REFUND OF ITC PAID UNDER EXPORT OF GOODS / SERVICES WITHOUT PAYMENT OF IGST

This article clearly explains, how to fill and submit Refund Application for claiming REFUND unutilised ITC against Export of Goods/Services without payment of IGST (means, Sales against LUT)

Path: Click on Services menu ——> Refunds ——> Application for Refund — > Fill Up Refund of ITC on Export of Goods & Services without Payment of Integrated Tax

—–Select Refund period ( you can Select single or multiple months)

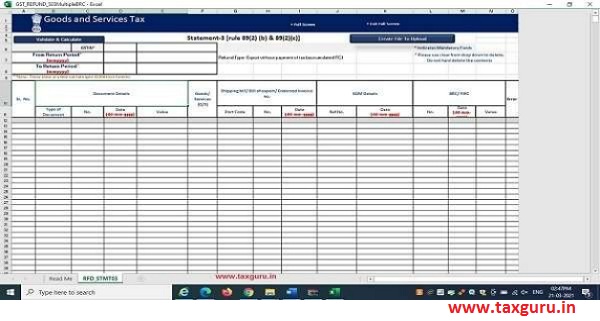

Download Statement Statement 3 under rule 89(2) (b) and 89(2)(c)

Statement 3 are preparing as per rule 89(2)(b) and 89(2)(c) of CGST Rules, 2017.

Following are the important details it has to be mentioned compulsory in the statement 3 at the time of creation of Json filed of statement 3.

(1) GSTIN Number

(2) Return Period: From Return period —— To Return period

(3) Type of Document/ Invoice No/Date of Invoice and Total Value of Invoices mentioned in the statement 3 form at the time of filing

It has to verify that the figure which you are mentioned in the Statement 3 it should be matched with your filed GSTR 1 for that period.

(4) Refund application file for Export of Goods or Services are select as per the application

(5) Shipping Bill/Bill of Export/Endorsement invoices–àPort Code, Shipping Bill No, Shipping bill date is compulsory mentioned if you are file refund application for export of

(6) EGM details: EGM Number and EGM date are mandatory to mentioned at the time of filing of Refund

It has to be verified with the company ICEGATE IGST Validation details regarding every shipping bills issued by the custom portal against which EGM is filed by the CHA Agent or not. If EGM has not been filed against the invoices than that invoice shall not be consider for calculation of refund claim.

(7) BRC/FIRCis require at the time of filing of Refund application of Export of

Once all data is filed up in statement 3 after that click on Validate & calculate button and creation of Json file. File of Json uploaded on the online portal and validate.

After uploading JSON file on online GST portal, portal has verified all the data with the filed GSTR 1 for that relevant period. All data available in creation of json file should be matched with the filed GSTR 1. If any mismatch of data between creation of Json file and filed GSTR 1 in such a case portal has showing the Download Invalid Invoices which are not matched as per the filed GSTR 1 vs JSON File.

If all the data mentioned in the filed GSTR 1 vs JSON file are matched in a case portal showing Download all valid Invoices. All data are matched with the relevant period than portal is allowed us to fill up the data of Taxable Turnover of Zero rate supply of goods and services. Taxable Turnover of zero rated supply of goods and services should be matched with the total of turnover mentioned in JSON file.

HOW TO FILL FORM NO 3A ?

Statement- 3A [rule 89(4)]

Refund Type: Export without payment of tax (accumulated ITC) – calculation of refund amount

| Turnover of zero rated supply of goods and services ** | Net input tax credit ## | Adjusted total turnover ### | Refund amount (1×2÷3) *** |

| 1 | 2 | 3 | 4 |

**Here put Export Tunrover of Goods/Services against LUT for the refund period (as declared in GSTR1)

**If Export of goods ,the calculation for Zero Rated Turnover is 1.5 times of Local Sales or Export Turnover, whichever is less (As per CBIC Notification 16/2020)

## Here system will show the ITC Value shown in GSTR3B. You can edit the same to ELIGIBLE value. ITC against Capital goods if any should be excluded from this value ### This column to be filled with most care. For detailed knowledge, please read the notes given at the bottom of this article.

*** This column is automatically filled by the system, based on the formula given in the column. You can edit the column to lower amount

The next step is to put the Refund amount CLAIMED against each tax (IGST/CGST/SGST)

| Amount eligible for Refund (in ) | |||

| BALANCE ITC AS ON REFUND PERIOD END | BALANCE ITC AS ON APPLICATION DATE | REFUND TO BE CLAIMED | |

| IGST | |||

| CGST | |||

| SGST | |||

| CESS | |||

| Total | |||

The Lower amount of comparison of all 3 should be eligible for taking Refund Amount.

The Value which was derived as per statement of 3 are compared with Balance available in Electronic Credit Ledger and Tax credit availed during the period. Once comparison was complete than lowest refund amount would be eligible for Refund.

Value as per Statement 3: calculation already made in above

Balance in Electronic Credit ledger: Balance which is available in electronic ledger credit account at the time of submission of Refund Application form.

Tax Credit availed during the period: If we apply for refund claim file for the month of APRIL 2020 then total credit availed during that month should be taken.

Documents are submitted at the time of online filing of manual refund claim?

Ans: Following Documents are required to be attached at the time of filing of Online Manual Refund Claim of Export of Goods without payment of IGST

a. Declaration under the 2ndproviso to section 54(3) export of goods is not subject to export

b. Declaration under the 3rdproviso to section 54(3) no drawback in respect of central tax has been claimed/shall be claimed or no refund of IGST paid on supplies has been

c. Declaration under section 54(3) declares ITC availed on the goods or services used for making “Nil” rated/ exempted supplies has not been included in the refund of ITC

d. Declaration related to claimants have not contravened to Rule 91(1) and incidence of tax has not passed to any other person as per rule 89(2)(1).

e. Annexures B (Details of ITC Claimed with HSN code)

f. Copy of GSTR 2A for the relevant

g. Bank Realisation Certificates (BRC) against all Export of goods/service from Bank

h. Copies of GSTR1 and GSTR3b for the Refund period

Total documents can be uploaded is 10 (5mb each)

Meaning of Taxable Turnover of Zero-rated supply of goods or services.

Turnover of zero-rated supply of goods means the value of zero rated supply of goods made during the relevant period without payment of tax under bond or Letter of Undertaking .

At the time of calculating Taxable Turnover of zero-rated supply of goods – goods which were sold under rebate claim (Goods sold under payment of IGST) are to be excluded from the total turnover of goods.

Goods are sold with payment of IGST in such a case not needed of filing of Refund application separately.

Net Input Tax Credit: Input tax credit available during the month. (credit which were availed during the relevant period are to be considered). Input Tax credit of IGST, CGST, SGST are availed during the relevant period are separately disclosed.

Adjusted total Turnover: Adjusted total turnover inclusive of Domestic Turnover + Zero rated supply (Export Turnover) – exempt supplies. It means the sum total of the value of (a) the turnover in a State or a Union territory, as defined Section 2(112) excludes the turnover of Services and (b) the turnover of a zero rated supply of services as per rule 89(4)(d) of CGST Rules, 2017 and non zero rated supply of services.

Excluding: (i) the value of exempt supplies other than zero rated supplies and

(ii) the turnover of supplies in respect of which refund is claimed under rule 4A and 4B.

As per CBIC Notification No 16/2020 Dtd 23/03/2020 ZERO RATED SUPPLY OF GOODS defined as under:

8. In the said rules, in rule 89, in sub rule (4), for clause (C), the following clause shall be substituted, namely:- „ (C) “Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking or the value which is 1.5 times the value of like goods domestically supplied by the same or, similarly placed, supplier, as declared by the supplier, whichever is less, other than the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both

***The above Notification is for export of goods and not for export of services

“Net ITC” means input tax credit availed on inputs and input services during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both;

*****

Article Prepared by: REJIMON P R, Tax Consultant, Cochin, Kerala. Email: etaxcochin@gmail.com

Author Bio

Dear Sir,

please POST one article on CSB-V.