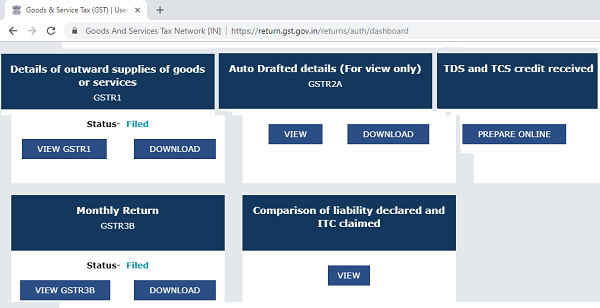

NEW FEATURE ROLLING OUT ON A GST PORTAL

As the Due date of GSTR-9 is notified by the Government as 30th June 2019 the government is trying to simplify the Reconciliation of the Returns. ITC claimed as this is major issue in Reconciliation of ITC claimed under GSTR-3B & ITC as per GSTR-2A.

The government has given easy outcome as Credit and liability Statement.

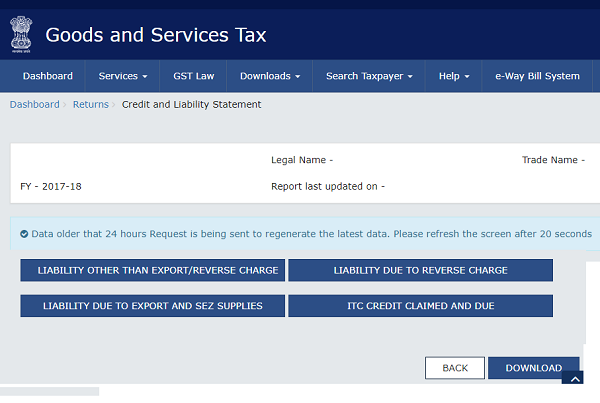

As After the view the Detail for the Various it will Take time of few Seconds to Generate the All Statement of Following

1. Liability other than Export/Reverse Charge

2. Liability to Reverse charge

3. Liability Due to Export and SEZ Supply

4. ITC Credit Claimed and DUE

As the Major issue as Mentioned above is ITC Claimed and Due.

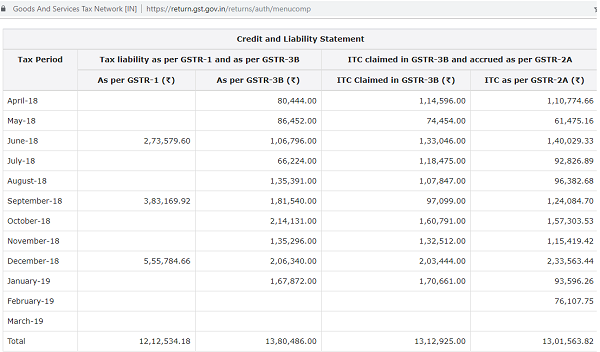

As For FY 2017-18 the ITC claimed as per GSTR-3B, ITC as per GSTR-2A, Shortfall (-)/ Excess (+) in liability (GSTR3B – GSTR2A), Cumulative Shortfall (-)/ Excess (+) in liability (GSTR3B – GSTR2A)

A. As the Shortfall /Excess computed and the Figures of such is Calculated Automatically.

B. Cumulative Shortfall /Excess is calculated through outcome of point A Adjusting the Excess of Credit if in any Tax as per the ITC rule & And if After Cumulative Adjustment of tax is still there is a shortfall the the Excess liability will be calculated and is excess of either of the tax then Excess credit will be Shown as per IGST, CGST, SGST.

As For FY 2018-19 The image of Credit and Liability Statement.

Hope This New Initiative By Government will Be Helpful for Business Person or to the Professional in Reconciliation of GST Figures.

Author Bio

While doing GST Audit for a company, I found that there were some differences between 2A and 3B. The invoices for which the ITC claimed in 3B is not in 2A. Ans it comes to 13% of the eligible ITC. Please clarify whether the ITC of 13% not in 2A needs to be reversed or not?

I have download the chart of comparison betwnn ITC claimed in GSTR-3B and accrued as per GSTR-2A fy 2019-20 then their is diff between actual ITC taken in GSTR 3b and download chart.

month itc as per chart itc as per 2a diff

April-19 93,13,079 99,56,295 -6,43,216

but i have claimed itc for the month of april is 9025835/- and their is diff of 643216/-

in all the month month fy 18-19 & 19-20 diff in ITC

please sugguest

there is lesser ITC claimed in 3B for the year 2017-18, during the same year Auto populated in 2 A is excess of ITC availed but it is related to business. Now How to adjust that ITC availed amount, Now we r in 2019-20 please clarify it.

When excess itc claimed in gstr-3b in september 2017 but not reversed till date can we reverse that excess itc claimed in august 2019 filing of gstr-3b or we should do it only by gstr-9 .

The ITC of CGST SGST wrongly claimed as IGST which got noticed during reconciliation So How can the same be rectified ?

My vendor have uploaded B2B invoices issued in my favor, but in GSTR2A the return status is NOT SUBMITTED, shall this affects the auto populated amount in Comparison of Gstr3b vs. Gstr2a.

How can we treat the difference between ITC claimed and ITC aoto populated ?

If my party did not submit my details in his GSTR 1 and i have claimed the ITC input so now how can we treat/correct these fault ?

The difference between ITC claimed and ITC populated is an offence ?

Any penalty on the amount excess claimed ?

how to reverse the excess claimed itc of the year 2017-18 in the year 2018-19

GST R9 FACED GST 3B AND GST R1 SUBITED THE RETURNS AS PER GST PORTAL FACED GST R 3B AND GST R1 AND GST R 2A ITC TH SUPPLIERS AFTER YEAR THE REPORT IN GST R 1 SO FOR GST R3B ITC GST R 2A ITC SMALL DIFFRENCE WHEN MISSED INOVICES WHEN ACCOUNT FOR GIVE ME TIME FOR AND ALSO SUBMITED THE INCOMETAX RERUN THAT YEAR AGAIN ACCOUNT FOR THE YEAR DIFF. COME HOW TO RECTFY PLEASE INFORM HELP FOR RECTICATION ITC PROBLEMS