1. INTRODUCTION

1. INTRODUCTION

There are certain type of forms which has been prescribed under central sales tax rules 1957, form C for making interstate purchase at lower rate, form F used to transfer goods from one branch to other in different state without making it as sale form E1 and E2 used when interstate sale or purchase which are effected by mere transfer of document of title (subsequent sale).

2. ANALYSIS

A) C FORM

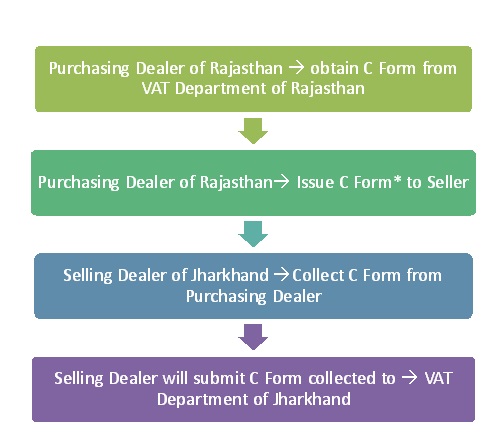

It is issued by VAT department to the registered dealer who makes interstate purchases of those goods which are mentioned in his RC (registration certificate). While doing transaction purchasing dealer furnish this form to selling dealer in course of interstate purchase to get exemption/reduction in sales tax rate. It is defined under section 8(1) of CST act 1956.

*One C Form/One Quarter/Dealer

From above chart it is clear that firstly purchasing dealer will furnish form C to the selling dealer of Jharkhand to claim tax exemption or reduced rates of taxes (2%) thereafter selling dealer will submit these form to the department of VAT of Jharkhand.

One C form can be used for no of transactions for one quarter.

B) F FORM

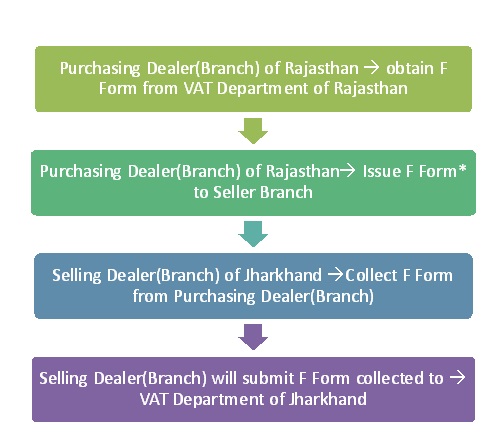

With this, goods can be transferred/delivered from one state to another without recognising it as a sale. For instance the head branch may transfer goods/stock from one state to another to its branch or agent without becoming liable for CST.

It is issued by the VAT department on the request of the purchasing dealer (branch) the purchasing dealer submits F form to the selling dealer to claim exemption from making it as CST sale. As per section 6(A) of CST act F from is mandatory to prove transaction as stock transfer. One F Form/One Month/Dealer

One F Form/One Month/Dealer

Is F form required in case goods are returned? The answer is yes, decided by the hon’ble Supreme court in case of AMBIKA STEELS that the liability of furnishing F form would be still there even if stock or goods are required to be sent back.

Registration certificate {RC} should contain the name and address of branches to which stock is transferred against F FORM {branch transfer} to claim concessional/nil rate of tax. One F form has to be issued for each month.

C) E1 AND E2 FORM

As per section 6(2) of CST act first interstate sale will be taxable, subsequent sale during movement of good by way of transfer of document is exempt from tax. For making subsequent sale exempt Form E1 & E2 are used.

- Ashok has to dispatch goods to Chandan Jaipur (Rajasthan) but Invoice done on Bhanu in Delhi

- A will receive C Form from Bhanu of Delhi and will issue declaration in E-I form to Bhanu

- Bhanu Sells Goods to C in Jaipur-Rajasthan

- Bhanu of Delhi will issue declaration in Form E-II to Chandan of Jaipur against which Chandan will furnish C form to Bhanu (Delhi).

- Chandan Ultimately receives the goods.

- Chandan will issue C Form to Bhanu and will receive E-II Form from him.

From above illustration it is clear that how goods/document of title move from one place to another. Actual delivery was received by C in Jaipur however between A, B there was only transfer of title. Only the first sale will be taxable, other subsequent sale will be exempt if dealers are registered.

In above example A of Mumbai will receive C form from B of Delhi & will issue declaration in E-I form to B of Delhi .Later on B of Delhi will issue declaration in Form E-II to C of Jaipur against which C will furnish C form to B (Delhi).

If above chain is broken then the exempt sale will get reversed and CST will be applied on these transaction.

Provisions of C form applicable to E1/E2 forms: Some provisions which are applicable to C forms are also applicable to E-I/E-II forms. For example one declaration for one quarter, indemnity bond if form is lost, issue of duplicate form, sales tax concession is not available if the forms are not submitted.

Latest case of Delhi High Court and Supreme court’s verdict in A&G Projects and Technologies Ltd case: The Supreme court in A & G Projects and Technologies Ltd v. State of Karnataka [2209] 19 VST 239; [2009] 2 SCC 326 explained the scheme of section 6(2) of CST Act and held that once the first inter-state sale has suffered CST then subsequent sales effected by transfer of documents during transit will be exempt provided conditions prescribed u/s 6(2) are satisfied. This has been done to remove the cascading effect. The observation of the Supreme Court in the said case is provided as below

“Analysing Section 6(2), it is clear that sub-section (2) has been introduced in Section 6 in order to avoid cascading effect of multiple taxation. A subsequent sale falling under sub-section (2), which satisfies the conditions mentioned in the proviso thereto, is exempt from tax as the first sale has been subjected to tax under sub-section (1) of Section 6 of the CST ACT 1956. Thus, in order to attract Section 6(2), it is essential that the concerned sale must be a subsequent inter-State sale affected by transfer of documents of title to the goods during the movement of the goods from one State to another and it must be preceded by a prior inter-State sale. It is only then that Section 6(2) may be attracted in order to make such subsequent sale exempt from levy of sales tax. However, the proviso to sub-section (2) of Section 6 prescribes further conditions and it is only on fulfilment of those conditions that the subsequent sale stands exempted. If those conditions are not satisfied then, notwithstanding the fact that the sale is a subsequent sale, the exemption would not be admissible to such subsequent sales. This is the scheme of Section 6 of the CST ACT 1956.”

In a recent case namely Mitsubishi Corp. Ind. Ltd. Vs Value Added Tax officer decided by Delhi High court wherein sighting the above observation of the Supreme court it was argued by the counsel for the state that if the first Inter State sales is an exempted sale then the subsequent sales should not get the benefit of Section 6(2) of CST Act even if all the conditions u/s 6(2) are satisfied since the first sales had not suffered tax. The Delhi High Court in this regard observed as under:

“A reading of the said portion of the Supreme Court decision only indicates that where the first sale is taxed, the second sale would be exempted because of the object of avoiding the cascading effect. However, the Supreme Court decision cannot be understood to mean that where the first sale is exempted, the second sale must be taxed even though the conditions under Section 6(2) for exemption stand satisfied.”

Thus even if the first sales was exempted due to exemption on tax available in the state where from the first sale is made the subsequent sales in other state will be exempted if the conditions u/s 6(2) of CST Act are satisfied.

Our Customer is SEZ unit issued I Form 2014-15 on yearly basis now department is not accepting yearly form they are allowing only quarterly sales value amount is there any provision for quarterly form in rule 12 of CST act not mentioned properly.