Reasons and Logic behind not extending the GST Returns due date but giving exemption from payment of Late Fee and Interest for February, March and April 2020 due to COVID-19 pandemic

Whenever there are exceptional situations, the return filing due dates will be extended which we have seen many times in GST era also. Presently tax payers in India are facing unprecedented situation due to COVID-19 pandemic and aftermath lock down. To give relief to the tax payers, Finance Minister announced in a press conference various relief measures. One of the relief measures is giving exemption from payment of late fee and interest on filing GST Returns for the 3 months. Every one presumed that the due dates for the 3 months are extended up to the end of June 2020.

After press meet, GST Notifications 31 & 32 are issued on 03-04-2020. To every one’s surprise, the return filing due dates are not extended, but only they provided exemption for payment of late fee and interest on one condition that the returns should be filed in the last week of June, 2020. If returns are not filed after that date, the late fee & interest exemption is not applicable.

The question here is what is the logic or reason behind not extending the due dates but only giving the exemption from payment of late fee & interest. The simple logic is that, there might be many consequences for not filing returns within due date but Government wants to give relief for the 2 consequences only i.e., late fee & interest.

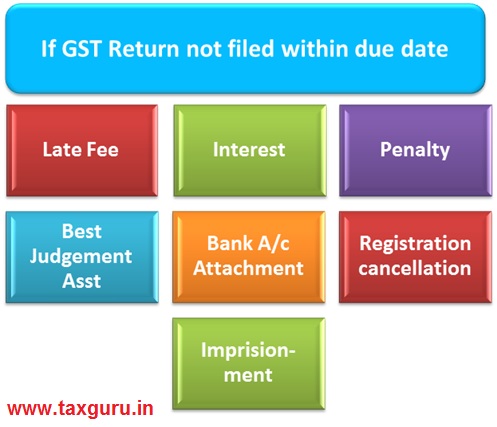

So what are the other consequences of not filing the GST Returns within the due date?

In the given table, some major consequences are listed:-

|

Consequences (other than late fee and interest) in case GST Returns are not filed within due date |

|

| Consequences | Remarks |

| Penalty | Maximum of 100% of tax or Rs.10000/- if taxes not paid within 3 months in some cases |

| Best Judgment Assessment |

|

| Bank Account Attachment | Bank Account can be attached before or after issue of assessment order |

| Cancellation of Registration | If GST Return not filed for 6 months consecutively |

| Imprisonment | If tax default is Rs.100.00 crore or more |

| Rating | The rating of the taxpayer may be affected |

So to avoid the above consequences, the tax payers may file the returns in case the situation allows them to do the same.

The extended due dates or specified dates for the purpose of exemption from payment of late fee and interest is given in the below table:

| Notification No. 32/2020 – Central Tax (for waiver of late fee) | ||||

| Notification No. 31/2020 – Central Tax (for waiver of interest) | ||||

| Form No. | Tax Payers Criteria | Tax period | Late Fee &

Interest |

Specified Date |

| GSTR-3B | TO > 5 Cr. in prev. FY | Feb, Mar & Apr 20 | Nil / 9%

(see note1) |

24-06-20 |

| 1.5 Cr < TO <= 5 Cr. in prev. FY | Feb & Mar 20 | Nil | 29-06-20 | |

| Apr 20 | Nil | 30-06-20 | ||

| TO <=1.5Cr in prev. FY | Feb 20 | Nil | 30-06-20 | |

| Mar 20 | Nil | 03-07-20 | ||

| Apr 20 | Nil | 06-07-20 | ||

Note 1: For tax payers having turnover of more than 5 Cr. complete waiver of late fee is given if the return is filed on or before the specified date. However in the case of interest full waiver is given if the return is filed on or before 15 days from the due date of filing return. Beyond 15 days 18% (CGST 9% + SGST 9%) is applicable

Can we file return within specified date ?

Can Mar GSTR3B be filed in the month of june ?

Please clarify

Good analysis. Expecting more articles from Tiruvai garu