusal of the aforesaid provision reveals that the only mode prescribed for communicating the show-cause notice/order is by way of uploading the same on website of the revenue.

……

8. It is trite principle of law that when a particular procedure is prescribed to perform a particular act then all other procedures/modes except the one prescribed are excluded. This principle becomes all the more stringent when statutorily prescribed as is the case herein.

Penalties under various section:

Section 122 for any reason other the reason of fraud or any willful misstatement or suppression of facts to evade tax, liable for penalty Rs.10000/- or 10% the dues

Section 123 penalty for failure to furnish information return (section 150) Rs.100 per day max 5000/=

Section 124 fine for failure to furnish statistics to the department up to 10000/- continues 100 per day subject to max Rs,25000/-

Section 125 contravening any provisions of the Act max Rs.25000/-

Section 126 general disciplines related to penalty (where the minor breach) less than 5000/-no penalty

Section 127 power to impose penalty in certain cases (where the PO is if the view that penalty is warranted but it is not covered under section 62,63,64,73,74,129, and 130) he can levy penalty after giving reasonable opportunity no outer limit

Section 128 power to waive penalty(the government may by NN waive in part or full referred in 122, 123, 125, or any late fees referred in section 47

Show Cause Notice and Natural Justice:

- Audi alteram partem (listen to other side)

- Nemo judex in re sua – the authority passing the orders should be free from bias

- and prejudice.

- Nemo judex in cause sua – No one should judge his own case (with rested

- interest)

- Proper Notice – contain time, authority, place and nature of hearing

- Proper hearing and not mere formality

- The affected parties should have right to scrutinize the documentary evidence collected.

Adjudication

- Adjudication should be proper, reasoned and not passed in hasty Adjudication should be proper, reasoned and not passed in haste

- Adjudication beyond show cause notice, not sustainable

- Adjudication should be an independent application of mind

- Recording of reasons must in Adjudication

- Delay in hearing and passing of order

- Pre-Consultation before issuance of SCN – Master Circular on 10th March,2017

- SCN can be quashed in certain cases by HC

Skills Required Litigation in GST (By GSTP’s)/Tax payers

Law aids the vigilant and not the dormant or laws aid/assist those who are vigilant, not those who sleep upon/over their rights – often noted by Court in cases of disallowing condonations.

- Presume Nothing

- Substantive and procedural law – Complete Knowledge

- Strong writing and oratory skills

- Reasoning – both Analytical and logical are important

- Handling legal and factual materials – Quantum as well complication

- Interpersonal skills – With team and with client

- Legal research Resources and Techniques – Knowledge and application

- Client’s development and retention. Quick decision making.

Instruction No. 02/2022-GST dated 22nd March 2022

CBIC Instructions No. 02/2022-GST dated 22nd March 2022 – Extract

- Standard Operating Procedure (SOP) for Scrutiny of returns for FY 2017-18 and 2018-19

- Interim SOP

- Directorate General of Analytics and Risk Management (DGARM) to select the GSTINs registered with Central tax authorities, whose returns are to be scrutinized

- DGARM would provide some relevant data (along with likely revenue implication) pertaining to the returns to be scrutinized

- Proper officer? Scrutiny of returns of a taxpayer may be conducted by Superintendent of

Central Tax in-charge of the jurisdictional range of the said taxpayer.

The proper officer shall conduct scrutiny of returns pertaining to minimum of 3 GSTINs per month.

- Scrutiny of returns of one GSTIN shall mean scrutiny of all returns pertaining to a financial year for which the said GSTIN has been identified for scrutiny

- Payments made through FORM GST DRC-03 may also be taken into consideration while communicating discrepancies to the taxpayer in FORM GST ASMT-10

- For proceeding under section 73 or section 74, monetary limits as specified in Circular No.

31/05/2018-GST dated 9th February 2018 shall be adhered to (Who can issue SCN?)

if the proper officer is of the opinion that the matter needs to be pursued further through audit or investigation to determine the correct liability of the said registered person, then he may refer the matter to the jurisdictional Principal Commissioner/Commissioner through the divisional Assistant/ Deputy Commissioner, for the decision whether the matter needs to be referred to Audit Commissionerate or Anti-evasion Wing of the Commissionerate, as the case may be

- Likely Discrepancies

- Taxable Supply as per R-1 > Taxable Supply as per 3-B

- Forward charge ITC as per 3B is not matching with ITC as per 2A – Whether mandatory till 09/10/2019?

- IGST availed on Import (3B/GSTR-9) not matching with 2A (courier bill of entry?)

- 16(4) violation- Suppliers have filed Return after due date of filing Return of September of Next FY (Is this fair?)

- RCM liability as per 3B not matching GSTR-2A. (TOS??)

- Delayed payment interest not paid (Net liability, ITC availed and not utilised)

- Blocked Credits availed and not reversed

- Other ITC Reversal not carried out (Rule 42/43.

Likely Discrepancies:

ITC claim – Registration of vendor cancelled retrospectively.

ITC claim – supplier has not furnished Form GSTR-3B

Outward supply in R-1 vs Outward supply in EWB

Turnover in GSTR-9 vs 26AS statement vs ITR

ISD ITC availed in Table 4A.4 vs appearing in 2A

Value of outward supply declared in 3B < Value of TDS and TCS furnished by the corresponding deductors or E-Commerce Operators in their Form GSTR- 7 (Supply vs payment).

Non reflection in GSTR-2A/2B – Whether ITC to be reversed?

No mechanism to rectify defects –No Online ledger confirmation

> Madras High Court in D.Y. Beathel Enterprises v. STO

> Hon’ble Madras High Court held that first the recovery action should be initiated against the seller and only in exceptional cases (e.g missing dealer, closure of business by the seller or the seller not having adequate assets etc.) department should proceed against the purchasers for reversal of credit availed. [2021] 127 taxmann.com 80/86 GST 400 (Mad.)

> Allahabad High Court in Jai Maa Jwalamukhi Iron Scrap Supplier Vs State of U.P Hon’ble Allahabad High court held that the invoice is primary evidence of the transaction.

> Unless the revenue authority disputes its genuineness, it cannot be lightly overlooked.

> Further, Hon’ble court observed that mere existence of some discrepancies may not have ever led the revenue authority to the conclusion that tax had been evaded or the transaction had not been disclosed. [2021] 127 taxmann.com 474 (Allahabad).

Non reflection in GSTR-2A /2B– Whether ITC to be reversed?

Chhattisgarh High Court, in Bharat Aluminium Company Ltd (BALCO) vs. Union of India Ors. – Interim Order Hon’ble Chhattisgarh High Court has granted interim stay on Recovery Order denying Input Tax Credit (ITC) due to mismatch GSTR-2A and Form GSTR3B, on a condition of deposit of 5% of the demand by the company

Sahil Enterprises v. Union of India [2021] 129 taxmann.com 233 (Tripura) Petitioner contended that after paying taxes to the seller at the time of purchases, the Petitioner has no control over the seller to ensure that such tax is deposited with the Government. Denying ITC to the Petitioner where they have already paid tax would amount to double taxation. The Hon’ble High Court held that the issue needs consideration and notice was issued to the Union of India.

Non reflection in GSTR-2A /2B– Whether ITC to be reversed.

Bharti Airtel (SC) It is imperative upon a registered person to maintain records regarding transactions between suppliers and the recipients based on their agreements, invoices and books of accounts, either manually or electronically.

Registered person has been provided with a common electronic portal or tax electronic portal,

which is only an enabler and a facilitator in bringing on board all the registered persons which include the supplier, recipient, registered person and other recipients. The efficacy of common electronic portal or so to say malfunctioning thereof, does not extricate the registered person from the primary obligation of self-assessment of tax liability as predicated.

Pre-Show Cause Notice – Legal provisions.

liability, he may make such submission Rule 142(1A)/(2A) : Similar to Pre SCN (Excise and Service Tax) Inserted w.e.f 9th Oct 2019

- R.142(1A) – Obligation of Proper Officer to issue Pre SCN

- The proper officer may (shall), before service of notice to the person chargeable with tax, interest and penalty, under sub-section (1) of section 73 or sub-section (1) of section 74, as the case may be, shall communicate the details of any tax, interest and penalty as ascertained by the said officer, in Part A of FORM GST DRC-01A.

- Rule 142(2A) – Reply by taxpayer

- Where the person referred to in sub-rule (1A) has made partial payment of the amount communicated to him or desires to file any submissions against the proposed liability, he may make such submission in Part B of FORM GST DRC-01A. (online).

–

Time-limit for issuance of Show Cause Notice & Order

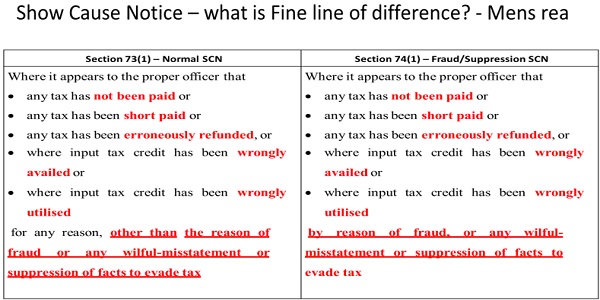

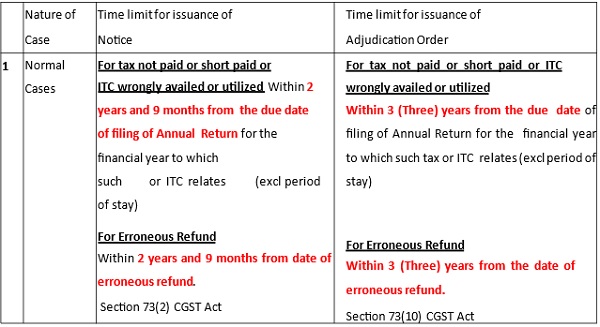

Section 73 – Normal Cases

Proper officer shall issue the notice at least 3 months prior to the time limit specified for issuance of order;

Proper officer shall issue order within:

3 years from the due date for furnishing of annual return for the financial year to which the tax relates; or

3 years from the date of erroneous refund.

Sec 74 – Cases involving fraud etc.

Proper officer shall issue the notice at least 6 months prior to the time limit specified for issuance of order;

Proper officer shall issue order within:

5 years from the due date for furnishing of annual return for the financial year to which the tax relates; or

5 years from the date of erroneous refund.

| FINANCIAL YEAR | NORMAL CASES | CASES INVOLVING FRAUD ETC |

| 2017-18 | Nov 05, 2022 | Aug 9, 2024 |

| 2018-19 | Sep 30, 2023 | June 30, 2025 |

| 2019-20 | Dec 21, 2023 | Sep 30, 2025 |

Time barring date for issue of SCN/orders – Normal SCN

SCN for new issue – Section 73(1) RELEVANT FORMS TO BE ISSUED:

R.142(1)(a) – The proper officer shall serve, along with the Notice issued under section 52 or section 73 or section 74 or section 76 or section 122 or section 123 or section 124 or section 125 or section 127 or section 129 or section 130, a summary thereof electronically in FORM GST DRC-01.

SCN for recurring issues/periodical SCN –

S.73(3) – Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement, containing the details of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for such periods other than those covered under sub- section(1), on the person chargeable with tax.

S.73(4) – The service of such statement shall be deemed to be service of notice on such person under sub-section (1), subject to the condition that the grounds relied upon for such tax periods other than those covered under sub-section (1) are the same as are mentioned in the earlier notice.

R.142(1)(b) – The proper officer shall serve, along with the Notice statement under sub-section (3) of section 73 or sub-section (3) of section 74, a summary thereof electronically in FORM GST DRC-02, specifying therein the details of the amount payable.

REPLY TO SHOWCASUE NOTICE:

S.73(9) – The proper officer shall, after considering the representation, if any, made by person chargeable with tax, determine the amount of tax, interest and a penalty equivalent to ten per cent. of tax or ten thousand rupees, whichever is higher, due from such person and issue an order.

S.74(9) The proper officer shall, after considering the representation, if any, made by the person chargeable with tax, determine the amount of tax, interest and penalty due from such person and issue an order

R.142(4) The representation referred to in sub-section (9) of section 73 or sub- section (9) of section 74 or sub-section (3) of section 76 or the reply to any notice issued under any section whose summary has been uploaded electronically in FORM GST DRC-01 under sub-rule (1) shall be furnished in FORM GST DRC- 06.

Time limit to reply SCN: Generally 30 days

DRC-06: Reply to the Show Cause Notice (online).

Full / Part Payment pursuant to SCN:

. 73(8) – Where any person chargeable with tax under sub-section (1) or sub-section

(3) pays the said tax along with the interest payable under section 50 within thirty days of issue of show cause notice, no penalty shall be payable and all proceedings in respect of the said notice shall be deemed to be concluded.

S.74(8) – Where any person chargeable with tax under sub-section (1) pays the said tax along with interest payable under section 50 and a penalty equivalent to twenty-five per cent. of such tax within thirty days of issue of the notice, all proceedings in respect of the said notice shall be deemed to be concluded.

R.142(3) – Where the person chargeable with tax makes payment of tax and interest under sub-section (8) of section 73 or, as the case may be, tax, interest and penalty under sub-section (8) of section 74 within thirty days of the service of a notice under sub-rule (1), or ……., he shall intimate the proper officer of such payment in FORM GST DRC-03 and the proper officer shall issue an order in FORM GST DRC- 05 concluding the proceedings in respect of the said notice. Form DRC-05: Intimation of conclusion of proceedings.

Time limit Adjudication/Order:

73(10) – The proper officer shall issue the order under sub-section (9) within three years form the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilised relates to or within three years from the date of erroneous refund.

S.74(10) – The proper officer shall issue the order under sub-section (9) within a period of five years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilised relates to or within five years from the date of erroneous refund.

R.142(5) – A summary of the order issued under section 52 or section 62 or section 63 or section 64 or section 73 or section 74 or section 75 or section 76 or section 122 or section 123 or section 124 or section 125 or section 127 or section 129 or section 130 shall be uploaded electronically in FORM GST DRC-07, specifying therein the amount of tax, interest and penalty payable by the person chargeable with tax.

142(6) – The order referred to in sub-rule (5) shall be treated as the notice for recovery.

FORM GST DRC-07 : Summary of the Order.

Rectification of Order/Notice etc

- Rectification of errors apparent on the face of record.—

- any authority, who has passed or issued any decision or order or notice or certificate or any other document, may rectify

- any error which is apparent on the face of record in such decision or order or notice or certificate or any other document

- either on its own motion or where such error is brought to its notice by any officer or by the affected person

- within a period of three months from the date of issue of such decision or order or notice or certificate or any other document

- Provided, no such rectification shall be done after a period of six months from the date of issue of such decision or order or notice or certificate or any other document

- said period of six months shall not apply where the rectification is purely in the nature of correction of a clerical or arithmetical error, arising from any accidental slip or omission:

- For adverse rectification, principles of natural justice shall be followed by the authority carrying out such rectification.

- 142(7) – Where a rectification of the order has been passed in accordance with the provisions of section 161 or where an order uploaded on the system has been withdrawn, a summary of the rectification order or of the withdrawal order shall be uploaded electronically by the proper officer in FORM GST DRC-08.

- What if Tribunal/Court takes a view against Extended period SCN?

- 75(2).Where any Appellate Authority or Appellate Tribunal or court concludes that the notice issued under sub-section (1) of section 74 is not sustainable for the reason that the charges of fraud or any wilful-misstatement or suppression of facts to evade tax has not been established against the person to whom the notice was issued, the proper officer shall determine the tax payable by such person, deeming as if the notice were issued under sub-section (1) of section 73.

- Demand can be raised for normal period SCN within 2 years from receipt of such order

Summons – Legal Provision.

- The proper officer under this Act shall have power to summon any person whose attendance he considers necessary either to give evidence or to produce a document or any other thing in any inquiry in the same manner, as provided in the case of a civil court under the provisions of the Code of Civil Procedure, 1908.

- Every such inquiry referred to in sub-section (1) shall be deemed to be a “judicial proceedings” within the meaning of section 193 and section 228 of the Indian Penal

Who is Proper Officer?

Circular No. 3/3/2017-GST dated July 05, 2017, Superintendent of Central Team is the PO under sub-section (1) of Section 70 of the CGST Act.

NN 14/2017 Central Tax dated 01.07.2017 Senior Intelligence Officer, GST Intelligence or Superintendent, GST Audit.

Summons – CBIC Guidelines

Obligation of Person so summoned

- A person who is summoned, legally bound to attend either in person or by an authorized representative

- He is bound to state the truth on the subject matter of examination and to produce such documents and other things as may be required

Guidelines for issue of summons: [CBIC FAQ’s and F. No. 207/07/2014- CX-6 dated January 20, 2015]

- Summon is to be issued as a last resort where assesses are not co-operating;

- Language of the summons should not be harsh and legal which causes unnecessary mental stress and embarrassment to the receiver;

- Summons by Superintendents should be issued only after obtaining prior written permission from an officer not below the rank of Assistant Commissioner with the reasons for issuance of summons to be recorded in writing:

How to view GST Notices in the Portal and reply through online:

steps to reply to a scrutiny notice:

Step 1: Select the ‘Replies’ tab on the case details page to view all the replies filed with the tax department. To add a reply, click ‘Notice’.

Author Name: M.S. VIJAYAKUMAR

Qualification: M.COM. B. ED.M.B.A.M. PHIL.HDNC.,

OCCUPATION: ASSISTANT COMMISSIONER GST (RETD.)

Location: MADURAI TAMILNADU

Author can be reached in 9442022874; 8838052001;

mail4rvijay@gmail.com

Author Bio

there are legal remedies for you to avoid penalty whether they ed officer has issued orders then go for appeal sir there are lotof cases in favor of assessee

we have given gst department notice –

1) we have taken previous year ITC of current year .

so we have requested you will give me reply

sir you can take the input tax credit for the previous year input tax credit in the month itself, following the month and finally annual return to be filed on or before 30.11. 2024. you are eligible for the input tax credit if you have invoice, received the goods and make payment to the supplier and the supplier has paid the tax collected from you to the government by filing GSTR1 . so you can take itc. if any further clarification write to me

The Asst commissioner sent a notice through the portal and we have not replied within 30 days. after that officer call after two months and we we visited with the officer and comply properly. there is a small amount which is availed as ITC. now the officer sent a notice for penalty as we have not replied within 30 days. we have not received any notice by SMS or Email. please help me if the penalty is revocation.

sir whether you received any notice and get signed for receipt of notice. you give a written reply stating everything in detail to your officer. at the notice stage you can approach only the officer to explain and drop. if orders passed by the officer you can file an appeal before applellate deputy commissioner and legal remeady. approach any lawyer with notice and draft a reply then file an appeal

very thoughtfully written.

I have a case where SCN have same DIN for two different persons. For e.g . A and B have received SCN from service tax department with same 20 digit DIN number from the same deputy commissioner. Whether they are valid and what is the implication.

Sir,

Can you give me reference of Act/Rules in regard to CBEC clarification for issuance of Pre-Show Cause Notice u/s 73(5)/74(5) in DRC-01A, when demand exceeds Rs.50 lacs. Also give details of CBEC .clarification & your views on the legality of such instructions.

CA Om Prakash Jain s/o J.K.Jain, Jaipur Tel:9414300730

In the case o demand of duty is above 50 LathaLakhs With the consultation of commissioner prePreSCN should be issued

CBEC clarrified

Comprehensive , very useful !!

Sir,

Whether issuance of Pre-Show Cause Notice u/s 73(5)/74(5) in DRC-01A is a must prior to issuance of show cause notice u/s 73(1)/74(1) in Form DRC-01 since recently in the case of Agrometal Vendibles Private Limited v. State of Gujarat & Ors.(2022) 37 J.K.Jain’s GST & VR 523 (Guj), the High Court quashed notice served in DRC-01 instead of DRC-01A

CA Om Prakash Jain s/o J.K.Jain, Jaipur

Tel:9414300730

Check has clarified that in the case of duty exceeds 50lakhs pre SCN is must sir