Section 54 of CGST Act 2017 provides various mechanism to the taxpayer under which they can claim REFUND of the INPUT TAX CREDIT (ITC) they had paid on the purchase of their supplies and otherwise also.

> PROVISION

As per explanation 3 to section 54 the registered person may claim refund of any unutilised input tax credit at the end of any tax period:

Provided that no refund of unutilised input tax credit shall be allowed in cases other than––

(I) zero rated supplies made without payment of tax;

(II) where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies), except supplies of goods or services or both as may be notified by the Government on the recommendations of the Council.

> TIME LIMIT

Any registered person claiming refund under this category has to file the same within two years from ‘Relevant Date’.

Where Relevant Date means:

- Prior to 02.2019: in the case of refund of unutilised input tax credit under clause(II) of first proviso to section 54(3), the end of financial year in which claim for refund arises.

- E.F. 01.02.2019: in the case of refund of unutilised input tax credit under clause(II) of first proviso to section 54(3), the due date for furnishing return under section 39 for the period in which such claim for refund arises.

> ANALYSIS OF AMENDMENT

Let’s take an example suppose any registered person wants to claim refund for JULY 2017 then prior to such amendment he can apply for refund u/s 54 till MARCH 2020 i.e. he was provided two years from the end of financial year to which refund relates BUT as per amendment a registered person was eligible to apply for refund till 20th MAY 2019. Since date for July 2017 was 20th May 2017.

> PRACTICAL PROBLEM DUE TO AMENDMENT

- When you apply refund for tax period July 2017 after 20th May 2019 and so on, the department rejects your application on the ground of amendment effective from 01.02.2019 onwards that the due date for refund has lapsed.

- Now argument here arises that due date mentioned on GST portal from July 2017 to Feb 2019 is 31st March 2019.

- In response to argument raised the proper officer justifies his action by stating that the due date 31st March 2019 mentioned on GST portal is for the purpose of waiving off late fee during that periods.

- In my opinion the said amendment is effective 02.2019 onwards, which means that refund applied for tax period February 2019 onwards the relevant date shall be determined as per this amendment. Whereas for refund related to period prior to February 2019 should be determined according to earlier provisions. (My basis for opinion is that when this amendment was inserted period of 2 years has not lapsed for F.Y. 2017-18, as GST was introduced from 01.04.2017)

> AUTHORS OPINION

In my opinion the argument provided by department is baseless and the above matter is subject to appeal.

> DOCUMENTS REQUIRED TO BE FILED

| Declaration/statement/undertaking/ certificates to be filled online | Supporting documents to be additionally uploaded |

| Declaration under second & third proviso to section 54(3) | Copy of GSTR-2A downloaded from portal in PDF format of the relevant period. |

| Declaration under section 54(3)(ii) | Statement of invoices (Annexure-B) |

| Undertaking in relation to section 16(20(c) and section 42(2) | Self-certified copies of invoices entered in Annexure B whose details are not found in GSTR-2A of the relevant period. |

| Statement 1 under rule 89(5) | |

| Statement 1A under rule 89(2)(h) | |

| Self-declaration under rule89(2)(1) if amount claimed does not exceed two lakh rupees, certification under rule 89(2)(m) otherwise |

> PROCEDURE FOR FILING THE APPLICATION

1. Login on taxpayer account on www.gst.gov.in.

2. Click on tab Refund > application for refund > select Refund on account of ITC accumulated due to Inverted Tax Structure option > select the relevant tax period for which refund is to be applied.

3. A dialogue box pops up asking Do you have refund for selected period? Clock on YES button. Your refund application opens up.

4. On the top of application a link appears click to fill the details of invoices for inward and outward supplies > upload Statement 1A and Validate it. If any error exists generate error report & correct the errors in statement Repeat the above process until your statement is validated without any error > click on proceed button. After clicking on proceed button you will get back to main page.

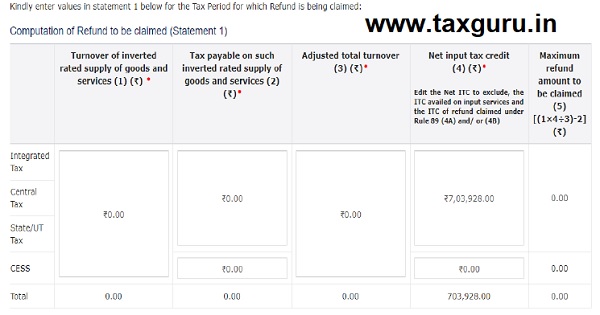

5. Now enter the various values in statement 1 for tax period for which refund is being claimed (Make sure you don’t enter any bogus value)

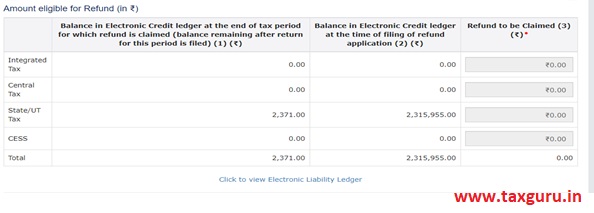

6. Now the amount calculated in in column no. 5 shall be entered in column no. 3 in amount eligible for refund under various heads i.e. IGST/CGST/SGST. Make sure that the amount entered under various head shall be lower of amount auto populated in column 1 & 2.

7. Now Select the bank account number in which refund amount is to be credited (Make sure that the selected Bank account is validated by )

8. Now upload all the supporting documents as specified above & click on SAVE button.

9. The check box under head declaration & undertaking gets activated. Select the check boxes & click on SAVE button.

10. Click on PREVIEW button & view the drafted copy of application.

11. Click on SUBMIT button & finally click on PROCEED button.

12. Select the Authorised Signatory & file the application through EVC/DSC. After filing the application the ARN is generated which shall be used for tracing the status of the application.

> HOW TO CALCULATE REFUND AMOUNT

Maximum Refund Amount = (Turnover of inverted rated supply of goods and services X Net input tax credit / Adjusted total turnover) – Tax payable on such inverted rated supply of goods and services

Where,

-

- “Net ITC” shall mean input tax credit availed on inputs during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or

- “Turnover of inverted rated supply of goods” means the value of the inverted supply of goods made during the relevant period.

- “Tax payable on such inverted rated supply of goods” means the tax payable on such inverted rated supply of goods under the same head, i.e. IGST, CGST, SGST.

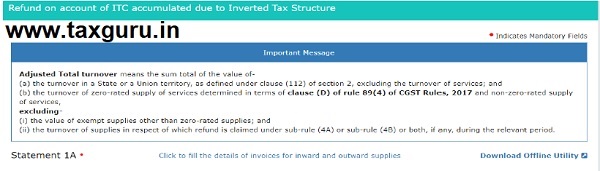

- “Adjusted Total turnover” means the turnover in a State or a Union territory, as defined under clause (112) of section 2 of CGST Act, excluding the value of exempt supplies other than inverted-rated supplies, during the relevant

- “Relevant period” means the period for which the claim has been

EXAMPLE

Details of Inward supplies

| PARTICULARS | VALUE | GST RATE | GST(ITC) |

| Inward supplies used for the manufacture of good which is taxed at 5%

Inward supplies used for the manufacture of good which is taxed at 18% |

Rs.2000000 | 12% | Rs.240000 |

| Rs.1500000 | 18% | Rs.270000 | |

| Total ITC | Rs.510000 |

Details of Outward supplies

| PARTICULARS | VALUE | GST RATE | GST(ITC) |

| Turnover of inverted rated supply taxed at 5% | Rs.3000000 | 5% | Rs.150000 |

| Turnover of other supply taxed at 18% | Rs.2000000 | 18% | Rs.360000 |

| Total Turnover | Rs.5000000 | Rs.510000 |

Maximum Refund Available = (3000000*510000/5000000)-150000 = Rs.1560000

> ITEMS ON WHICH REFUND IS PROHIBITED

Initially Notification No. 5/2017- Central Tax Dated 28-06-2017 was issued specifying list of prohibited items on which refund shall not be allowed. However through Notification No. 20/2018 dated 26-07-2018 the refund shall be allowed in respect of

strike items provided the in respect of strike items the accumulated ITC up to month of July 2018 shall lapse i.e. no refund shall be allowed for period up to July 2018

| S.NO. | Tariff item/heading/sub heading/chapter | Description of Goods |

| 1. | 5007 | Woven fabrics of silk or of silk waste |

| 2. | 5111 to 5113 | Woven fabrics of wool or of animal hair |

| 3. | 5208 to 5212 | Woven fabrics of cotton |

| 4. | 5309 to 5311 | Woven fabrics of other vegetable textile fibres, paper yarn |

| 5. | 5407, 5408 | Woven fabrics of manmade textile materials |

| 6. | 5512 to 5516 | Woven fabrics of manmade staple fibres |

| 7. | 60 | Knitted or crocheted fabrics [All goods] |

| 8. | 8601 | Rail locomotives powered from an external source of electricity or by electric accumulators |

| 9. | 8602 | Other rail locomotives; locomotive tenders; such as Diesel-electric locomotives, Steam locomotives and tenders thereof |

| 10. | 8603 | Self-propelled railway or tramway coaches, vans and trucks, other than those of heading 8604 |

| 11. | 8604 | Railway or tramway maintenance or service vehicles, whether or not self-propelled (for example, workshops, cranes, ballast tampers, trackliners, testing coaches and track inspection vehicles) |

| 12. | 8605 | Railway or tramway passenger coaches, not self-propelled; luggage vans, post office coaches and other special purpose railway or tramway coaches, not self-propelled (excluding those of heading 8604) |

| 13. | 8606 | Railway or tramway goods vans and wagons, not self-propelled |

| 14. | 8607 | Parts of railway or tramway locomotives or rolling-stock; such as Bogies, bissel-bogies, axles and wheels, and parts thereof |

| 15. | 8608 | Railway or tramway track fixtures and fittings; mechanical (including electro-mechanical) signalling, safety or traffic control equipment for railways, tramways, roads, inland waterways, parking facilities, port installations or airfields; parts of the foregoing |

> FREQUENTLY ASKED QUESTIONS

QUES1: what is the time limit in which proper office is required to sanction the refund?

ANS1: As per section 56 of CGST ACT 2017, a proper officer is required to sanction the refund within 60 days from the date of filing.

QUES2: what if proper officer does not sanction refund within said period?

ANS2: As per section 50 of CGST ACT 2017, if proper officer fails to sanction the refund within 60 days, then the applicant shall be eligible for interest at 6%p.a.

QUES3: When can proper officer issue Deficiency Memo?

ANS3: Deficiency memo is issued through RFD-03. Whenever proper officer on receipt of application finds that the supporting documents attached by applicant are incomplete he may issue RFD-03.

QUES4: Can applicant make fresh application if RFD-03 after issuance of RFD-03.?

ANS4: Yes, applicant have to file fresh application for same refund period.

QUES5: Whether an applicant take input of those invoices which are not appearing in GSTR-2A while calculating amount of eligible ITC?

ANS5: Yes, an applicant is eligible to take ITC of such invoices which are not appearing in GSTR-2A provided he uploads scanned copy of such invoices as supporting documents. But there exist practical problem, that department does not consider the ITC of invoices which are not appearing in GSTR-2A.

QUES6: Is it compulsory to mention HSN for every invoice mentioned in annexure b?

ANS6: As per the revised circular issued by the cbic, the applicant is required to mention HSN only for those invoices for which it is mentioned in there invoice. Lets take an example, suppose applicant receives supplies from any registered person whose turnover is below 1.5 crores, then the invoice he must be having might not contain HSN because it not compulsory for him to mention. In such case applicant shall mention NA in front of invoice under head HSN.

QUES7: How to enter B2C detail in Statement 1A?

ANS7: This is most crucial point when you prepare statement 1A and frankly speaking you encounter problem because your sheet is not getting validated. While entering B2C details you must take total of all B2C invoices and enter it as single entry.

QUES8: Whether while preparing statement 1a can we paste all the entries directly after copying from excel sheet?

ANS8: It is not advisable to directly paste the data in columns because there may be chances that your file gets corrupted and when you upload json file it may show invalid data format error. In case you still want to use copy & paste then instead of simple paste option use paste special key. Moreover while preparing statement be cautious and rather uploading whole file you can validate in parts also.

QUES9: In case incomplete documents are uploaded by applicant what are the options available to proper officer other than issuance of RFD-03?

ANS9: The proper officer is not bound to issue RFD-03 only, he can issue issue show cause notice in RFD-08. The applicant is required to submit his response in RFD-09 within the prescribed period.

QUES10: What are consequences on issuance of RFD-08?

ANS10: If proper officer is satisfied with the response submitted by applicant in RFD-09 he will issue RFD-06(sanction refund) and if not satisfied by response then your refund will be rejected.

QUES11: Whether refund application once rejected can be filed again?

ANS11: If application is rejected by proper officer then applicant cannot make fresh application again for same refund period. However, if he is of view that department is unjustified in rejecting the refund he may file an appeal.

Author Bio

sir, we are supplier of edible oil (gst-5%). we supply the edible oil in bulk qunatity as well in small consumer packs. Sale proceeds from sale of consumer pack – 10 lacs sale proceeds from bulk sale- 10 lacs. purchase value of edible- 18 lacs and purchase value of packing material is 1.80 lacs. plz let me know value of inverted rated turnover and adjusted turnover.

IN THE AFOREMENTIONED ANALYSIS YOU HAVE CONSIDERED DUE DATE OF FILING OF GST RETURN FOR THE M/O JULY-2017 AS MAY-2017 AND ACCORDINGLY CALCULATED THE PERIOD OF TWO YEARS EXPIRING ON MAY-2019 WHERE AS THE DUE DATE OF JULY-2017 SHOULD BE AUGUST-2017 AND ACCORDINGLY LIMITATION OF REFUND APPLICATION SHOULD BE AUGUST-2019. PLEASE EXPLAIN .