1. Initiation of recovery proceedings. (Sec 78 of the CGST Act)

Any amount payable by a taxable person in pursuance of an order passed under this Act shall be paid by such person within a period of three months from the date of service of such order failing which recovery proceedings shall be initiated:

Provided that where the proper officer considers it expedient in the interest of revenue, he may, for reasons to be recorded in writing, require the said taxable person to make such payment within such period less than a period of three months as may be specified by him

2. Practical Aspects.

In GST regime, where any sum is payable by the taxpayer on account of scrutiny, assessment, enforcement, adjudication and appeal process, and remains unpaid, the tax authorities would initiate the recovery process by adopting any of the following modes as provided in the GST laws. Some of the modes of recovery available to tax official are as under:

- Detaining and selling of goods of the taxpayer in the possession of the tax department/ other officer

- Issuance of letter / correspondence to third parties including banks / any other government departments/ debtors/ any other person provided in law/ successor or transferee or legal heir

- Distrain, detain and sell immovable and movable property

- Issuance of certificate to revenue authorities for recovery as arrears of Land Revenue

- Application to magistrate to recover as fine

- Recovery from Electronic Cash Ledger/ Electronic Credit Ledger of a taxpayer

- the proper officer may deduct or may require any other specified officer to deduct the amount so payable from any money owing to such person which may be under the control of the proper officer or such other specified officer;

- Any other mode as prescribed under law.

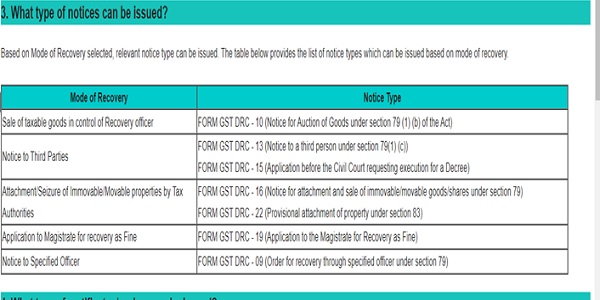

3. Notices.

4. Recovery –Practical Aspects

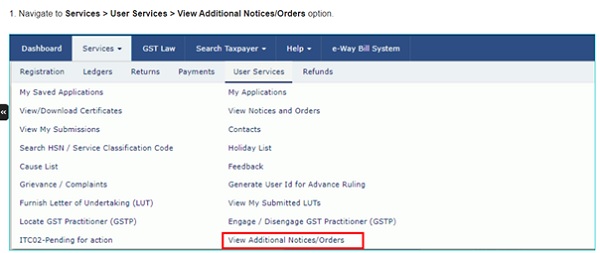

To view the recovery details, perform following steps:

1. Navigate to Services > User Services > View Additional Notices/Orders option.

(Source:https://tutorial.gst.gov.in/userguide/demandsandrecovery/index.htm#t=manual_recovery_from_taxpayer.htm)

(Source:https://tutorial.gst.gov.in/userguide/demandsandrecovery/index.htm#t=manual_recovery_from_taxpayer.htm)

5. Payment of tax and other amount in instalments.(Sec 80 of CGST Act)

On an application filed by a taxable person, the Commissioner may, for reasons to be recorded in writing, extend the time for payment or allow payment of any amount due under this Act, other than the amount due as per the liability self-assessed in any return, by such person in monthly instalments not exceeding twenty four, subject to payment of interest under section 50 and subject to such conditions and limitations as may be prescribed:

6. Practical Aspects of Deferred Payment

FORM GST DRC – 20 is an application form that can be filed by any taxpayer to apply for one of the following two options available to him in case he cannot pay the entire amount due under the GST Act in one go:

- Deferred payment: when dues are deferred for payment at later stage

- Payment in instalments: when due is paid in installments over a period of time

Once you have filed FORM GST DRC – 20, following actions will take place on the GST Portal:

- GST Portal will generate and display Application Reference Number (ARN) receipt with an option to”Save and Print” the same.

- SMS and Email will be sent to you intimating ARN and successful filing of the Form.

- Your application for payment in Installments shall be submitted to the Commissioner/proper officer of concerned jurisdictional authority and will become a pending item in his/her queue of work-items. The Officer will adjudicate on the application and either Accept or Reject or Accept with modification your request. You can access the generated ARN and view the filed application from the following navigation: Dashboard >Services > User Services > My Applications > Case Details > APPLICATIONS

- Demand ID in DCR, in respect of which you have filed this application, will be flagged to show that such an application is filed against the Demand ID.

7. Tax to be first charge on property.(Sec 82 of the CGST Act)

Notwithstanding anything to the contrary contained in any law for the time being in force, save as otherwise provided in the Insolvency and Bankruptcy Code, 2016, any amount payable by a taxable person or any other person on account of tax, interest or penalty which he is liable to pay to the Government shall be a first charge on the property of such taxable person or such person

8.Provisional attachment to protect revenue in certain cases.(Sec 83 of the CGST Act)

(1) Where during the pendency of any proceedings under section 62 or section 63 or section 64 or section 67 or section 73 or section 74, the Commissioner is of the opinion that for the purpose of protecting the interest of the Government revenue, it is necessary so to do, he may, by order in writing attach provisionally any property, including bank account, belonging to the taxable person in such manner as may be prescribed.

(2) Every such provisional attachment shall cease to have effect after the expiry of a period of one year from the date of the order made under sub-section (1).

9.References

1. https://tutorial.gst.gov.in/userguide/demandsandrecovery/index.htm#t=FAQs_recovery_from_taxpayer.htm

2. https://tutorial.gst.gov.in/userguide/demandsandrecovery/index.htm#t=FAQs_recovery_from_taxpayer.htm

3. https://tutorial.gst.gov.in/userguide/demandsandrecovery/index.htm#t=manual_recovery_from_taxpayer.htm

4. https://www.cbic.gov.in/resources//htdocs-cbec/gst/CGST%20Act%20Updated%20as%20on%2031.08.2021.pdf

5.https://tutorial.gst.gov.in/userguide/demandsandrecovery/index.htm#t=FAQs_application_for_deferred_payment.htm

Author Bio