1. INTRODUCTION

1. INTRODUCTION

There are certain type of forms which has been prescribed under central sales tax rules 1957, form C for making interstate purchase at lower rate, form F used to transfer goods from one branch to other in different state without making it as sale form E1 and E2 used when interstate sale or purchase which are effected by mere transfer of document of title (subsequent sale).

2. ANALYSIS

A) C FORM

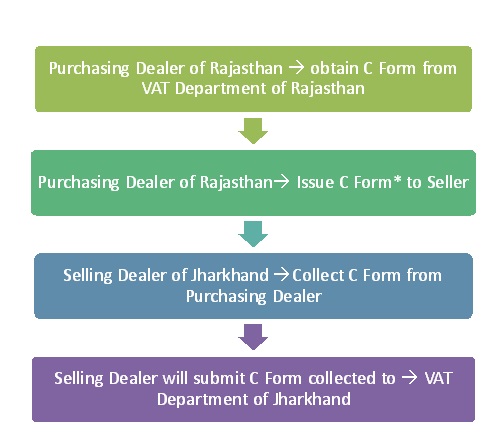

It is issued by VAT department to the registered dealer who makes interstate purchases of those goods which are mentioned in his RC (registration certificate). While doing transaction purchasing dealer furnish this form to selling dealer in course of interstate purchase to get exemption/reduction in sales tax rate. It is defined under section 8(1) of CST act 1956.

*One C Form/One Quarter/Dealer

From above chart it is clear that firstly purchasing dealer will furnish form C to the selling dealer of Jharkhand to claim tax exemption or reduced rates of taxes (2%) thereafter selling dealer will submit these form to the department of VAT of Jharkhand.

One C form can be used for no of transactions for one quarter.

B) F FORM

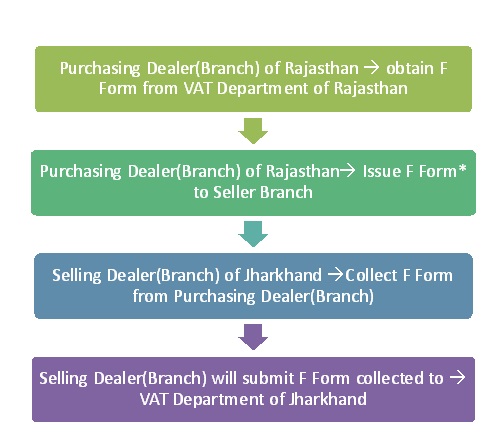

With this, goods can be transferred/delivered from one state to another without recognising it as a sale. For instance the head branch may transfer goods/stock from one state to another to its branch or agent without becoming liable for CST.

It is issued by the VAT department on the request of the purchasing dealer (branch) the purchasing dealer submits F form to the selling dealer to claim exemption from making it as CST sale. As per section 6(A) of CST act F from is mandatory to prove transaction as stock transfer. One F Form/One Month/Dealer

One F Form/One Month/Dealer

Is F form required in case goods are returned? The answer is yes, decided by the hon’ble Supreme court in case of AMBIKA STEELS that the liability of furnishing F form would be still there even if stock or goods are required to be sent back.

Registration certificate {RC} should contain the name and address of branches to which stock is transferred against F FORM {branch transfer} to claim concessional/nil rate of tax. One F form has to be issued for each month.

C) E1 AND E2 FORM

As per section 6(2) of CST act first interstate sale will be taxable, subsequent sale during movement of good by way of transfer of document is exempt from tax. For making subsequent sale exempt Form E1 & E2 are used.

- Ashok has to dispatch goods to Chandan Jaipur (Rajasthan) but Invoice done on Bhanu in Delhi

- A will receive C Form from Bhanu of Delhi and will issue declaration in E-I form to Bhanu

- Bhanu Sells Goods to C in Jaipur-Rajasthan

- Bhanu of Delhi will issue declaration in Form E-II to Chandan of Jaipur against which Chandan will furnish C form to Bhanu (Delhi).

- Chandan Ultimately receives the goods.

- Chandan will issue C Form to Bhanu and will receive E-II Form from him.

From above illustration it is clear that how goods/document of title move from one place to another. Actual delivery was received by C in Jaipur however between A, B there was only transfer of title. Only the first sale will be taxable, other subsequent sale will be exempt if dealers are registered.

In above example A of Mumbai will receive C form from B of Delhi & will issue declaration in E-I form to B of Delhi .Later on B of Delhi will issue declaration in Form E-II to C of Jaipur against which C will furnish C form to B (Delhi).

If above chain is broken then the exempt sale will get reversed and CST will be applied on these transaction.

Provisions of C form applicable to E1/E2 forms: Some provisions which are applicable to C forms are also applicable to E-I/E-II forms. For example one declaration for one quarter, indemnity bond if form is lost, issue of duplicate form, sales tax concession is not available if the forms are not submitted.

Latest case of Delhi High Court and Supreme court’s verdict in A&G Projects and Technologies Ltd case: The Supreme court in A & G Projects and Technologies Ltd v. State of Karnataka [2209] 19 VST 239; [2009] 2 SCC 326 explained the scheme of section 6(2) of CST Act and held that once the first inter-state sale has suffered CST then subsequent sales effected by transfer of documents during transit will be exempt provided conditions prescribed u/s 6(2) are satisfied. This has been done to remove the cascading effect. The observation of the Supreme Court in the said case is provided as below

“Analysing Section 6(2), it is clear that sub-section (2) has been introduced in Section 6 in order to avoid cascading effect of multiple taxation. A subsequent sale falling under sub-section (2), which satisfies the conditions mentioned in the proviso thereto, is exempt from tax as the first sale has been subjected to tax under sub-section (1) of Section 6 of the CST ACT 1956. Thus, in order to attract Section 6(2), it is essential that the concerned sale must be a subsequent inter-State sale affected by transfer of documents of title to the goods during the movement of the goods from one State to another and it must be preceded by a prior inter-State sale. It is only then that Section 6(2) may be attracted in order to make such subsequent sale exempt from levy of sales tax. However, the proviso to sub-section (2) of Section 6 prescribes further conditions and it is only on fulfilment of those conditions that the subsequent sale stands exempted. If those conditions are not satisfied then, notwithstanding the fact that the sale is a subsequent sale, the exemption would not be admissible to such subsequent sales. This is the scheme of Section 6 of the CST ACT 1956.”

In a recent case namely Mitsubishi Corp. Ind. Ltd. Vs Value Added Tax officer decided by Delhi High court wherein sighting the above observation of the Supreme court it was argued by the counsel for the state that if the first Inter State sales is an exempted sale then the subsequent sales should not get the benefit of Section 6(2) of CST Act even if all the conditions u/s 6(2) are satisfied since the first sales had not suffered tax. The Delhi High Court in this regard observed as under:

“A reading of the said portion of the Supreme Court decision only indicates that where the first sale is taxed, the second sale would be exempted because of the object of avoiding the cascading effect. However, the Supreme Court decision cannot be understood to mean that where the first sale is exempted, the second sale must be taxed even though the conditions under Section 6(2) for exemption stand satisfied.”

Thus even if the first sales was exempted due to exemption on tax available in the state where from the first sale is made the subsequent sales in other state will be exempted if the conditions u/s 6(2) of CST Act are satisfied.

can we clain C form if we are not register under CST

I Need a information regards

What is meant by Form H

What is meant by ER2 form

What is meant by Pre Eport sales

I like to know if we exort the good applicable tax form name(Example : For ER2)

I like to know if we Import the good applicable tax form name (Example Form H)

hello sir,

I have trading form.pl advise how to obtain c form for year 2009-10,

Respected Sir,

What we have to do. If we have not Submitted any Details to Generat Form No. F against Sales Return ?

We have taken adjusted such goods return in our Account.

but our Consultant had not inform us about it.

So let me inform us about it as early as possible.

What is vat(r) & vat(t)?

Sir, I have received the notice for submission of c/f from. I have submitted all forms as we have mentioned in 704.But while checking the declaration forms he asked for sales / purchase register and other details also. My question is that can he ask for all these things without MVAT assessment notice?

Sir, I have received the notice for submission of c/f from. I have submitted all forms as we have mentioned in 704.But while checking the declaration forms he asked for sales / purchase register and other details also. My question is that can he ask for all these things without MVAT assessment notice?

My company failed to provide C Form to our vendor and hence they charged us with the balance tax and interest @ 18% on it. Are we liable to deduct TDS on the interest paid to the vendor? if not, then why?

Ters a place called mahe wch is found in d geographical area of kerala..but mahe cums under puducherry… fr tem puducherry is a longer route…so if d dealer purchases or sells its goods from/to kerala dealer…tat wl b treated as cst purchase/ sales right…wthr do tey hv ny spcl provisions or benefits in tis regard

We are supplying our goods to Orrissa what is the c forms formate for collecting of C from

orrisa Commercial tax office at sombalpur

we have 2 branches in Maharashtra. supposed we are sending the material one location to another location i.e. Maharashtra state. is the applicable the F Form & what is procedure?

we have 2 firm same name , 1 st in chandiagrh, 2 nd in panchkula , we are sale c form in chandiagrh. , we stock trf into panchkula , after that we are sale agst c form to chandigarh same material to party. is it ok or not

form c procedure

our company have hotel business buying chemical in cst purchase it is elible for form c

thanks

Sir, i may need guidance from u.

I M HAVING BUSINESS IN GUJARAT, V R RECEIVING RAW MATERIAL FROM OUR BUYER OF KARNATAKA, RAW – MATERIAL DIRECT – RECEIVE FROM GUJARAT – N BILLD DIRECT TO KARNATAKA BUYER AGAINST FORM ‘C’ – V JUST PRODUCE COMPONENTS FORM MATERAIL N

FW TO KARNATAKA BUYER – ON JOB – WORK BASE. THIS IS JOB-WORK SO V MAY NOT CHARGE

ANY TAXES IN OUR JOB-WORK INVOICE.

NOW A DAY TAX OFFICER , DEMAND FORM ‘F’, IN CASE V MAY NOT SUBMEET FORM – THE

MAY NOTICE US TO PAY CST @5% FOR – RAW MATERIAL + JOB WORK BILL.

OUR BUYER IS NOT ABLE TO ISSUE FORM ‘F’ – BECAUSE THIS IS MATTER OF F.Y.2011-12 N HE IS NOT ABLE TO ISSUE OLD YEAR FORM.

ANY HOW WHAT TO DO?

EXPECT YOUR PROMPT GUIDANCE.

THANKS

Dear Sir,

I am registered Dealer in Karnataka under CST. I am purchasing goods from Tax Exempted area from Silvassa under C Form & selling it in Maharashtra under C-E 1 Form. During assessment of FY 2012/13 I have not received C Form from Sales Tax Department Karnataka but Authority is asking for E 1 Form. I am unable to get E 1 Form unless I am submitting C Forms received from Karnataka. Please give me evidence that Sales Tax Department have to release C form first then I will Submit E 1 Forms.

Thanks.

Form f received with omission of transfer details in maharastra state.what are the procedures to include the omission transfer in that form.

Sir,

I’m a manufacturer at Chattisgarh. I sold goods to the dealer at Odissa. The sales invoice raised and goods sent in the month of January-2015. In the month of May, I came to know that the materials was not accepted by the customer for quality problem and it was then under analysis at their end. In June, they accepted the materials and shown in their books as purchase and sold to their customer at Jharkhand.

On hearing, I also reversed sale in the year 2014-15 and recognised the same in 2015-16 1st quarter. Accordingly, I submitted sales tax revised return of 2014-15 (4th Qr.) and shown the sales in the 1st. Qr. of 2015-16.

Recently the my customer issued me the Form-C with a request to issue E1 for the 1st. Qr. 2015-16.

While filing application on-line for E1 (Chattisgarh), it denied to accept the application for the year 2015-16 as because the date of Invoice Jan-15. On enquiry at the department, it is learnt that the E1 could not be issued for 2015-16 due to the date of invoice. And there is no provision in the state sales tax rule for manual issue of E1.

My question is that although the matter is genuine and every compliance is there, why should I be deprived of the E1 and liable for consequences.

Regards

Asis Protihar

Sir,

Ours is a SSI manufacturing unit in Punjab. We sold some goods against Form I to the customer in Andhra Pradesh in March 2014. Now after one year, the customer has informed us that they cannot issue Form I to us. The customer has instead sent us the C Form i.e. @ 2% CST.

Can we now change the Sales from I form to C form? Can we file Revised CST Return for the period after changing the sales from I form to C form?

Our sales tax officer is refusing to accept C Form with 2% CST plus interest for the delay.

Sales tax officer is insisting to pay full VAT tax on the sales, with interest and penalty or I form only.The reason cited by him is that once annual return has been file no revision can be made what so ever, as per CST (Punjab rules).

Can the sales tax officer refuse to accept C Form, when it is a genuine Inter-state sales with lorry receipt details etc.

Please advice. Thanks.

Sir

we are a registered delaer in delhi. we purchase machine from intersate delear but we miss that to shiwing in purchase. now party asking for C F ORM. AND WE HAVE DONE audit. is there any way to settle this

please help us

contact no 9717622787

name – mohd rashid

Sir,

A,B And C , we are C , we issued c form to b , how to issue form ( taxable ( Basic + ed )+ tax ( cst ) is right

I AM DELHI IMPORTER MY GOODS ARRIVED TO MUMBAI AND I SELL MY WHOLE GOODS TO PUNE FROM TRUCK SO WHICH FORM WE RECIVED FROM PARTY

dear sir,

i am a importer,

i have sales my stock mvat to goa vat under f form sales to party, goa party not paid any tax in goa how can i claimed SAD REFUND.

I have a query that in case of vat exempted on goods in a state,sells the goods to other state can impose CST on the said goods and require C form.

i am a manufacturer at west bengal and i have purchased a heavy duty vehicle from volvo india , bangalore at cst 2% through a dealer from kolkata at a price of rs 30 lakh. the dealer from kolkata have issued me the invoice without charging 2% cst and waybill part 2 has been issued to me by volvo india, bangalore for an amount of rs 2610333.

so my doubt is that on whose name i should provide c form and at what value. and i also have a doubt that whether the dealer from kolkata would provide me with e1 form or not.

i Can Issue C form With Invoice Value (Basic+Excise+cst+freight+other)

Pl Clear The Issue

After take out the information about C,E & F-form , I am very glad n Want to give bigger thanks , so Accept my thanks and would provide like these information in this site whose are useful to us.

A dealer of Odisha send damaged tyres received from buyers within the warranty period to its principal outside Odisha. In this case declaration in form ‘F’ is mandatory or not ?

Sir,

I am registered in delhi sales tax in automobiles, and machinery items i can sale tax free goods ( shoes use for labour)

Do we need to issue f-form against interstate stock transfer of tax free goods like poultry / cattle feed supplements ?

regards

in c form , what value should be issued, give me detail about valuation,

Sir,

If I am supplier. I am selling goods to party at Tamilnadu. The party is sending me monthly C Forms. Can I accept all 12 C Forms or only quarterly C Forms are acceptable? That means all 12 C forms will be valid or only 4 will be valid and remaining 8 forms will be rejected? If yes then why? If no then please give me proper reference about that. Kindly reply urgently.

sir i am cotton business iam selling f.p.cotton bales to export co ,(galiyakotawal )but he was not giving h form what can i do

SIR

I AM FROM DELHI.

IF I PURCHASE GOODS FROM CHANDIGARH AGAINST C FROM

WHAT IS THE RATE OF TAX HE WILL CHARGE FROM ME?

PLEASE EXPLAIN

FORM H

If in E2 sale the seller and purchaser are from same state. Then shall we issue Form-C to the seller. But the E1 sale is of different states are Form-C is issued in E1 sale. Pls,reply me….

I am registered dealer in maharashtra. I want to purchase good from chattisgarh and sell it in chattisgarh. What will be sales tax liability and form reqd?

Hi,

I am shoes supplier from agra,recently i shiped shoes to some in pune but he rejected the shipment i asked for return but he said transporter is asking for form c.please guide me hiw he can shipback product to me.

plz explaine E1/E2 CHAIN

Can I issue the E1 forms to the customer on quarterly basis like how we issue the FORM-C to our vendors, please clarify urgently

f form is for all state

sir im going to open n enterprises which will supply the spare parts to the plant n locomotive parts to various plants n arailway allso across india

so wht kind of registration do i required to get a TIN NO and to get a pvt.ltd tag

allso tell me what other registration is needed n wht abt form c n all

Why the provision of Form C.

Sir

Why the provision of “Form C”.

purchaser issued c-form as per the goods receipt date not as per invoice date.provide solution

Sir,

In yr example for 6(2) sales, C will issue C form to B, but there is no need for B to issue any EII form, as the sale ends with C. C being the ultimate customer, as per yr illustration has no obligation to collect an EII form. Pl re-chk the provisions.

Nice article, good work

Nice article good work…

Good work! keep it up!