Introductory View: The Goods and Services Tax Appellate Tribunal (GSTAT) serves as the second appellate authority under the GST framework. Filing an appeal before the GSTAT requires strict adherence to procedural and statutory guidelines to ensure admissibility.

Salient Features of GSTAT Appeals

Mandatory Electronic Filing: All appeals must be filed electronically on the official GSTAT portal via Form GST APL-05.

Limitation Period: The standard period for filing an appeal is three months from the date on which the order sought to be appealed against is communicated to the person preferring the appeal.

Automatic Stay: Upon payment of the mandatory pre-deposit, recovery proceedings for the balance of the disputed demand are automatically stayed under Section 112(9).

Pre-Deposit Requirement: To file an appeal, you must pay:

The full amount of tax, interest, fine, fee, and penalty arising from the impugned order, as admitted by you.

An additional 10% of the remaining disputed tax amount. (Note: This is in addition to the 10% paid at the first appeal stage, resulting in a cumulative 20% deposit).

Payment Mode: The pre-deposit must be made exclusively through the Electronic Cash Ledger. Payment via the Input Tax Credit (ITC) ledger is generally not permitted.

Restriction on Fresh Evidence: You are generally not permitted to produce additional evidence before the Tribunal that was not produced during the proceedings before the adjudicating or first appellate authority, unless specific exceptions are met (e.g., sufficient cause for non-production).

Summary of Pre-Deposit Calculation

| Component | Requirement |

| Admitted Liability | 100% of admitted tax, interest, penalty, etc. |

| Disputed Tax | 10% of the disputed tax amount (additional). |

| Penalty-Only Disputes | 10% of the disputed penalty amount. |

| Maximum Cap | ₹20 Crore (for CGST/SGST); ₹40 Crore (for IGST). |

Note: The total cumulative pre-deposit by the time you reach the GSTAT is 20% of the disputed tax.

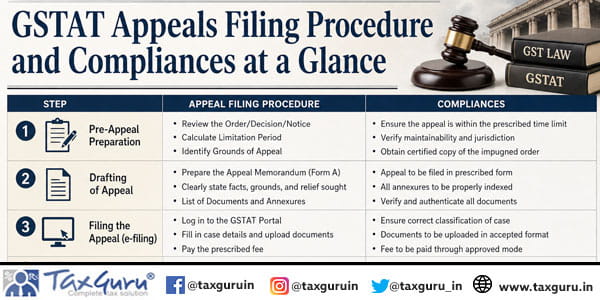

Step-by-Step Filing Procedure of GSTAT Appeals

Assess Merit: Evaluate whether the First Appellate Authority’s order warrants an appeal, preferably with legal counsel to review existing precedents.

Prepare Documentation: Ensure all mandatory documents (PDF format, less than 20 MB per file) are ready.

Payment: Calculate the pre-deposit and make the payment via the GST portal using the Electronic Cash Ledger. Ensure you have the challan details.

Portal Filing:

- Log in to the GSTAT e-filing portal.

- Navigate to the appeal section and initiate Form GST APL-05.

- Enter order details (Order-in-Appeal/Revision Number).

- Upload all required documents, including the Statement of Facts and Grounds of Appeal.

Digital Signature: Sign the application using a valid Digital Signature Certificate (DSC) or Aadhaar e-Sign.

Submission: Submit the form to receive a provisional acknowledgement. A final acknowledgement number is generated after the registry completes a preliminary scrutiny.

Essential Documentation for Checklist

Certified Copies: A certified copy of the Order-in-Appeal (OIA) being challenged and the original Order-in-Original (OIO).

Statement of Facts: A clear, chronological narrative of the case.

Grounds of Appeal: A concise, numbered list of legal and factual arguments.

Proofs of Payment: Copy of the pre-deposit challan.

Authorization: Board Resolution (for companies) or Vakalatnama (if represented by an advocate).

Verification: Duly signed verification document (Form APL-02A).

Crucial Compliance Tips

Defect Rectification: If the registry flags defects in your filing, you must rectify them within the stipulated timeframe (typically 30 days) to prevent the appeal from being rejected.

Clearance of Backlog: For orders issued before 1 April 2026, be mindful of any specific cut-off dates or staggered filing windows announced by the government to manage the transition to the new system.

Language: All documents must be in English. If a document is in a regional language, provide a certified English translation.

Separate Appeals: You must file a separate appeal for each Order-in-Original, even if they were combined in a single Order-in-Appeal. Joint appeals by multiple persons are not permitted.

Step by Step Filing of Adjournment Application and Written Submissions

Filing an adjournment application or submitting written documents before the Goods and Services Tax Appellate Tribunal (GSTAT) is governed by the GSTAT (Procedure) Rules, 2025. These rules emphasize procedural discipline to prevent the long delays seen in previous tax tribunals.

Adjournment Applications

The GSTAT has implemented a “strict adjournment” policy. You generally have a maximum of three adjournments available per party per case.

Procedure: File an Interlocutory Application (IA): You must file an IA using GSTAT Form-01 on the official GSTAT e-filing portal.

Grounds: The application must specify the “sufficient cause” for the request (e.g., medical emergency, non-availability of key documents, etc.). Vague reasons like “advocate is busy” are frequently rejected.

Submission: Ideally, file this well before the hearing date. If the urgency arises on the day of the hearing, the application must be resented to the Bench directly.

Objecting: The opposing party has the right to object to your request. The Tribunal will decide on the spot whether to grant it.

Fees & Costs:

Application Fee: There is typically a nominal fee for filing an Interlocutory Application (often ₹1,000 per application).

Adjournment Cost: Be aware that the Tribunal may impose a cost of ₹5,000 for each adjournment granted. This is a punitive measure meant to discourage frivolous requests. Non-payment of these costs can lead to the adjournment request being denied.

Important: Once you exhaust your three permitted adjournments, the Tribunal will proceed to hear the case on its merits, even if you are unprepared or absent (which may lead to an ex-parte order).

2. Filing Written Submissions

Written submissions are crucial for detailing complex legal arguments that may be difficult to convey fully during oral arguments.

Procedure:

Preparation: Your submission must be typed in double-space on A4 paper, strictly paginated, and indexed.

Digital Filing: Upload the final document to the GSTAT e-filing portal. Ensure it is in PDF format, properly bookmarked, and does not exceed the specified file size limits (usually 20 MB).

Advance Service: You are required to serve an advance copy of the written submission to the other party (the Department or the Taxpayer) and provide proof of such service if the Tribunal requires it.

Timing: Ideally, these should be filed before the final hearing.

If the Bench grants permission during the hearing, you may file supplementary written submissions within the timeframe specified by the Presiding Member (often 7–15 days).

Format Requirements:

Conciseness: Keep it focused on the disputed points of law or fact.

Structure: Use consecutively numbered paragraphs.

Evidence: Reference the documents already on record. Do not introduce “fresh evidence” in a written submission unless the Tribunal has specifically granted leave to do so.

Summary Table: Fees & Forms

| Action | Form | Typical Fee |

| Adjournment Application | IA (Form-01) | ₹1,000 (Filing Fee) + up to ₹5,000 (Potential Cost) |

| Written Submissions | N/A (Uploaded) | No separate filing fee |

| Rectification Application | IA | ₹500 |

| Restoration Application | IA | ₹5,000 |

Quick Tips for Compliance

Track Your Limits: Check the “My Cases” section on the GSTAT portal to monitor your remaining adjournment count.

Electronic Payment: All fees (application fees or costs imposed) must be paid online, typically via Bharatkosh or the integrated payment gateway on the GSTAT portal. Keep transaction IDs ready for reference.

Avoid “Fresh” Arguments: Written submissions are meant to clarify and summarize, not to introduce entirely new grounds of appeal. Ensure your core legal arguments are already present in your original Form APL-05.

Author Bio