Private Ltd. Companies – compliances & reports by management & auditor’s

Nowadays, there are lot of start-ups or business in India which have one of the most popular legal entity i.e., Private Limited Company (which gives a lot of benefits).

These start-ups has become a trend but certainly, it is not at all an easy task to run a private corporation (since law demands and tries to limit private companies by issuing a lot of compliance & conditions maintained under Companies Act, 2013) at least not for a faint-heart (because majority of small businesses don’t fulfil their compliance requirements in the opening years, they end up paying heavy penalties (up to Rs. 1 Lakh a year) for failing to do so)

Managing the day to day operations of regular business along with complying the corporate laws can be little taxing for any entrepreneur. Hence management takes help of professionals like CA’s, CS’s & etc.., to ensure timely fulfilment of compliances, without any levy of interest or penalty.

Sec. 2(68) of The Companies Act, 2013 – ‘Private Company’ means a company having a minimum paid-up share capital of one lakh rupees or such higher paid-up share capital as may be prescribed, and which by its articles –

(i) Restricts the right to transfer its shares

(ii) Except in case of One Person Company, limits the number of its members to two hundred,

Provided that where two or more persons hold one or more shares in a company jointly, they shall, for the purposes of this clause, be treated as a single member;

Provided further that –

a. Persons who are in the employment of the company &

b. Persons who, having been formerly in the employment of the company, were members of the company while in that employment and have continued to be members after the employment ceased, hall not be included in the number of members &

(iii) Prohibits any invitation to the public to subscribe for any securities of the corn

Here are some of the common compliances which a private limited companies has to mandatory ensure:

APPOINTMENT OF AUDITOR

Appointment is mandatory thing. As provided under the CA’2013, an auditor will be appointed by a company for a term of 5 years (2 terms of 5 consecutive years, in case of firm auditor) and if it is a new, the auditor has to be appointed within one month of the inauguration of the enterprise. (File a form ADT – 1 within 15 days)

ANNUAL ROC FILING

Once in a year

1. Annual Returns – within a period of 60 days from the last annual meeting held. (The annual returns will be calculated from 1st April to 31st March) (Form MGT – 7)

2. Financial Statements – within a period of 30 days from the last annual meeting held. (Form AOC – 4)

“To Know about their financial growth and valuations.”

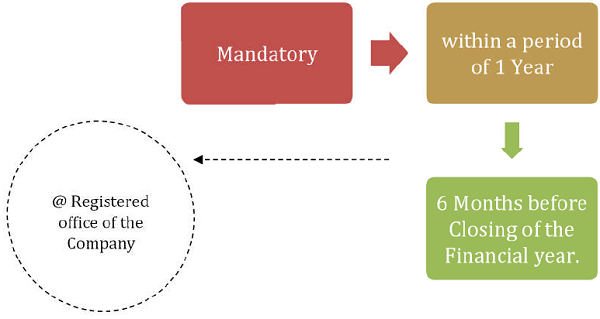

ANNUAL GENERAL MEETING

“Motto of AGM is to discuss certain essential topics like approval of financial statement, appointment of auditors, salary or remuneration of directors, and etc..,”

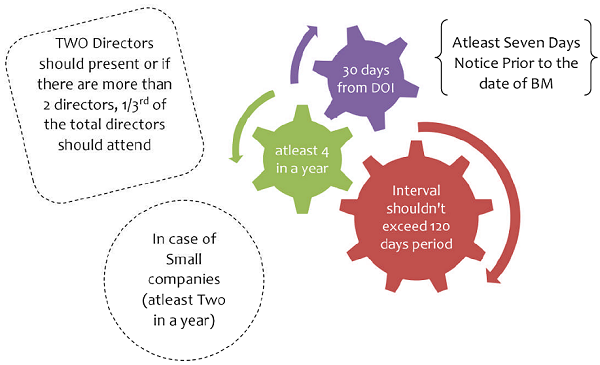

BOARD MEETINGS

“To discuss about the financial & Operational growth in a Company (so far from Start-up point of view it’s an important compliance).”

REPORTS OF DIRECTORS

INCOME TAX

MAINTENANCE OF RECORDS

D – Directors; M – Members & S – Shares … .

OTHER COMPLIANCES

There are some events based compliances too, which are –

a) Giving loans to other companies.

b) Providing loans to directors.

c) Change in paid-up capitals of the enterprise.

d) Opening or Closing up bank accounts.

e) Appointment or Change in Auditor of the Enterprise.

f) Allotment on new shares or transfer of shares.

Different forms are required to be filed with the registrar for all such events within specified time periods.

Compliance by Auditor –

SEC. 143 (1) – SPECIFIC ENQUIRIES

Every auditor of a company shall have a right of access at all times to the books of accounts and vouchers of the company whether kept at the registered office of the company or at any other place.

He shall be entitled to require from the officers of the company information and explanation as the auditor may consider necessary for the performance of his duties as auditor.

The auditor may also inquire into the following matters, viz.,

SEC. 143 (2) – AUDIT REPORT

SEC. 143 (3) – PRINCIPAL ASSERTIONS

The auditor’s report shall also state –

1. Whether he has sought & obtained all the information and explanations which to the best of his knowledge and belief were necessary for the purpose of his audit and if not, the details thereof and the effect of such information on the financial statements.

2. Whether, in his opinion, proper books of account as required by law have been kept by the company so far as appears from his examination of those books and proper returns adequate for the purposes of his audit have been received from branches not visited by him;

3. Whether the report on the accounts of any branch office of the company audited under sub section (8) by a person other than the company’s auditor has been sent to him under the proviso to that sub section and the manner in which he has dealt with it in preparing his report.

4. Whether company’s balance sheet and profit and loss account dealt with in the report are in agreement with the books of account and returns.

5. Whether in his opinion, the financial statements comply with accounting standards.

6. The observations or comments of the auditors on financial transactions or matters which have any adverse effect on the functioning of the company

7. Whether any director is disqualified from being appointed as a director under section 164(2).

A person who is a director of a company which –

1. Failed to repay deposits or interest payable thereon or to redeem debentures or to pay dividend declared and such default continues for 1 year or more.

2. Has failed in filing of annual returns or financial statements & such default continues for more than 3 years.

“Shall not be eligible to act as a director in such company or any other company for 5 years from the date of such default”

8. Any qualification, reservation or adverse remark relating to the maintenance of accounts and other matters connected therewith.

Author Bio