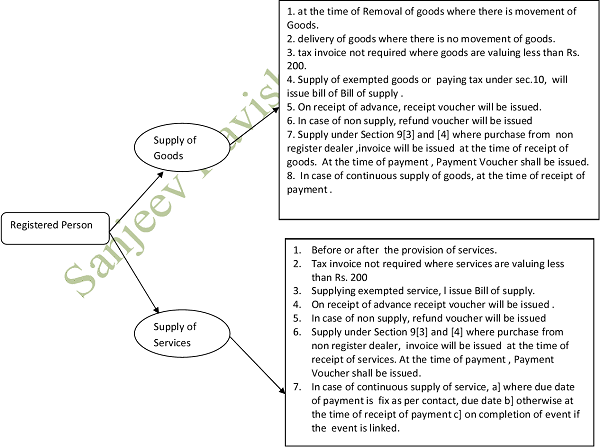

Invoice is basic document for supply of goods or service. There are circumstances where Taxable Invoice need not be raised only Bill of Supply will be issued .what are circumstances where Taxable Invoice as well as Bill of supply need not be raised and instead Delivery Challan will be sufficient. Where there is difference in price downward and upward one need to issue supplementary invoice / debit note or credit note. What are the circumstance where revised invoice will be issued. Let us discuss one by one and focus on Section 31 to 34 of the GST Act ,2017 and Invoice Rule of the same.

Issue of tax Invoice and Bill of Supply

Information Required to be Inserted in Tax Invoice/ Bill of Supply/ Revised Invoice/ Supplementary Invoice/ Debit or Credit Notes/ receipt Voucher

| Requirement | Tax Invoice | Bill of Supply | Supplementary/ Revised Invoice

Debit & Credit Note |

Receipt Voucher |

| 1. Name ,Address and GSTIN of supplier |

Y |

Y |

Y |

Y |

| 2. Serial Number | Y | Y | Y | Y |

| 3. Date of issue | Y | Y | Y | Y |

| 4. Name ,Address and GSTIN or UIN of recipient if register | Y | Y | Y | Y |

| 5. Name ,Address of recipient & address of delivery with name and code of state if recipient is unregistered where the value of taxable supply is Rs.50000 or more. | Y | N | Y | Y

|

| 6. HSN Code or SAC | Y | Y | N | N |

| 7. Description of Goods and Services | Y | Y | N | Y |

| 8. Quantity in case of goods & unit or unique Quantity code | Y | N | N | N |

| 9. Total value of Goods or Services or both | Y | Y | N | N |

| 10. Taxable value of Goods or services after discount | Y | N | Y | Y |

| 11. Rate of tax | Y | N | N | Y |

| 12. Amount of tax | Y | N | N | Y |

| 13. Place of supply with name of State in case of Inter state supply. | Y | N | N | Y |

| 14. Address of delivery if the same is different from place of supply | Y | N | N | N |

| 15. Whether the tax is payable on reverse charge basis | Y | N | N | Y |

| 16. Signature or Digital Signature | Y | Y | Y | Y |

Note :

1. In case of revised invoice the word “Revised Invoice” must be written prominently. Corresponding Invoice no. or Bill of supply must be mentioned on the revised invoice/ debit note or credit note in addition to the above informations..

2. In case of receipt voucher , amount of advance taken must be inserted in addition to the above information.

3. Every register person who has been granted registration after the date of effective liability, has to issue revise invoice from the effective date of liability to date of certificate of registration. Provided that RP may issue consolidated invoice for supply to non registered person.

4. In case of Input service distributor the following details to be inserted :

⇒ Name address and GSTIN of input service distributor

⇒ Serial number

⇒ Date of issue

⇒ Name address and GSTIN of recipient

⇒ Amount of credit distributed

⇒ signature

where the ISD is bank , financial institution or NBFC , they can issue any document without any serial number but having all information mentioned above.

5. Where the supplier of goods is GTA supplying goods by road shall issue tax invoice or any other document containing the gross weight of the consignment, name of the consignor and consignee , registration number of goods carriage, detail of goods transported, place of origin and destination, GSTIN of person liable for paying tax consignor , consignee or GTA and also containing other information as per rule -1.

6. Where the supplier is passenger transportation , tax invoice shall include ticket in any form by what ever name called without any serial no. , without the address of recipient but include all information mentioned in rule-1.

7. Following are the cases where invoice is not mandatory

⇒ Supply of liquid gas where the quantity at the time of removal is not known

⇒ Transportation of goods for job work

⇒ Transportation of goods other than supply

Consignor may directly issue deliver challan serially no. but containing the following details.

⇒ Date and no. of delivery challan

⇒ Name , address and GSTIN of consignor , if registered

⇒ Name , address and GSTIN of consignee , if registered

⇒ HSN Code and description of goods

⇒ Quantity

⇒ Taxable value

⇒ Tax rate and amount

⇒ Place of supply in case of inter state.

⇒ signature

Delivery challan shall be prepared in triplicate 1. Consignor 2. Transporter 3. Consignee

Where the goods are transported on delivery challan in lieu of invoice , the same shall be declared in Form[ WAY BILL ]

In case of Export following additional details are required in lieu of details contain in point no. 5

1. Invoice carry an endorsement that “ Supply meant for Export on payment of IGST “ or “Supply meant for Export under Bond or letter of undertaking without the payment of IGST”

2. Name and address of recipient

3. Address of delivery

4. Name of the country of destination

5. Number and date of application for removal of goods for export

Time Limit for issue of tax Invoice for services

1. 30 days from the date of supply of services.

2. 45 days in case of banking company, financial institution and NBFC

Manner of issue of Invoice

1. Invoice of Goods in triplicate

2. Invoice of Services in duplicate

Disclaimer :

The contents of this article are solely for information and knowledge and does not constitute any professional advice or recommendation. Author does not accept any liability for any loss or damage of any kind arising out of this information set out in the article and any action taken based thereon.

Author Bio