Every registered person is required to maintain certain documents prescribed under GST law. Some of the important and common documents include tax invoices, bills of supply, debit and credit notes, receipt, payment and refund vouchers. The situations which warrant mandatory issuance of these documents are explained below;

- Tax Invoice – Any registered person, supplying taxable goods and/or services shall issue a Tax Invoice.

- Bill of supply – Any registered person, supplying exempted goods and/or services or paying tax under composition levy scheme shall issue a Bill of supply, instead of Tax Invoice.

- Receipt Voucher – A registered person is required to issue a Receipt Voucher on receipt of advance payment with respect to supply of goods and/or services.

- Refund Voucher – Where a registered person issues a Receipt Voucher on receipt of advance payment, but subsequently no supply is made and no Tax Invoice is issued, the registered person may issue a Refund Voucher to the person who had made the advance payment, against the

- Payment Voucher – A registered person, who is liable to pay tax under reverse charge basis, shall issue a Payment Voucher at the time of making payment to the supplier.

- Credit Note – Where a Tax Invoice is issued and the taxable value/tax charged in it is found to exceed the actual taxable value/tax payable, or where the goods supplied are returned by the recipient, or where goods and/or services supplied are found to be deficient, the registered person (supplier), shall issue a Credit Note to the recipient.

- Debit Note – Where a Tax Invoice has been issued and the taxable value/tax charged in it is found to be less than the actual taxable value/tax payable, the registered person shall issue a Debit Note to the recipient.

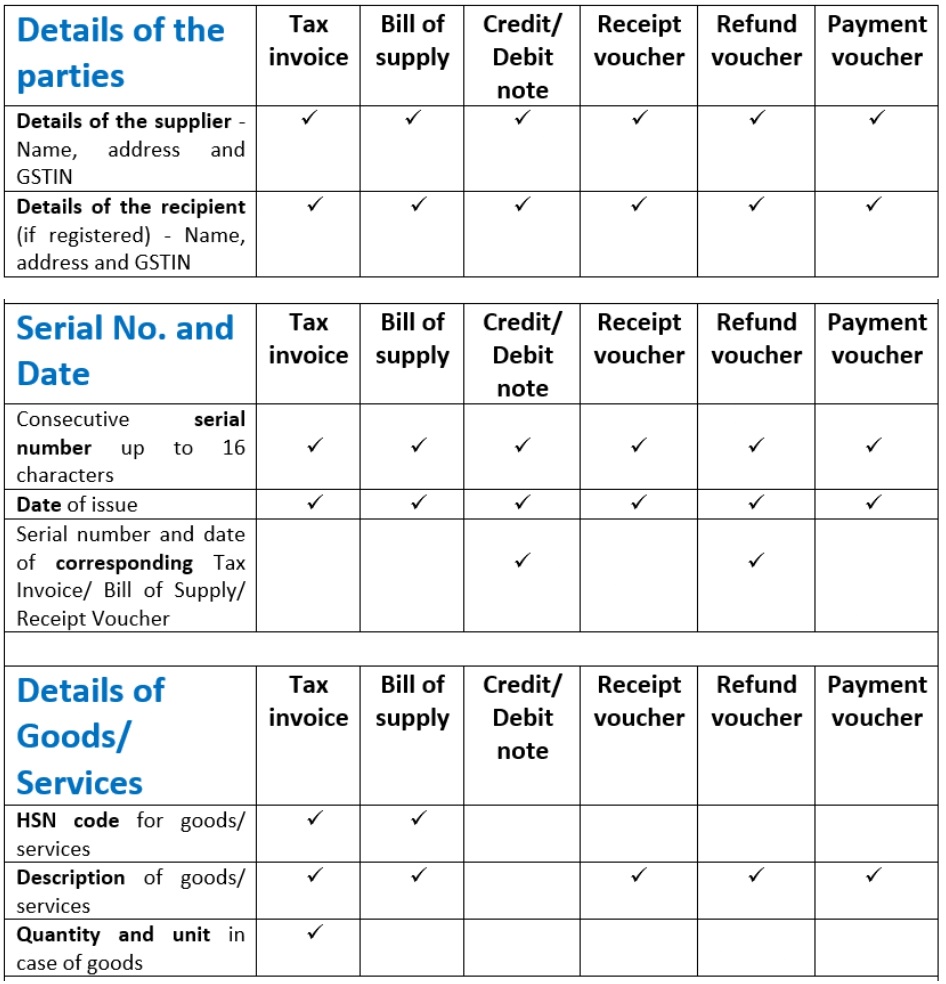

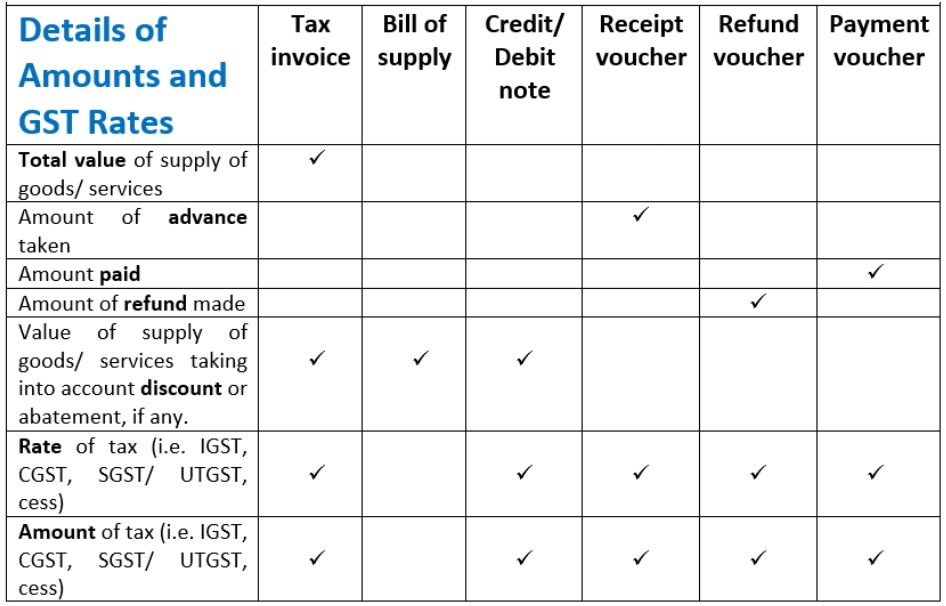

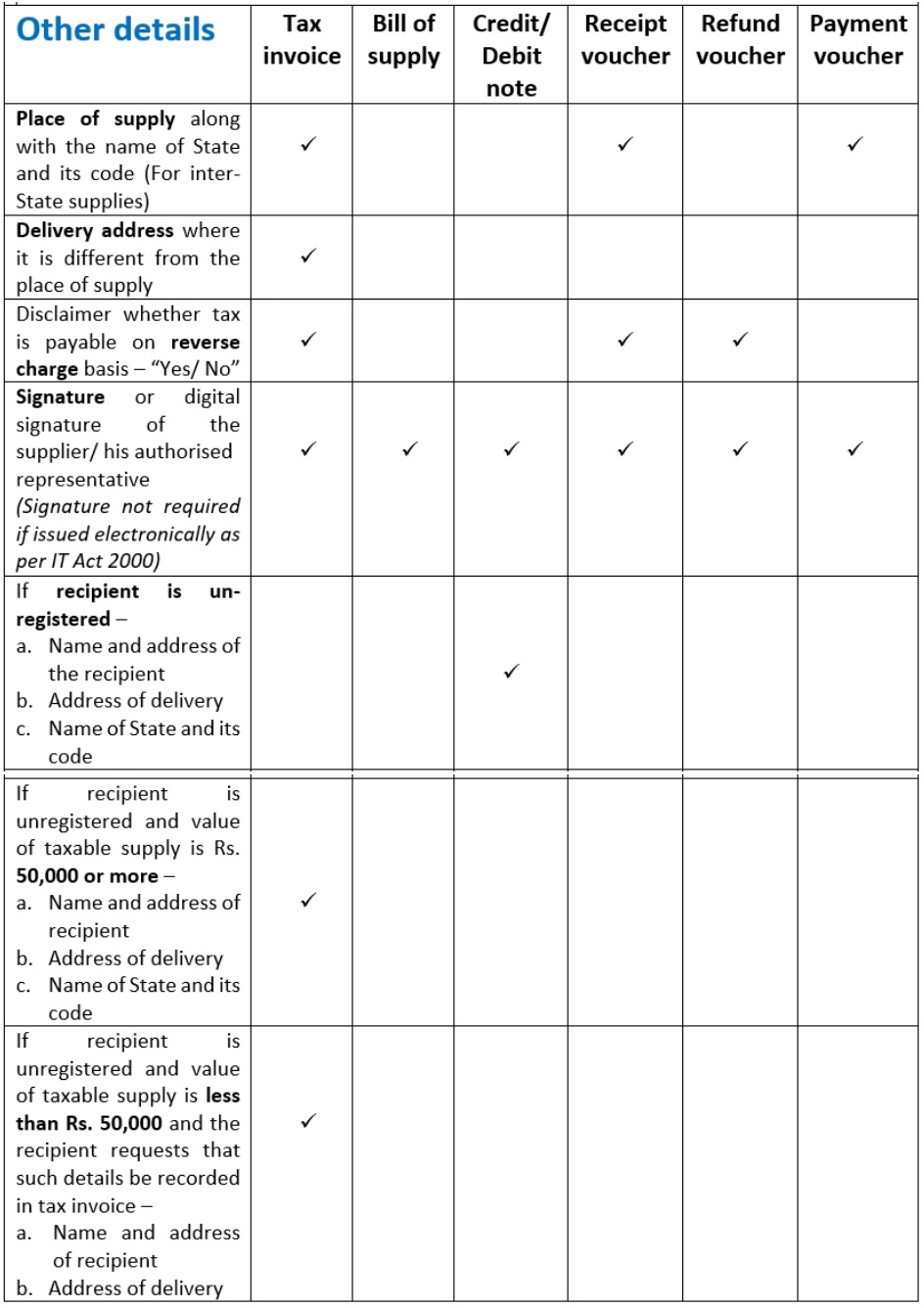

Mandatory details to be included in the aforementioned documents are summarised below;

This article is written by Dohit Muranjan, who is a Chartered Accountant and working as a Consultant at Aria CFO Services in Mumbai. Aria CFO Services provides professional services exclusively to NGOs and Social Enterprises across India. In case of any queries regarding this article, please feel free to reach out to Dohit on his email ID – dohit@ariaadvisory.in

DISCLAIMER: The basis of this work is the GST law in India as on the date of writing this article. The article is for informational purpose only and is solely aimed at providing the reader an insight to the common documents prescribed under GST law. No part of this article shall be construed as any kind of legal advice.

Author Bio