Reema Sondhi

In my previous article, I had discussed on how to determine Point in time when GST shall apply. Now the next & the most significant question is how to determine the PLACE where the Supply is being made i.e. which place shall be assumed to be the location of supplier of Goods or Services and what place shall be assumed to be the location of the Recipient of goods or Services.

This shall be answered by Place of Provision of Supply Rules, precisely this will be the determinant of whether a transaction is Inter or Intra State.

Thus a detailed analysis needs to be done for what will be the Location of Supplier & Place of Supply as per Draft GST Law.As per proposed IGST Law, the place of supply has been specifically given for various scenarios for both goods & Services.

Below are the simplified representations of these scenarios:

LOCATION OF SUPPLIER OF GOODS

Location of Supplier of goods has not been specifically defined in the proposed law. It is only the location of supplier of services which has been defined. However a general interpretation would be the principal place of the registration of the supplier or his fixed establishment of business.

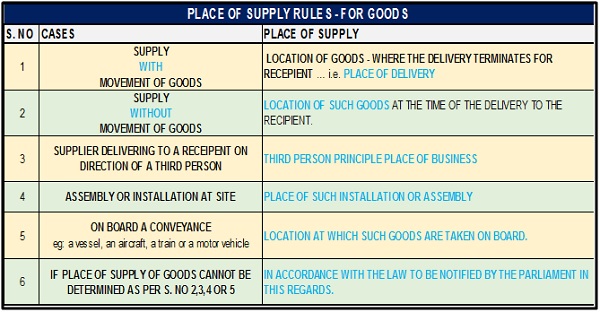

PLACE OF SUPPLY FOR GOODS

LOCATION OF SUPPLIER OF SERVICES

General Rule -The principal place of business for which registration has been obtained, however if the delivery is made from any other place than the principal place of registration, then place of such fixed establishment from where the delivery is made. If delivery is made from more than one fixed establishment, then the establishment from which the most direct provision of such services is provided.

In absence of above such places, the principle place of business shall be his usual place of residence.

PLACE OF SUPPLY FOR SERVICES – General Rule

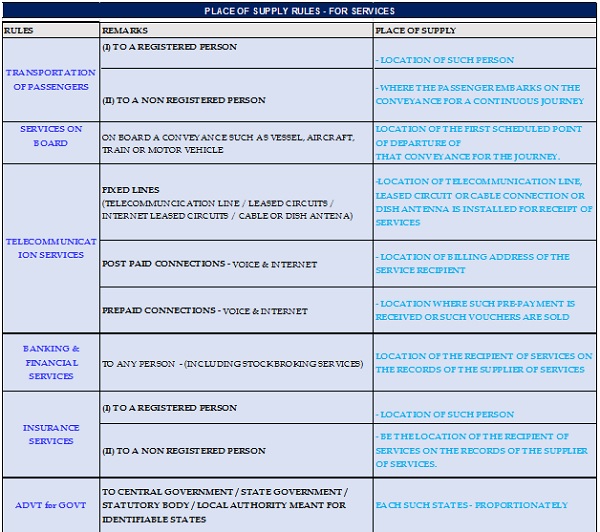

PLACE OF SUPPLY FOR SERVICES – Specific Rule’s

Conclusion:

Hence first we need to determine the location of the Location of Supplier and the place of Supply as per GST Law.

In case both of them are in the same state the transaction will be one of INTRA STATE & only CGST & SGST shall apply on such transactions.Whereas once the location of supplier and the place of supply as per GST Law is not in the same state the transaction is that of INTER STATE & IGST comes into picture.

Further, a worthwhile point to note here is that – In case cumulative of CGST+SGST is not the same as IGST, there is still a possibility of arbitration left over with traders. They may register into various states & take the benefit of difference in tax rate to bill the consumer. Hence leaving a loop hole &evasion tax base for government & tax saving for the trader.

Note: – Reliance & reference has been made on Draft GST / IGST Law, the contents are subject to change upon the release of the Final draft of Model GST Law.