Here I tried to discuss about all the GST Returns, New (ANX-1/2/3) etc as well as existing GSTR-1/3B/4/5/6/7/8/9/9A/9B/9C/10 etc.

Existing Return Regime:

Section 37 : Furnishing Details of Outward Supplies

Section 38 : Furnishing Details of Inward Supplies-GSTR-2 (Suspended)

Section 39 : Furnishing of Returns(GSTR-3B,4,5,6,7,8)

Section 44 : Annual Return(GSTR-9)

Section 45 : Final Return(GSTR-10)

The new Returns will also be Discussed which are applicable from 1st oct 2020

SECTION 37 : FURNISHING DETAILS OF OUTWARD SUPPLIES

Who is required to Furnish the details of Outward Supplies:

ii) Due date of Submitting:

– For Taxable person having T/O up to 1.5 CR – last date of next month(Quarterly)

– For Taxable person having T/O More then 1.5 CR – 11th of the next month(Monthly)

However Due to COVID-19 No penalty will be there for the month of March, April, May have been increased to 30.06.2020. Quarterly Tax Payer (Jan to Mar 2020) can also submit their return up to 30.06.2020.

This is a Waiver of Late fees, if you don’t file your return up to 30.06.2020, Late fees shall be levied from the due date. (Eg: For April, Late fees will be counted from 12 may)

SECTION 37 : FURNISHING DETAILS OF OUTWARD SUPPLIES

iii) Contents of GSTR-1

A) Basic details:

– GSTIN, Legal name, Aggregate T/O, Tax period, HSN wise Summary, Details of Docs issued, Adv Received or Adjusted

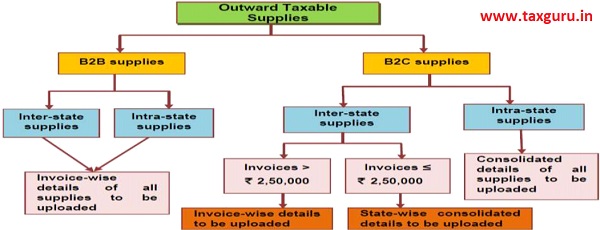

B) Details of Outward Supplies:

– B2B,B2C,Zero rated and Deemed Export, Debit/Credit Notes,Nil rated/ Exempted/ Non GST, Amendments to prior period

SECTION 37 : FURNISHING DETAILS OF OUTWARD SUPPLIES

iv) Time limit for correction of Errors, Amendments :

– Correction or Amendments of prior period can be done in subsequent Returns.

– Time Limit is as follows :

a) Date of filing GSTR-3B For the month of September of the following year

b) Date of filing Annual Return

v) Other Important Points :

– If there is no Business,GSTR-1 has to filed as NIL

– Late fees for GSTR-1 is Rs.50 per day or Rs. 20 per day(nil)

– However As per act late fees is Rs.200 or Rs. 100 per day

SECTION 39 : FURNISHING OF RETURNS (A) GSTR-3B

Who is required to Furnish GSTR-3B:

Due to COVID-1 9 time limit has been Revised as follows:

SECTION 39 : FURNISHING OF RETURNS

iii) Contents of GSTR-3B

A) Basic details:

– GSTIN, Legal name, Tax period

B) Details of Outward Supplies:

– Summarized Details of o/w and i/w Supplies liable for RCM

– Summarized Details of Inter state supplies made to URP, Composition tax payer, UIN holder

– Eligible ITC

– Value of exempt, nil rate, non gst inward supplies

– payment of tax

SECTION 39 : FURNISHING OF RETURNS

(B) GSTR-4/CMP-08

- GSTR-4 is a GST Return that has to be filed by a composition dealer. Unlike a normal taxpayer who needs to furnish 3 monthly returns, a dealer opting for the composition scheme is required to furnish only 1 return which is GSTR 4 once in a year by 30th of April, following a financial year.

- The due date for filing GSTR 4 is 30th of April following the relevant financial year. For example, the GSTR-4 for FY 2019-20 is due by 30th April 2020*. Due to COVID-19 extended date is 15.07.2020 for the FY 2019-20

- A late fee of Rs. 200 per day is levied if the GSTR-4 is not filed within the due date. The maximum late fee that can be charged cannot exceed Rs. 5,000.

- A taxpayer who has opted for the composition scheme has to file CMP-08 in order to deposit payments every quarter.

- Form CMP-08 must be filed on a quarterly basis, on or before the 18th of the month succeeding the quarter of any specific fiscal year. Due to COVID-19 Extended date for the Quarter Jan to Mar 2020 is 07.07.2020

- Normal Taxpayers wanting to opt for Composition should not file GSTR3B and GSTR 1 for any tax period of FY 2020-21 from any of the GSTIN on the associated PAN.

| Form | Tax period(FY) | Extended date |

| GST CMP-02(opt for comp.) | 2020-21 | 30.06.2020 |

| GST ITC-03(Normal to composition scheme etc.) | 2019-20(As on 31.03.2020) | 31.07.2020 |

SECTION 39 : FURNISHING OF RETURNS

(C) GSTR-5 Return of NRTP

- Non-Resident foreign taxpayers are those suppliers who do not have a business establishment in India and have come for a short period to make supplies in India. Such a person is required to furnish details of all taxable supplies in GSTR-5

- As per the GST Act, due date to file GSTR-5 is every 20th of next month. For instance, the return of September 2018 will be due on 20th October 2018.Due to COVID-19,Due date for the month of March, April, May 2020 has been extended to 30.06.2020.

- If you delay in filing, you will be liable to pay interest and a late fee. Interest is 18% per annum. It has to be calculated by the taxpayer on the amount of outstanding tax to be paid. The time period will be from the next day of filing (21st of the month) to the date of payment. A late fee is Rs. 50 per day and Rs. 20 per day if a nil return. The maximum late fees is Rs. 5,000.

SECTION 39 : FURNISHING OF RETURNS

(D) GSTR-6 Return of ISD

- GSTR 6 is a monthly return that has to be filed by an Input Service Distributor. It contains details of ITC received by an Input Service Distributor and distribution of ITC. There are a total of 11 sections in this return.

- The due date for filing of GSTR 6 as per GST Act is 13th of next month. Due to COVID-19,Due date for the month of March, April, May 2020 has been extended to 30.06.2020. Late fees have been reduced to Rs. 50 per day. However, no provision for reduction is made where NIL return is filed.

- GSTR 6A is an automatically generated form based on the details provided by the suppliers of an Input Service Distributor in their GSTR 1.GSTR-6A is a read-only form. Any changes to be made in GSTR-6A have to be done while filing GSTR-6.

SECTION 39 : FURNISHING OF RETURNS

(E) GSTR-7 Return for authorities deducting tax at source.

- GSTR 7 is a return to be filed by the persons who is required to deduct TDS (Tax deducted at source) under GST. GSTR 7 contains the details of TDS deducted, TDS liability payable and paid, TDS refund claimed if any etc.

- GSTR 7 shows the details of TDS deducted, amount of TDS paid and payable, any refund of TDS claimed. The deductee i.e. the person whose TDS has been deducted can claim the input credit of such TDS deducted and utilize for the payment of output tax liability. The details of TDS deducted is available electronically to each of the deductees in PART ‘C’of Form GSTR 2A after the due date of filing of Form GSTR 7. Also the certificate for such TDS deducted shall be made available to the deductee in Form GSTR 7A on the basis of return filed in GSTR 7.

- Filing of GSTR 7 for a month is due on 10th of the following month. For instance, due date of filing GSTR 7 for October is 10th November. Due to COVID-19,Due date for the month of March, April, May 2020 has been extended to 30.06.2020.

- If the GST return is not filed on time, then penalty of Rs 100 under CGST & Rs 100 under SGST shall be levied. The total will be Rs. 200/day. The maximum is Rs. 5,000 There is no late fee on IGST in case of delayed filing. Along with late fee, interest has to be paid at 18% per annum. It has to be calculated by the taxpayer on the tax to be paid. The time period will be from the next day of due date of filing to the date of payment.

SECTION 39 : FURNISHING OF RETURNS

(F) GSTR-8 Details of supplies effected through e-commerce operator and the amount of tax collected.

- GSTR-8 is a return to be filed by the e-commerce operators who are required to deduct TCS (Tax collected at source) under GST. GSTR-8 contains the details of supplies effected through e-commerce platform and amount of TCS collected on such supplies.

- Every e-commerce operator registered under GST is required to file GSTR-8. E-commerce operator has been defined under GST Act as any person who owns or manages a digital or electronic facility or platform for electronic commerce such as Amazon etc. All such ecommerce operators are mandatory required to obtain GST registration as well as registered for TCS (Tax collection at source).

- GSTR-8 filing for a month is due on 10th of the following month. For instance, the due date for GSTR-8 for October is on the 10th of November. Due to COVID-19,Due date for the month of March, April, May 2020 has been extended to 30.06.2020.

- If the GST return is not filed on time, then a penalty of Rs 100 under CGST & Rs 100 under SGST shall be levied per day. The total will be Rs. 200/day. The maximum is Rs. 5,000. There is no late fee on IGST in case of delayed filing. Along with late fee, interest at 18% per annum has to be paid. It has to be calculated by the taxpayer on the tax to be paid. The time period will be from the next day of filing to the date of payment.

SECTION 44 : Annual Return

GSTR-9T

- All taxpayers/taxable persons registered under GST must file their GSTR 9. However, the following are NOT required to file GSTR 9:Taxpayers opting composition scheme (They must file GSTR-9A)Casual Taxable Person, Input service distributors, Non-resident taxable persons ,Persons paying TDS under section 51 of CGST Act. GSTR-9C is a reconciliation statement between GSTR-9 and the audited books of accounts.

- GSTR 9 is an annual return to be filed yearly by taxpayers registered under GST. Points to note: It consists of details regarding the outward and inward supplies made/received during the relevant previous year under different tax heads i.e. CGST, SGST & IGST and HSN codes. It is a consolidation of all the monthly/quarterly returns (GSTR-1, GSTR-2A, GSTR-3B) filed in that year. Though complex, this return helps in extensive reconciliation of data for 100% transparent disclosures.

- GSTR-9 filing for businesses with turnover up to Rs 2 crore made optional for FY 17-18 and FY 18-19.

- The due date to file GSTR-9(FY 2019-20) is further extended to June 30, 2020. The late fees for not filing the GSTR 9 within the due date is Rs 100 per day, per act. That means late fees of Rs 100 under CGST and Rs 100 under SGST will be applicable in case of delay. Thus, the total liability is Rs 200 per day of default. This is subject to a maximum of 0.25% of the taxpayer’s turnover in the relevant state or union territory. However, there is no late fee on IGST yet.

- GSTR-9 is divided into 6 parts and 19 sections. Each part asks for details that are easily available from your previously filed returns and books of accounts. Broadly, this form asks for disclosure of annual sales, bifurcating it between the cases that are subject to tax and not subject to tax. On the purchase side, the annual value of inward supplies and ITC availed thereon is to be revealed. Furthermore, these purchases have to be classified as inputs, input services, and capital goods. Details of ITC that needs to be reversed due to ineligibility is to be entered.

- E commerce operators have to file GSTR-9B.Composition tax payers have to file GSTR-9A.

SECTION 45 : Final Return

GSTR-10

- A taxable person whose GST registration is cancelled or surrendered has to file a return in the form of GSTR-10. This return is called as final return.

- GSTR 10 must be filed within three months from the date of cancellation or date of cancellation order whichever is later. For instance if the date of cancellation is 1st September, 2017, then the GSTR 10 must be filed by 30th November, 2017.

- GSTR 10 is required to be filed only by the persons whose registration under GST has been cancelled or surrendered. The regular persons registered under GST are not required to file this return.

- If the GSTR 10 is not filed within the due date, a notice will be sent to the such registered person. The person will be given 15 days time for filing the return with all the documents required. If the person still fails to file the return, the tax officer will pass the final order for the cancellation with the amount of tax payable along with interest/penalty. Penalty can be up to Rs. 10,000

Some Important Aspects

> Form-PMT-09 is now live on GST Portal from 21.04.2020. In this form a tax payer can transfer any amount of tax, interest, penalty, etc. that is available in the electronic cash ledger, to the appropriate tax or cess head under IGST, CGST and SGST in the electronic cash ledger. Hence, if a taxpayer has wrongly paid CGST instead of SGST, he can now rectify the same using Form PMT-09 by reallocating the amount from the CGST head to the SGST head.

> A tax payer filed GSTR-3B by claiming ITC of 2 Cr. Instead of 2 Lacs, now tax payer can not do anything about it, either he has to reverse it by paying appropriate interest or he has to utilize it. The same case happened that went in Patna High Court, and Patna High court given a landmark judgment that Intention of the tax payer has to be seen, there is no option to revise the GSTR-3B by using which tax payer can correct the same. Finally the HC allowed the assess to file a Manual GSTR-3B. So it has to be kept in mind if we wrongly claimed any ITC we should not utilize it, if we utilize the same nothing can be done then.

> As per rule 36(4) of the CGST Rues 2017 inserted by notification number 49/2019 CT dated 09.10.2019,there shall be a capping of 20% which later on reduced to even 10% of the eligible Credit. This has to be done on a monthly basis. But by notification number 30-36/2020 CT dated 03.04.2020, Circuar number 136 dated 03.04.2020 it has been said that the capping for the month of February to August can be done Cumulatively in the GSTR-3B of September 2020.

> As per Rule 86A, if a supplier does not pay taxes to govt on supplies made by him, the recipient will not be allowed to take ITC. So now the recipient needs to be cautioned about this draconian provision. However a WRIT has been filed against this. Govt has issued guidelines to Know Your Supplier(KYS) u/s 155.

New Returns of GST w.e.f. 1st October 2020

In GST 31st Council Meeting, Council decided to introduced a new GST return Regime which will not only ease the Return system but also stop fake invoices.

So New GST Return Forms will be introduced which will replace the existing GST returns.

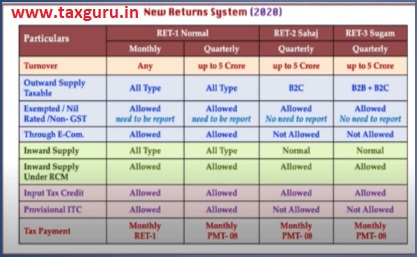

| Return/Form | Frequency | Category of person | Remarks |

| GST RET-1 (NORMAL) | Monthly | Agg. T/O >5 cr in PFY | Composition Scheme Dealer, NRTP, OIDAR service provider, ISD not liable to file |

| Quarterly | Agg. T/O <5 cr in PFY | -Do- | |

| GST RET-2 (SAHAJ) | Quarterly | Agg. T/O < 5Cr in PFY and Supply only to B2C | Composition Scheme Dealer, NRTP, OIDAR service provider, ISD, person whose turnover more than Rs.5 Crores Et person who supply to B2B, can not file GST RET-2 (SAHAJ) |

| GST RET-3 (SUGAM) | Quarterly | Agg. T/O < 5Cr in PFY and Supply only to B2C And B2B | Composition Scheme Dealer, NRTP, OIDAR service provider, ISD, person whose turnover more than Rs.5 Crores, can not file GST RET-2

(SAHAJ). |

| FORM GST ANX-1 | Monthly!

Quarterly |

Filing of this Form is mandatory before filing of GST RET-1 !2!3. | Annexure of outward supplies and inward supplies attracting reverse charge. This FORM is in lieu of FORM GSTR -1. |

| FORM GST ANX-2 | Auto Populated | Data uploaded by the supplier in GST ANX- 1, will be shown in GST ANX-2. These

details have to be ‘accepted’ or ‘rejected’ or ‘marked as pending’ before filing of GST RET-1 !2!3. |

Annexure of inward Supplies. |

| GST ANX -1A | Auto Populated | Amendment to Form GST ANX-1. | To make any amendment in GST ANX-1, this Form shall be filed. |

| GST RET-

1A!2A!3A |

Auto Populated | Amendment to Form GST RET-1 !2!3 | To make any amendment in GST RET-1!2!3, this Form shall be filed. |

| GST PMT-08 | Monthly!

Quarterly |

Payment of Self-assessed tax |

New Returns of GST w.e.f. 1st October 2020

> Monthly filers are allowed only GST RET-1

> Quarterly filers can choose between GST RET-1/2/3

> Uploading of invoices can be done throughout the month & credit can be claimed accordingly

> Matching tool would be provided to match Purchase Register with inward supply annexure in Form GST ANX-2

> New return system would deter habitual non-filers as auto population of Credit would stop in GST ANX-2

> Supplier uploads Invoices in ANX-1 > Recipient view invoice in ANX-2,can accept or reject but cant amend > rejected invoices seen by supplier > supplier amend the data > send back > final version.

> ITC on Missing Invoices i.e. Provisional ITC(T+2) is allowed only in case of RET-1 and not allowed in RET-2/3

> E-com supply can not be done through RET-2/3

> Tax payment in all returns is Monthly Through PMT-08

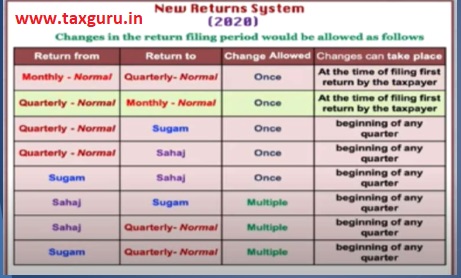

New Returns of GST w.e.f. 1st October 2020

> Some Extra Important Points to take into Effect:

How Taxable Person can switch Between the Returns: