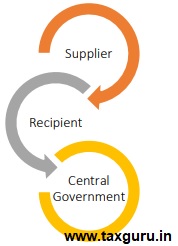

In the GST regime, An Entity or Supplier is required to be registered either mandatorily under cretin circumstances (say, crossing threshold limit – 40L/20L; involved in specified business’s) or on voluntary basis.

However there are certain suppliers,not registered due to illiteracy (say, local good transporters) or they are situated in non-taxable territories (say, supplier in Foreign Country’s); etc…, hence Govt. identified such similar transactions & introduced this method of taxi on i.e.,Reverse Charge Mechanism (to curb the tax evasion)– a concept of collecting the tax directly from the Recipient in stead of Supplier.

Here, confusion arises to everyone about applicability of this provision & if it’s applicable, what is the procedure to be followed like when and how much is payable & etc..,

This article, will clarifies such basis confusions which one has, let’s start with basic question i.e., What is RCM?

What is RCM?

It is a Reverse Charge Mechanism means ‘liability to pay tax by the recipient of supply of goods or services or both instead of the suppliers of such goods or services or both’ under Sec.9 of sub-section (3) or (4) of IGST Act or under Sec.5 of sub-section (3) or (4) of IGST Act.

Let’s see an Example – How it works?

M/s. XYZ & Co, a Security Services Co provided security services to M/s. Abhinav & Associates, a partnership firm & charged of Rs.118/- (TA-100 + GST-18) therefore, Abhinav associates requires to pay whole amount of Rs.118/- to supplier, right?

But under RCM provisions, Abhinav Associates supposed to pay only the taxable amount i.e., Rs.100/- to supplier by withholding the GST part in that and later Abhinav Associates required to pay this GST of Rs.18/- to the Government.

As the Abhinav Associates (i.e., Recipient) pays tax to the Govt. instead of Supplier this transaction will be treated as RCM.

And Abhinav Associates will be liable to pay through Electronic Cash Ledger (means in Cash mode) & can’t use his Electronic Credit Ledger balance (means ITC available on their account can’t be used) further, tax paid by them under RCM can be considered as Input tax credit as per the provision of ITC.

Now, let’s understand to Whom it’s applicable?

Applicability will be purely depending on the transactions with whom we entered & kind of services or goods we are obtaining from them.

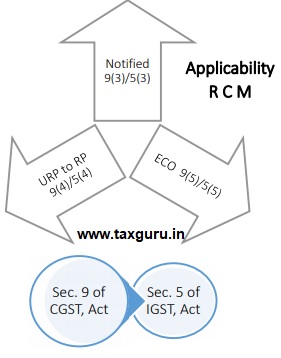

Under GST Act, 2017 – applicability was bifurcated into 3 categories –

1. On notified category of Goods or Services (Sec.9(3)/Sec.5(3))

2. Supply of goods or services from Unregistered to Registered (Sec.9(4)/Sec.5(4))

3. E-Commerce Operator (ECO) (Sec.9(5)/Sec.5(5))

Sec. 9(3)/5 (3) – Notified Services/Goods –

Notified Goods –

| Description of Supply – | Supplier of Goods | Recipient of Supply (Liability) |

| 1. Cashew nuts | Agriculturist | Any registered person |

| 2. Bidi Wrapper Leaves | ||

| 3. Tobacco Leaves | ||

| 4. Silk Yarn | Manufactures silk yam from raw silk or

Silkworm cocoons for supply of silk yarn |

|

| 5. Raw Cotton | Agriculturist | |

| 6. Lottery | State Government / Union Territory / Local Authority | Lottery distributor or selling agent |

| 7. Used vehicles, seized & confiscated goods, old & used goods, waste & scrap | Central Government / State Government / Union Territory / Local Authority | Any registered person |

| 8. Priority Sector Lending Certificate | Any registered person |

Notified Services –

| Services – By Whom | To Whom | Who’s Liable? |

| Goods Transport Agency – (Who has not paid central tax at the rate of 6% (CGST – 6% & SGST – 6%) |

Registered Person(RP) | Recipient who pays the freight is liable to GST. |

| Un-Registered Person(URP) | Notified person* is liable (located in Taxable Territory)

* Any Factory or Society or Co-operative society or Registered person or Body Corporate or Partnership Firm or AOP |

|

| Legal Services – directly or indirectly –

a. Individual advocate including senior advocate b. Firm of advocates |

Any Business Entity located in taxable territory (TT) | |

| Arbitral Tribunal – Private tribunal | ||

| Central Govt. (CG) / State Govt. (SG) / Union Territory (UT) / Local Authority (LA) | ||

| Renting of Immovable Property – CG / SG / UT / LA | Registered Person –(TT) | |

| Transfer of development rights or Floor Space Index/ Long-term lease of land (30 Years or more) – construction of a project – Any Person | Promoter | |

| Insurance Agent | Any person carrying any insurance business – (TT) | |

| Recovery Agent | A Banking Company, A Financial Institution, Non-Banking Financial Institution (NBFC) – (TT) | |

| Individual Direct Selling Agent’s(DSA’s) | ||

| Members of Overseeing Committee | Reserve Bank of India (RBI) | |

| Business Facilitator | A Banking Company – (TT) | |

| An Agent of Business Correspondent (BC) | A Business Correspondent – (TT) | |

| An Author – permitting the use or enjoyment of a copyright | A Publisher – (TT) | |

| Music Composer / Photographer / Artist – permitting the use or enjoyment of a copyright | A Publisher, Music Comp, Producer, or the like – (TT) | |

| Security Service – Any Personother than a body corporate | A Registered Person – (TT) | |

| Director of a Company or Body Corporate | Company or Body Corporate | |

| Sponsorship Services – Any Person | Any Body Corporate or Partnership Firm – (TT) | |

| Newly inserted by N/N 22/ 2019 CT – (R) dt 30-09-2019 | ||

| 1. Service of Lending Securities under Securities Lending Scheme, 1997 of SEBI – Lender

(i.e., a person who deposits the securities registered in his name or in the name of any other person duly authorised on his behalf with an approved intermediary for the purpose of lending under the scheme of SEBI) |

Borrower (i.e., a person who borrows the securities) | |

| 2. Renting of a motor vehicle – Any person other than Body Corporate (Paying CGST & SGST @ 2.5% on renting of Motor Vehicles with input tax credit only of input service in the same line of business) | Any Body Corporate located in the TT | |

In addition to the above-mentioned services, these two additional services are specified for purpose of IGST, under IGST Act, 2017 –

| By Whom | To Whom | Who’s Liable? |

| General Services – | ||

| Any Person in Non-Taxable Territory (NTT) | Any Person (TT) other than Non-Taxable Ordinarily Resident (NTOR)

(NTOR – Government / Local Authority / Governmental Authority / Individual (TT) / any URP receiving OIDAR services for non-commercial or non-business use) |

|

| Transportation of Goods by Vessels – | ||

| Any Person in Non-Taxable Territory (NTT) | Importer (as defined in clause (26) of Sec.2 of the Customs Act, 1962 located in the taxable territory) | |

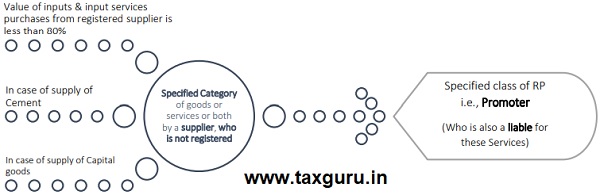

Sec. 9 (4) / 5 (4) – Supply of Services / Goods by URP to RP –

Note’s –

Say promoter has purchased goods (including CEMENT)or consumed services from RP (Rs.1,180/-) & URP (Rs.1,180/-)together of Rs.2,360/-

In the above example, we can notice that the total value of inputs from registered supplier is less than 80% (i.e., 50 %) therefore according to this provision, promoter is required to pay the balance of 30% of GST(i.e., to extent of 80%) under RCMat the rate of 18%.

If promoter has purchased the Cement from URP – he is liable to pay RCM @ 28 %

In case of Capital goods – liable at the applicable rate.

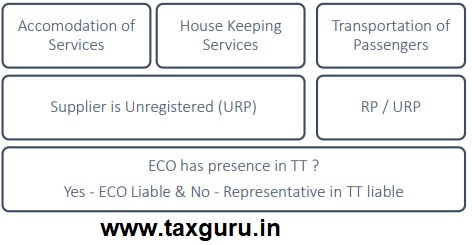

Sec. 9 (5) & 5 (5)-E-Commerce Operator

Notified Category of Services –

If supplier is registered in the first two Services, then ECO will be not liable, whereas in case of 3rd Service i.e., transportation of passengers irrespective of supplier registration – ECO is liable.

Proviso – Provided that where an ECO does not have a physical presence in TT, representative of such ECO in TT shall be liable to pay tax.

Provided further that where an ECO doesn’t have a physical presence in the TT and also, he doesn’t have representative in the said territory – Such ECO shall appoint a person in TT for the purpose of paying tax.

So, till here we understood What is RCM? & for which transactions it’s applicable?

Now, lets see Who is liable to register andWhen it is taxed –

In the above Notified transactions, we can notice that recipient might be Registered or Any person, in this scenario there wouldn’t be any problem for registered person’s( w.r.to paying the RCM liability and claiming that as Input – like Abhinav & Associates) but in case of Unregistered person they can’t pay the liability to the Govt.

Hence therefore All Unregistered Persons(i.e., Recipients) who involved in the above listed transactions, required to get registered MANDATORLY irrespective of threshold limit as applicable.

If a person only supplies goods and services on which GST is paid on reverse charge basis then such person is not required to take registration even if the turnover exceeds the specified limits. Say, farmer is not engaged in trading of other taxable goods then he is not liable to take registration under GST.

When it is taxable& at what Rate?

| When it is Taxable? | ||

| In case of Goods | In case of Services | |

| Date of receipt of goods | Earliest Date | Date of payment |

| Date immediately after 30 days from the date of issue of an invoice by the supplier | Date immediately after 60 days from the date of issue of invoice by the supplier | |

| Date of Entry in the books of account of the recipient (in case of difficulty to determine the above) | Date of Entry in the books of account of the recipient (in case of difficulty to determine the above) | |

At what Rate?

Irrespective of type of registration obtained by recipient(as a Normal Taxable Person / Composition Dealer),will be taxable at rate applicable on such goods or services(i.e., @ 5%, 12%, 18% & 28%) not at the concessional rate (i.e., @ 1% / 5%) available to composition dealers.

If the goods/services supplied are exempted or nil rated, then no tax is payable under RCM.

Additional Points to be Noted –

1. Only the person registered as Normal Taxable Person will be eligible to take Input Tax Credit.

(Say, for Ex – Composition dealers / Input Service Distributors – who paid RCM will be not eligible to take ITC, as they are not registered as a Normal Taxable Person)

2. If RCM paid on the services which are not utilised for business purpose, then recipient can’tavail ITC on such RCM payment.

(Say, for Ex – Abhinav Associates availed the Security services for there personal purpose not for business purpose)

3. Self-Invoicing is to be done when anyone has purchased goods or services from an unregistered supplier that fall under the ambit of reverse charge. However there is no specific format as such but the following details are mandatory to be mentioned (Invoice Date, Vendor Name, Description of Goods & Services & Total Amount) And also further Invoice must mention that this invoice includes payment of tax under RCM.

Author is a tax consultant, Bangalore & can be reached to author at abhinav_prasad2@outlook.com

Author Bio

Sir, even if a firm takes service of cranes etc., will it have to pay reverse charge? FROM UNREGISTERED DEALER

Excellent Article !!!

Kindly could you explain

“Renting of a motor vehicle – Any person other than Body Corporate (Paying CGST & SGST @ 2.5% on renting of Motor Vehicles with input tax credit only of input service in the same line of business)”

Not very clear on this !!!

Thanks and Regards

Excellent presentation, keep it up!!