The CBIC & GSTN recently changed the GSTR3B format as below to align with Input Tax Credit (ITC) as per GSTR2B in line with Circular No: 170/02/2022-GST dated: 06.07.2022

As per the new changes, the recipient has to avail Input Tax Credit as per the GSTR2B data and reverse the ITC for the supplies which are not received by him / in transit.

Once the supplies are received, the recipient can reclaim the ITC already reversed in that particular month GSTR3B.

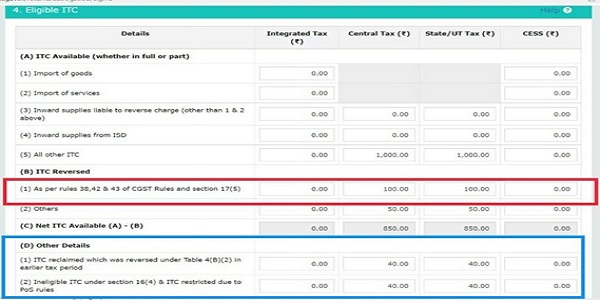

This shows that the GSTR2B ITC alone should be claimed in GSTR3B Table 4A and any reversals and reclaims has to be declared as adjustments in Table 4D.

It won’t surprise us if the GSTN disables editing of auto-populated values in Table 4A of GSTR3B in near future as we need to declare all additions and reductions in Table 4D only.

Now all these done to align GSTR3B with GSTR2B, the CBIC and Finance Ministry missed a big junk of issue with related to pending ITC as of July 31st.

Till July 31st assesses were claiming ITC as per their books as the GSTR2B will have only ITC related to filings happened during that particular month.

In a country like India where wider geographical area requires days / weeks to transport goods from one place to another obviously some of the ITC related to old months will be availed in the subsequent months only. Hence GSTN facilitated with editing of auto-populated data and claim ITC as per the books.

Now insisting to claim ITC only as per GSTR2B, which is the filing data pertaining to the particular month, the ITC related to old period has to be claimed in Table 4D as “reclaim of ITC already reversed”. But there is no ITC reversal done earlier for “reclaiming” now.

As there is no clarity given by the CBIC till date, there is only one procedure for assesses to adhere the new compliance as below:

> Avail ITC as per GSTR2B of August 2022 in Table 4A of GSTR3B

> Reverse all the ITC already availed for which supplies are not received / Vendor not filed their returns in Table 4(D)(2) of GSTR3B

> From September return onwards, reclaim the reversed ITC once the supplies are received / Vendor filed their returns in Table 4(D)(1) of GSTR3B

With the above procedure, the ITC as per GSTR2B alone will be reported in Table 4A of GSTR3B and adjustments like Reversals for Supplies not received & reclaim for supplied received against old reversal can be declared in Table 4D of GSTR3B

The above process is only to clarify the possible way of adhering the new requirement in GSTR3B without getting into litigation issues.

However, I suggest to wait for official clarification by CBIC with regard to old pending ITC and how it has to be claimed in GSTR3B of Aug 2022 returns.

Author Bio

The author may reply the brilliant critical observations of Raghul. It will help actual users of gst

This article is totally misguiding. Don’t go by this. Because, Table 4(D)(1) & (2) are only for reporting purposes and the amounts shown here won’t affect Electronic Credit Ledger.

Refer Circular No.170/02/2022 dt.06.07.2022

This article is *totally misguiding*. Don’t go by this. Because, Table 4(D)(1) & (2) are only for reporting purposes and the amounts shown here won’t affect Electronic Credit Ledger.

Refer Circular No.170/02/2022 dt.06.07.2022