Articles by this Author

Corporate Law

Corporate Law

All About Principles of Natural Justice

Income Tax

Income Tax

Survey and Assessment Proceedings under New Income Tax Act, 2025

Income Tax

Income Tax

Search & Seizure Procedures under New Income Tax Act, 2025

Goods and Services Tax

Goods and Services Tax

E- Way Bill Big Changes Applicable from 15.06.2026

Income Tax

Income Tax

ITR-1 & ITR-4: Income, Assets and Transactions That Can Never Be Reported

Income Tax

Income Tax

All About Exempted Income and Deductions under New Income Tax Act, 2025

Income Tax

Income Tax

Segregation & Aggregation of Income Under Income Tax Acts 1961 & 2025

Income Tax

Income Tax

Presumptive Taxation Simplified as Income Tax Act 2025 Merges 44AD, 44ADA & 44AE

Goods and Services Tax

Goods and Services Tax

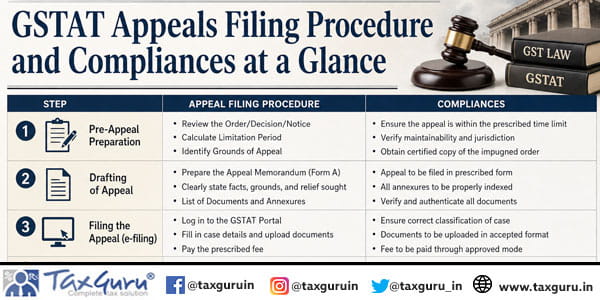

GSTAT Appeals Filing Procedure and Compliances at a Glance

Income Tax

Income Tax

Comparison Between 1961 and 2025 Income Tax Acts with Bollywood Songs

Income Tax

Income Tax

Section 54 Exemption not eligible on Sale of Open Land Without Building: ITAT Allahabad

Income Tax

Income Tax

Tax Treatment Under Section 10(23C)(iiiad) and Section 332 (RNPO)

Income Tax

Income Tax