GST authority had issued various notifications since GST had been introduced in India. Many of the notifications provided much needed relief, clarification etc. Notification 20/2017 & 22/2017 (Central & Integrated Tax Rate) appears to be such notifications vide which GST authority tried to bring more flexibility in GST regime. However, did it bring the flexibility in the GST regime or it made the regime even more complicated? To find out the answer all you need to do is, sit back, relax & enjoy the write-up!

What is GTA under GST?

As per the definition given in notification 11/2017 (Central Tax Rate), GTA or “goods transport agency” means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called. Hence, not all the transporter is GTA. For eg. Transportation of furniture in mini truck; unless it issues consignment note, it cannot be called as GTA under GST. So mere transportation does not make one GTA under GST, to test if a person qualifies as GTA under GST or not we need to get every answer of the following questions as YES.

1) Is s/he providing Transportation service? – YES

2) Is it transport for Goods – YES

3) Is s/he issuing consignment note – YES

If any of the answer of the above questions is no, then s/he is not GTA under GST.

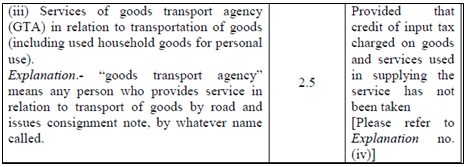

Now that, it is understood what is GTA under GST let’s get straight into the matter. Just before the introduction of GST Law in India, on 28th June 2017, GST authority had issued Notification no. 11/2017 (Central Tax Rate). Relevant entry of the same specifies, rate of GTA service is 2.5% (5% IGST) with condition that, the service provider (GTA) is not allowed to take Input Tax Credit (ITC):-

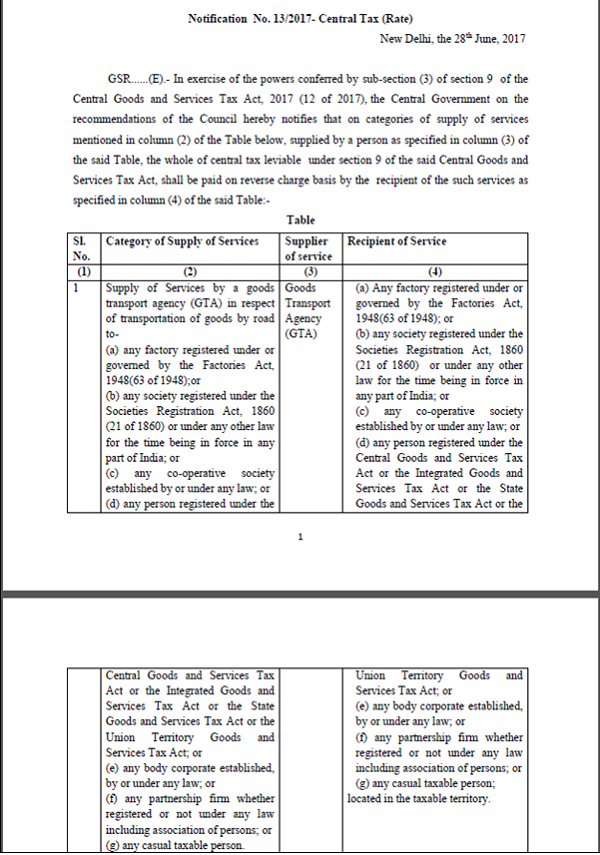

On the same day, notification no. 13/2017(Central Tax Rate) came up with the list of services to be covered u/s 9(3) of CGST Act or services to be covered under Reverse Charge Mechanism (RCM). Relevant entry of the said notification states GTA service provided by the GTAs to business entity etc. to be paid by the recipient as follows:-

However, GTA service provided by the service provider to the individual is not covered under RCM as per the above notification. So GTAs were still required to pay GST on the GTA service extended by them to the individuals and the said tax was required to be paid in cash due to notification number 11/2017 (Central Tax Rate) which does not allow ITC to GTA service providers.

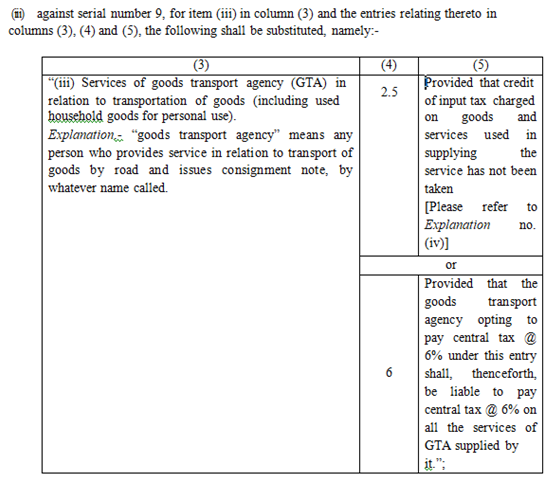

It appears that, to come up with a resolution, GST authority had further issued notification number 20/2017 (central tax rate) on 22nd August 2017 which amends the earlier notification no. 11/2017 (central tax rate) & gives option to the GTAs vide relevant entry to extend the facility of Input Tax Credit scheme to the GTAs, by making the GST rate @6% (12% IGST). However, It is pertinent to note that, notification number 20/2017 (central tax rate) does not amend notification number 13/2017 (Central Tax Rate), which mandates RCM for GTA service at the hand of business entities.

Notification number 20/2017 (central tax rate) states,

“…. the Central Government, on the recommendations of the Council, and on being satisfied that it is necessary in the public interest so to do, hereby makes the following amendments in the notification of the Government of India, in the Ministry of Finance (Department of Revenue), No. 11/2017- Central Tax (Rate), dated the 28thJune, 2017…”

In addition, following entry of the said notification states as follows:-

From the above it appears that, the intention of the notification was to give an option to remove RCM for GTA service & to provide GTAs an option to utilise ITC for the purpose of payment of GST on all the services provided by it by making the rate of GST at 6% (12% IGST) as oppose to 2.5% (5% IGST) earlier. However, if no further notification was issued in this regard, it would have create following issues:-

a) Business entity would have bound to pay tax on GTA service by virtue of notification number 13/2017 (Central Tax Rate) and would have taken ITC on the basis of Self invoice u/s 31(3)(f) of CGST Act.

b) On the other hand, GTA service provider would have been forced to pay @ 6%/12% (if opted so), as notification number, 20/2017 (Central Tax Rate) stipulates the condition to pay CGST @6% (12% IGST) on all the services. It is relevant to note that, the same would have been uploaded in GSTR 1 of the GTAs, and credit of the same would have automatically flow to the GSTR-2 of the recipients (business entities), by which they can avail the credit (ITC).

This would have essentially created ambiguity as follows,

i. The business recipient & GTA both would have forced to pay tax on a single transaction. Double taxation on a single service!

ii. There would have been confusion about ITC. One on the basis of the self-invoice u/s 31(3)(f) [point (a) above] and another on the basis of supplier’s invoice. [point (b) above]

iii. The problem wold have been more serious, had the supplier of GTA service been from other state. There might have been a situation, where on a same supply, supplier would have charged IGST (as interstate), whereas on the self-invoice it would have been CGST & SGST by the logic of GSTIN of the invoicing party & the recipient party comes under the same state.

Due to this, GTAs who opted to pay @6% or 12% (as the case may be) would have started facing the problem, as business entities would have reservation on the same. Large business entities would have considered payment to the extent of value of GTA service to the GTAs and pay GST on the same directly to GST authority based on self-invoice & take credit. Whereas, GTAs would have been claimed reimbursement of the 6% GST (or 12% IGST) as it is a statutory payment which GST law mandates to pay.

To make it interesting let’s take an example of Mr. Ram who is a GTA entity & Mr. Sham who is business entity. Earlier Ram was raising invoice value of Rs 1,00,000 for the GTA service provided by him to Sham & Sham was paying 2.5% (5% IGST) on it for Rs 5,000/- and was taking credit based on self-invoice raised by him. Also Sham was reimbursing the value of the service to the extent of Rs 1,00,000 to Mr. Ram as below:-

| Particular | Rs |

| Value of Service | 1,00,000 |

| GST(to be paid under RCM) | 5,000 |

| Total reimbursement/payment | 1,00,000 |

After notification number, 20/2017 (Central Tax or integrated tax rate), Mr. Ram had opted for paying 6% (12% IGST), and raised invoice for the supply made by him to Sham as below:-

| Particular | Rs |

| Value of Service | 1,00,000 |

| GST | 12,000 |

| Total | 1,12,000 |

Here is what would have happened,

1. Sham(GTA) would have paid tax @ 12% = 12,000

2. Ram (Business Entity) also would have paid tax @12% (RCM) = 12,000

3. Ram would have taken credit of the tax paid as mentioned in point (2)

4. Sham therefore would have not likely to pay tax amount once again to Ram (as it causes double payment)

5. Ram might not be getting reimbursement of the amount, which is statutory in nature.

6. Due to this Ram would have incurred loss of Rs 12,000/-

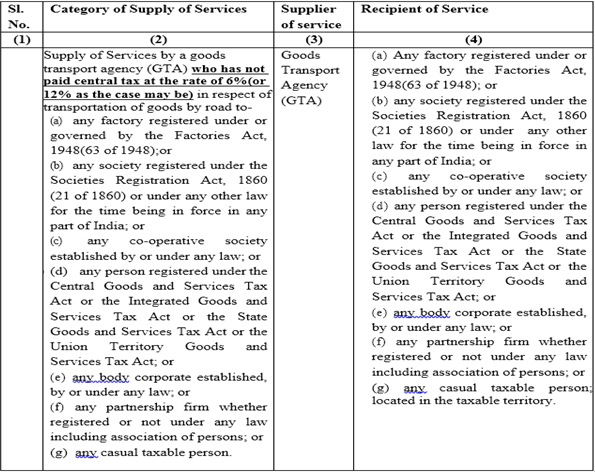

This is the reason why, GST authority had not only issued the notification 20/2017 (central tax/integrated tax rate) but also it had issued very crucial notification number 22/2017 (central tax/integrated tax rate). The notification 22/2017 (central & integrated tax rate) actually amends the RCM governing notification 13/2017(central tax rate) & 10/2017(integrated tax rate). It states:-

* Similar notification has been issued for integrated tax (rate)

Essentially notification number 22/2017 (central & integrated tax rate) makes the rate table of GTA service under the notification number 13/2017 (Central tax rate) or 10/2017 (integrated tax rate) as follows:-

Hence, rate structure & mechanism of GST for GTA services become as follows:-

| SL | Condition for GTAs | CGST | IGST | Mechanism (RCM or FCM) | Invoice u/s 31 of CGST Act |

| i) | No ITC benefit | 2.5% | 5% | RCM | 1. GTA will raise if registered by mentioning GST rate & applicability of RCM.

2. Recipient will raise u/s 31(3)(f), based on the rate mentioned by GTA invoice. |

| ii) | With ITC benefit | 6% (on all services) | 12% (on all services) | FCM | 1. GTA will raise if registered.

2. Recipient does not required to raise as it comes under FCM as per notification 22/2017 (central & integrated tax rate) |

The business entity should ensure the GST compliant invoice from the registered GTAs as per section 31, irrespective of the service comes under RCM or FCM. It will be helpful for the business entity to determine

1) Whether GTA is registered or not

2) GST rate structure (whether intra or inter)

3) Clarity on the applicability of RCM.

Author Pralay Chakraborty can be reached at 9705941371 or cp171185@gmail.com for feedback!

Disclaimer: The contents of this document are solely for informational purpose & personal view. It does not constitute professional advice or a formal recommendation. It is also not meant to portray anything against the GST law or any other law of the land for that matter. While due care has been taken in preparing the document, the existence of mistakes & omissions herein are not ruled out. The author does not accept any liabilities for any loss or damage of any kind arising out of any inaccurate or incomplete information in this document nor for any actions taken in reliance thereon. No part of this document should be distributed or copied without express written permission of the author.

Author Bio

We are paying GST on GTA Service at RCM base @ 5% , if i take the ITC for that 5 %

in business entity if the transporter is individual and not give us consigment note only invoice is raised then also rcm is applicable or not

Dear if GTA to GTA (FCM) is raise invoice than fcm division is paid RCM or not…

is RCM applicable for F.Y. 18-19

IS RCM APPLICABLE FOR FINANCIAL YEAR 18-19?

In case we are paying 5% GST on RCM basis, what is the threshold limit for RCM (If GTA Registered person or URD)

Can a service provider Opts foe both RCM and FCM ?

Hi Sir,

If Business Entity as a service receive pays 5% GST then will ot be able to take ITC of that. Or it will not be able to take as the rate it took is 5%. In other words, business entity pays 5% under RCM and can still take ITC?

Here it is found that you have not mentioned the Notification No. 22/2017 – Central Tax (Rate) in that article.

This is the notification which amends the Notification No. 13/2017 – Central Tax (Rate)

According to Notification No 22/2017 – Central Tax (Rate), Following is added in Notification No. 13/2017 – Central Tax (Rate)

(i) in the Table, against serial number 1, in column (2), after the words and brackets “goods transport agency (GTA)” the words and figure “, who has not paid central tax at the rate of 6%,” shall be inserted.

So as per the above Notification, Notification 13/2017 will not apply to the case where Central Tax has been paid at the rate of 6% ( GST @ 12%).

GTA is a Service Provider and Service receiver are registered tax payer and unregistered individuals. Unregistered persons are exempted now. Registered category should pay tax u/s 9 (3). Hence, GTA need not collect tax from anybody. For availing input, if he charge 12% means definitely cost will increase. Moreover it is unorganized sector also. I thing GTA will not collect tax @ 12%.

Dear Sir, The Interstate Trade ( House Rental) was not applicable for GST below Rs 20 Lakhs income per annum, upto March 31, 2018. What happens after March 31, 2018?? Will this benefit be continued for interstate homeowners in the NCT Region?? Please reply ASAP. Thanks. Dr Sandeep Parmar

Sir in case GTA charge GST@12% on forward charge then recipient did not to pay in RCM and GTA can avail ITC on inward supply, so there is no double taxation.Kindly correct me if i am wrong

Nothing anomaly, as it is advisable for a business entity to continue paying GST as per RCM and take rightful ITC on the basis of Self-Invoice. One thing needs to be done – direct the Transporter / GTA not to charge any GST on Invoice.

Kindly Read Notification No. 22/2017, whereby notification No. 13/2017 was amended