Case Law Details

In re Clad Weld Technologies Pvt. Ltd. (GST AAR Gujarat)

Question: Whether supply to be made by the applicant of Wear Plates and Tamping Tools as manufactured specifically as per RDSO Drawing, directly to the Railway Authorities as per the Order received from M/s Trio Enterprise, should fall under HSN 86040000 & classified under Chapter 86 and should be taxed GST @ 5%?

Answer: No. The products, “Wear plates” and “Tamping Tool” manufactured specifically as per RDSO Drawing and supplied to the Railways through M/s Trio Enterprise, being a parts of a self-propelled track maintenance vehicles (viz. the Ballast Cleaning Machine & the Tie Tamping Machine), are classifiable under chapter sub-heading 860799 (Other Parts of railway or tramway locomotives or rolling stock), and, hence, same would attract GST @ 5% under S. No. 241 of the Schedule I till 30.09.2019 and w. e. f. 01.10.2019, @12% under S. No.205G of the Schedule-II to the Notification No.01/2017- Central Tax (Rate) dated 28.06.2017, as amended.

FULL TEXT OF ORDER OF AUTHORITY OF ADVANCE RULING, GUJARAT

The applicant, vide their application for Advance Ruling, has submitted that they are having factory at Survey No. 428/1, Village-Nana Fofalia, Dabhol, Vadodara, Gujarat-391210 engaged in the manufacture of Wear plats & Tampering tools specially manufactured as per RDSO specifications and used by Railways as a part of Ballast Cleaning Machine and Tie Tamping Machine.

2. The applicant further submitted that M/s Trio Enterprise having GSTIN: 24AFRPS0617P1ZU has got orders from Indian Railways to supply Wear plats & Tampering tools and the same order is given by M/s Trio Enterprise to the applicant as back to back order. Here, the applicant is instructed to manufacture wear plates and tamping tools as per RDSO drawing No. mentioned in the Work Order as given by M/s Trio Enterprise, for South Eastern Railway and also instructed to deliver the same to them.

2.1 In view of above backdrops, the applicant has put forward his question on which advance ruling is required, as under:

“Whether supply to be made by the applicant of Wear Plates and Tamping Tools as manufactured specifically as per RDSO Drawing directly to the Railway Authorities as per the Order received from M/s Trio Enterprise, should be fall under HSN 86040000 & classified under Chapter 86 and should be taxed GST @ 5%?”

3. Statement containing the applicant’s interpretation of law and/or fact:

3.1 The applicant submitted that they are involved in the manufacturing of Wear plats & Tampering tools specifically manufactured as per RDSO specifications and used by Railways as a part of Ballast Cleaning Machine and Tie Tamping Machine.

3.2 Wear Plates used in Ballast Cleaning Machine: Considering the vertical thrust coming on railway track, the track is required to be cushioned with specific size of ballast (Grit/ Kapachi) to transfer the vertical thrust to the soil. During working over the period of time, this ballast becomes rigid due to accumulation of fine dust, mud and sand particles and creating hurdles to maintain track up to the standard with use of track tampers, thus requires periodic cleaning and screening. Ballast Cleaning Machine is an important Track Maintenance Vehicle used to clean ballast. Ballast below track is removed by cutter bar and conveyed up to screens thru TURF (Red arrow marked line shows the movement of ballast) by chain. The TURF is lined with various wear plates as per machine design and due to continuous friction between ballast, wear plates and chain, the wear plates get wear out during working which needs to be replaced time to time to protect basic body of machine. As the machine cannot work without wear plates and BCM machine is a very important self-propelled track maintenance vehicle, wear plates of BCM should fall under HSN code 86040000 as a part of track maintenance vehicle.

3.3 Tamping Tool used in Tie Tamping Machine: Railway track is cushioned with ballast to absorb the vertical thrust generated by the train running on it with high speed. Due to continue jerks and vibration, it gets loose and unorganized which is required to be tamped time to time. Tie Tamping Machine is another self-propelled track maintenance vehicle which does ballast tamping work and Tamping Tools is the key component of machine which get wear out after few days of working due to friction between ballast and tools. These tools required being replaced time to time to keep the machine and in turn the railway track working. As tamping tool is important part of this self-propelled track maintenance vehicle, it should fall under HSN code 86040000.

3.4 The applicant submitted the extracts of Chapter 86 and HSN-8604 00 00, as under:

“Chapter 86: Railway or tramway locomotives, rolling-stock and parts thereof; railway or tramway track fixtures and fittings and parts thereof; mechanical (including electromechanical) traffic signalling equipment of all kinds HSN-8604 00 00: Railway or Tramway Maintenance or Service Vehicles whether or not Self Propelled (For Example, Workshops, Cranes, Ballast Tampers, Track Liners, Testing Coaches and Track Inspection Vehicles)”

3.5 From above, it is very clear that both the items, i.e. Wear Plates and Tamping Tools are specifically manufactured for and used by Railways and should fall under Chapter 86.

3.6 The applicant has lastly submitted that as the order is given by M/s Trio Enterprise to the applicant on back to back basis and also supply is to be made by the applicant directly to the Railways only. To justify the same, they have attached the copy of the Work Order as received by M/s Trio Enterprise from Railways and the copy of the Work Order as issued by M/s Trio Enterprise to the Applicant.

4. At the time of personal hearing held through Video Conferencing on 09.07.2020, the Authorised Representative of the applicant, CA Rachit Shah, reiterated the facts as stated in the Application.

5. The applicant, vide their letter dated 11.07.2020 stated that during the last hearing conducted on 09-07-2020 through Whatsapp calling in which they have been asked to provide various details and photographs of the product specific along with the RDSO drawings on the basis of which the said products are manufactured and the justification regarding usage of the product is only limited to Railways only. Accordingly, their further submission is as below:

PHOTOGRAPHS OF THE PRODUCTS:

A. TAMPING TOOL – USED IN TIE TAMPING MACHINE:

6. Railway track is cushioned with ballast to absorb the vertical thrust generated by train running on it with high speed. Due to continue jerks and vibrations it gets loose and unorganized which is required to be tamped time to time. Tie tamping machine is another self-propelled track maintenance vehicle which does ballast tamping work and Tamping Tools (As shown in figure) is the key component of the machine which gets wear out after few days of working due to friction between ballast and tools. These tools required being replaced time to time to keep the machine and in turn the railway track working. As tamping tool is an important part of this self-propelled track maintenance vehicle, it should fall under HSN code 86040000.

6.1 PHOTOGRAPH OF TAMPING TOOL:

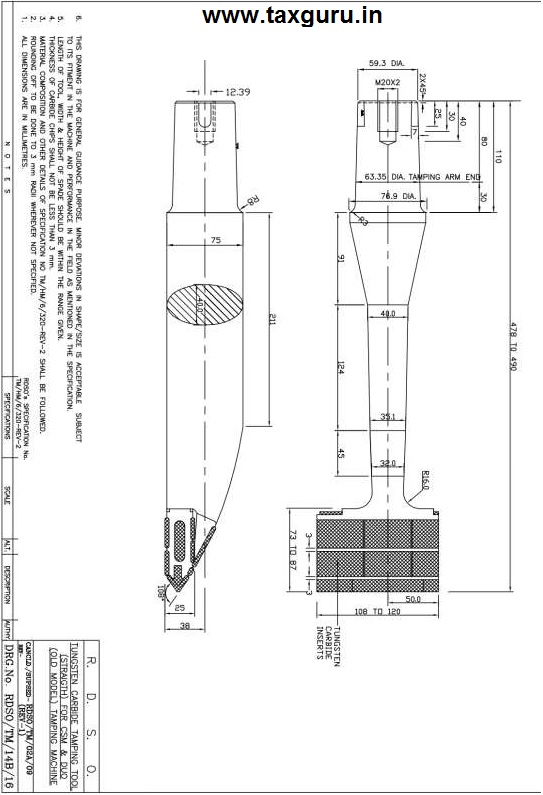

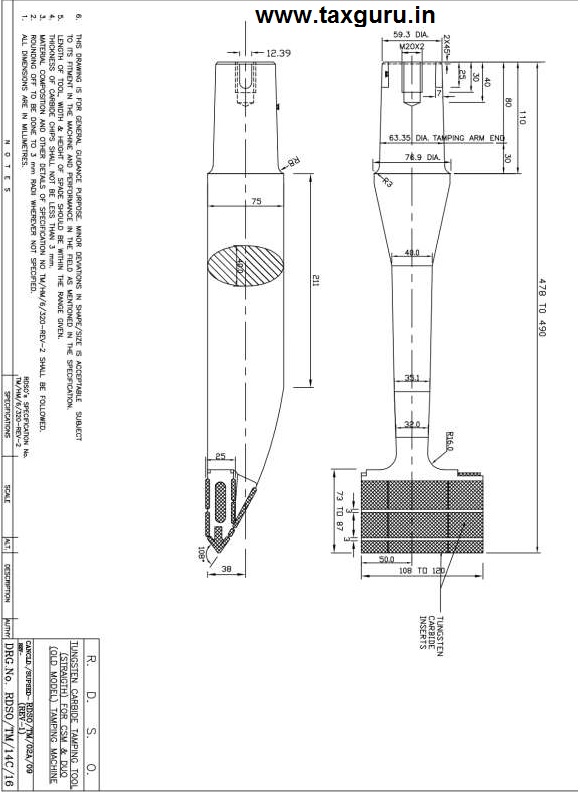

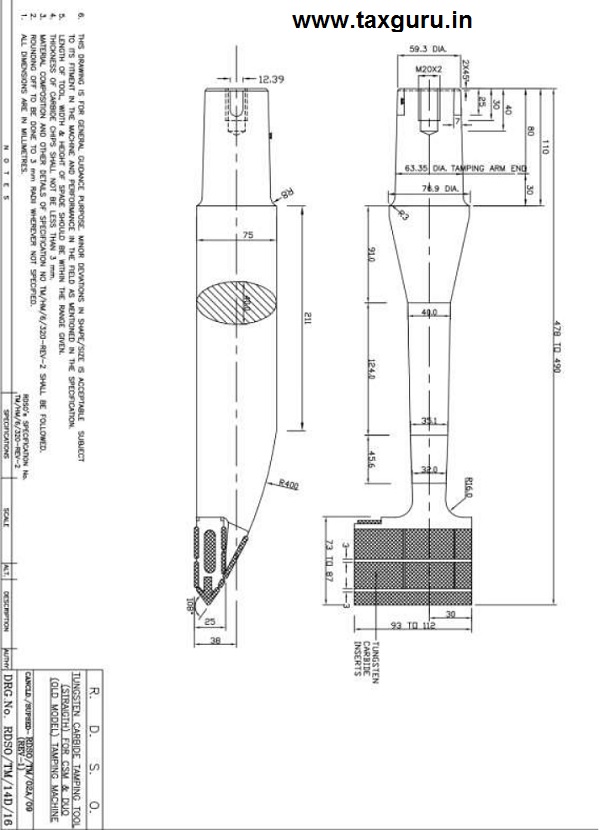

6.2 RDSO DRAWINGS ON THE BASIS OF WHICH THE SAID TAMPING TOOLS ARE MANUFACTURED:

Trio Enterprise (Main Contractor) has received Purchase order from South Eastern Railway by PO NO. XEN/Spare/LP/SNY/18-19/2575, dated 2210-2018 for supply of Tamping Tools as per RDSO Drawings mentioned in it. Against which Trio Enterprise has given BACK TO BACK order to CLAD WELD TECHNOLOGIES PVT LTD. To manufacture Tamping Tools as per the said mentioned RDSO drawing Numbers as given by South Eastern Railway by mentioning the said RDSO drawing numbers in the work order given to Clad Weld Technologies Pvt Ltd. by PO No.02/18-19, dated 22-10-2018. The copies of both the work orders have already been furnished to you in their earlier submissions. So, the RDSO drawing numbers can be easily identified from it.

6.2.1 Now, with this they have attached RDSO Drawings as required by the authorities. There are 4 RDSO drawing as mentioned in the work order which are as under:

1. RDSO Drawing No. RDSO/TM/14A/16.

2. RDSO Drawing No. RDSO/TM/14B/16.

3. RDSO Drawing No. RDSO/TM/14C/16.

4. RDSO Drawing No. RDSO/TM/14D/16.

6.2.2 All the drawings are attached herewith. The RDSO Drawing No. is mentioned at the bottom of the right side of the drawing.

6.2.3 PHOTO GRAPH OF TIE TAMPING MACHINE – WHERE TAMPING TOOL IS

FIXED AS MARKED BY RED COLOUR IN THE PHOTO GRAPH:

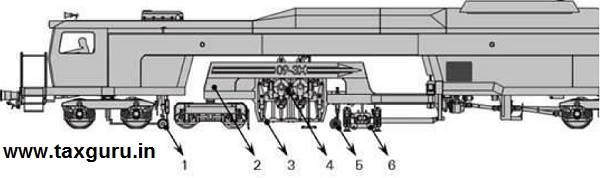

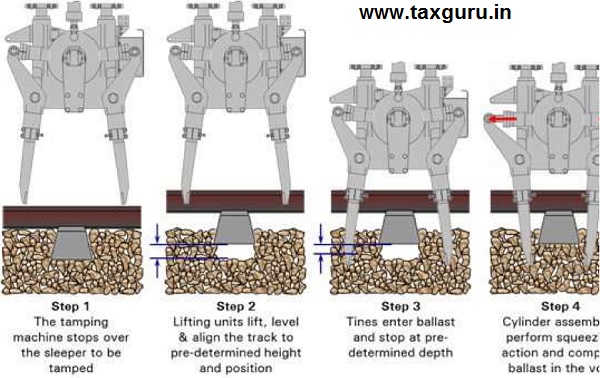

6.2.4 BASIC TAMPING PROCESS:

The most important working components of a tamping machine are shown in Figure 1, which are as below:

1 – Rear Measuring Trolley; 2 – Satellite (Continuous Action)

3 – Tamping Unit Frame; 4 – Tamping Unit/s;

5 – Centre Measuring Trolley; 6 – Lifting and Lining Unit;

7 – Front Measuring Trolley.

Figure 1: Working Components of Tamping Machine (09-3X Continuous Action Tamping Machine illustrated)

Figure 2: provides a schematic illustration of the tamping process in 4 simplified steps.

Step 1 – A basic tamping machine indexes forward and comes to a standstill with the tamping tines of the tamping unit straddling the sleeper to be tamped on both sides.

Step 2 – The lifting and aligning unit works in conjunction with the measuring system and grips the rail under the crown, lifts the track to a predetermined height while correcting any vertical alignment defects in the track and at the same time slews the track to correct the horizontal alignment (simultaneous levelling and aligning).

Step 3 – The tamping units are lowered. The vibrating tines/tamping tools enter the ballast and stop at a pre-determined depth. The tines/tamping tools are vibrating in order to fluidise the ballast stone to permit it to re-arrange and settle in a dense matrix. Controlled vibration greatly reduces the force required to penetrate the tamping tines/ tamping tools into the ballast without damaging or crushing the ballast stone.

Step 4 – The cylinder assembly exerts a force on the tine arms which perform a squeezing motion of the tines. The taming tools compact ballast underneath the sleeper in the void created by the lifting process. The tamping machine indexes forward to the next sleeper and the process repeats itself. Behind the tamping machine the track is left at the required geometric standard on a homogeneous ballast bed with restored elasticity.

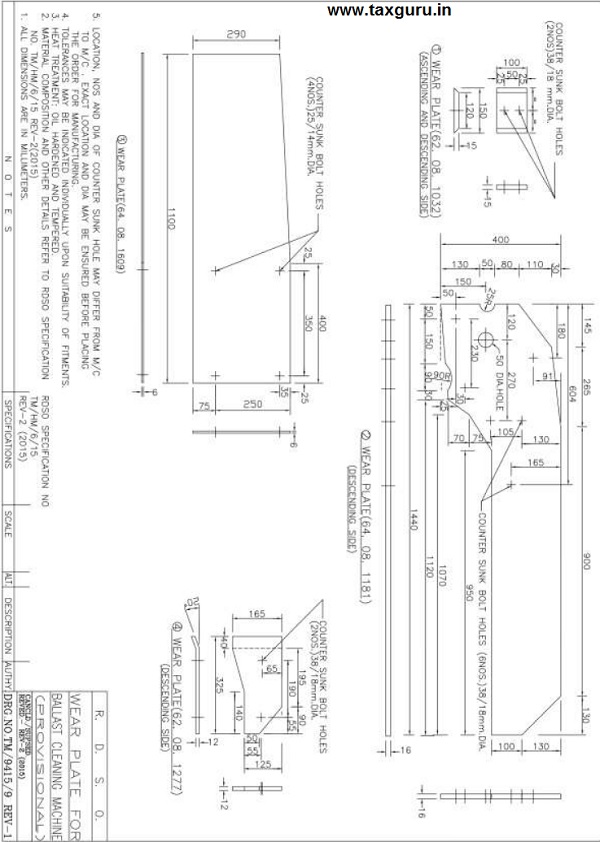

B. WEAR PLATES – Used in Ballast Cleaning Machine:

7.1 Considering the vertical thrust coming on railway track, the track is required to be cushioned with specific size of ballast (Grit/Kapachi) to transfer the vertical thrust to the soil. During working over the period of time this ballast becomes rigid due to accumulation of fine dust, mud and sand particles and creating hurdles to maintain track up to the standard with use of track tampers, thus requires periodic cleaning and screening. Ballast Cleaning Machine is an important Track Maintenance Vehicle used to clean ballast. Ballast below track is removed by cutter bar and conveyed up to screens thru TURF (Red arrow marked line shows the movement of ballast) by chain. The TURF is lined with various wear plates as per machine design and due to continuous friction between ballast, wear plates and chain the wear plates get wear out during working which needs to be replaced time to time to protect basic body of machine. As the machine cannot work without wear plates and BCM machine is a very important self-propelled track maintenance vehicle, wear plates of BCM should fall under HSN code 86040000 as a part of track maintenance vehicle.

7.2 PHOTOGRAPH OF WEAR PLATE:

7.3. RDSO DRAWINGS ON THE BASIS OF WHICH THE SAID WEAR PLATES ARE MANUFACTURED: Trio Enterprise (Main Contractor) has received Purchase order from Western Central Railway by PO NO. 99185424150453, dated 13-7-2018 for supply of WEAR PLATES as per RDSO Drawings mentioned in it. Against which Trio Enterprise has given BACK TO BACK order to Clad Weld Technologies Pvt Ltd.. To manufacture WEAR PLATES as per the said mentioned RDSO drawing Numbers as given by Western Central Railway by mentioning the said RDSO drawing numbers in the work order given to Clad Weld Technologies Pvt Ltd. by order dated 13-7- 2018. The copies of both the work orders have already been furnished to the authorities in their earlier submissions. So, the RDSO drawing numbers can be easily identified from it.

7.4 Now, with this they have attached RDSO Drawings as required by the authorities. There is RDSO drawing as mentioned in the work order which are as under:

RDSO Drawing No. TM/9415/9 REV-1

THE DRAWING IS ATTACHED HEREWITH

The RDSO Drawing No. is mentioned at the bottom of the right side of the drawing.

BALLAST CLEANING MACHINE

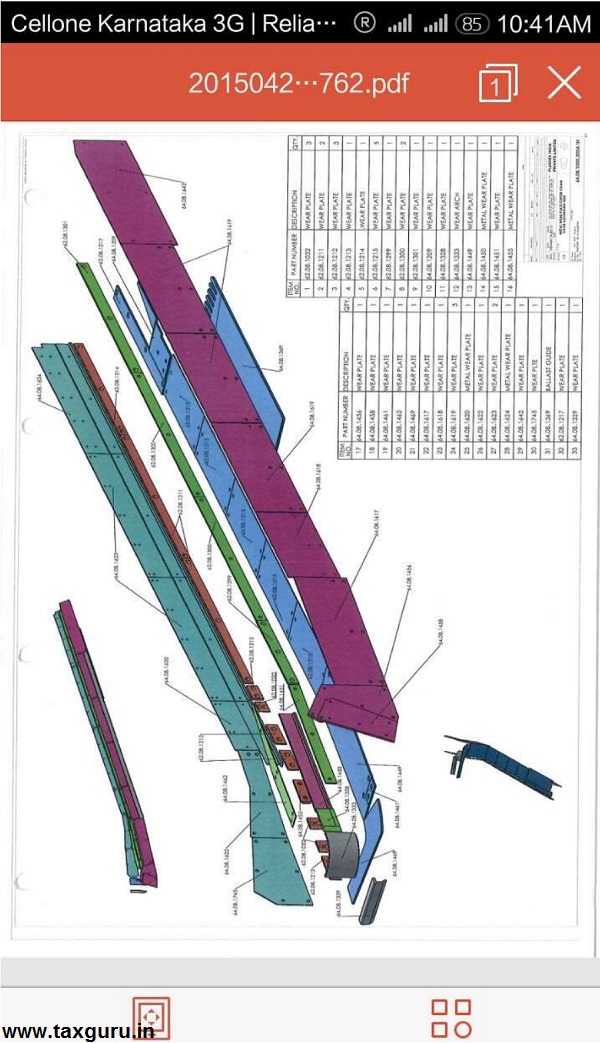

7.5 PHOTO GRAPH OF BALLAST CLEANING MACHINE – WHERE WEAR PLATE IS FIXED:

7.6 Arrangements of fixing wear plates in ballast cleaning machines is shown in sketch below. These wear plates are solely used in BCM machines of railway and are not useful in any other machines elsewhere as can be seen from the arrangement sketch below:

8. DETAILS REGARDING RDSO DRAWING:

SO is the sole R&D organisation of Indian Railways and functions as the technical advisor to Railway Board Zonal Railways and Production Units and performs the following important functions:

- Development of new and improved designs.

- Development, adoption, absorption of new technology for use on Indian Railways.

- Development of standards for materials and products specially needed by Indian Railways.

- Technical investigation, statutory clearances, testing and providing consultancy services.

- Inspection of critical and safety items of rolling stock, locomotives, signalling & telecommunication equipment and track components.

- RDSO multifarious activities have also attracted attention of railway and non-railway organisations in India and abroad.

8.1 SCREEN SHOT OF THE WEBSITE OF RDSO:

Justification regarding tamping tool and wear plates as manufactured by the applicant is specifically manufactured for railways and specifically used by railways only:

9. As mentioned above that M/s Trio Enterprise has got order from Railways and given as a back to back order to the applicant for manufacturing of Tamping Tool and Wear Plates as per RDSO drawings as mentioned in the work order as received from Railways. So, both the products are specifically manufactured as per RDSO drawings by the applicant and supplied to M/s Trio Enterprise, which ultimately supplied as a back to back supply to the Railways by Trio Enterprise. So, there is no general usage of the said product as covered above.

10. In their submission supra, they have attached photographs of both the products along with the photographs of Railway Track Maintenance Machines (Ballast Cleaning Machinery & Tie Tamping Machinery) along with the place where both the products are fixed in the abovementioned machinery and working of the same. This also justifies the usage of the product is only for Railways and not for general use.

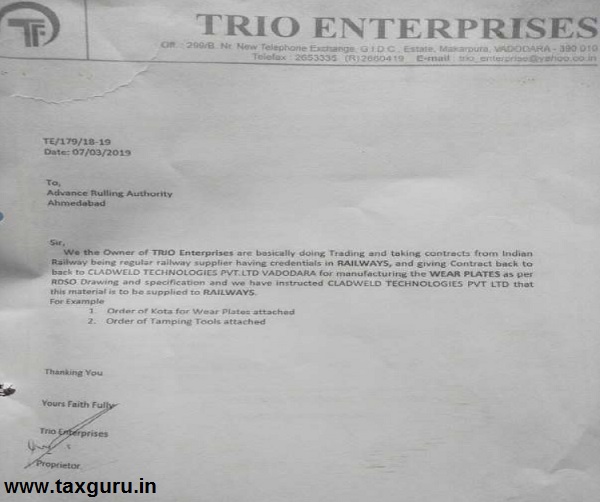

11. They also obtained a letter from M/s Trio Enterprise, referring to Advance Ruling Authority dated 7-3-2019 stating that M/s Trio Enterprise is doing Trading activity and taking contracts from Indian Railway being regular railway supplier having Credentials in Railways, and giving contract of manufacturing of those products as back to back order to M/s Clad Weld Technologies Pvt Ltd. for manufacturing of Wear plates and Tamping tool as per RDSO drawings and specification. The copy of the said letter has also been attached herewith for kind reference to justify that both the products are ultimately manufactured as per Railway’s RDSO drawing specification and would be supplied to Railways only by M/s Trio Enterprise for usage of Railway Track Maintenance machinery only.

Scan Image of the letter dated 7-3-2019 obtained from M/s Trio Enterprise

12. DETERMINATION OF RATE OF TAX AND ENTRY FALLING IN CHAPTER 86:

Chapter 86: Railway or Tramway Locomotives, rolling Stock and parts thereof; Railway or Tram Way Track fixtures and Fittings and parts thereof; Mechanical (Including electro Mechanical) Traffic signalling Equipment of all kinds.

HSN-86040000: Railway or tramway maintenance or service vehicles whether or not self-propelled (For Example, workshops, Cranes, Ballast Tampers, Track liners, Testing coaches and track inspection vehicles) From abovementioned details, it is very clear that both the items – wear plates and tamping tools are specifically manufactured for and used by Railways and should fall under Chapter 86.

12.1 Now, as per Notification No. 1/2017-Central Tax(Rate), dated 28th June, 2017, entry No. 238 covers rate of tax liable @ 2.5% CGST and @ 2.5% SGST in total taxable @ 5%.

12.2 Further reference is to be given to Clarification on supplies made to the Indian Railways classifiable under any chapter, other than Chapter 86– regarding, F. No.354/1/2018-TRU, Circular No. 30/4/2018-GST, dated 25th January, 2018. As Chapter 86 covers parts also for the specified items, the same should be supplied @ 5% to Railways.

12.3 Further, w. e. f. 1st October, 2019, as per Notification No.14/2019-Central Tax (Rate) dated 30th September, 2019, it would be liable to be taxed @ 6% CGST and @ 6% SGST in total taxable @ 12% as per new entry No. 205D in Schedule II.

12.4 Considering abovementioned facts, as the Wear plates and Tamping tools are manufactured as per the RDSO specification, the applicant should charge GST @ 5% before 30-09-2019 and @ 12% after 01-10-2019 to M/s Trio Enterprise.

12.5 Further, they also relied upon the AAR judgment in the case of Shree Construction, dtd.11-7-2018, by Maharashtra Authority of AAR where subcontractor is allowed to charge rate of tax to Main Contractor as applicable to main contractor if the work is performed for railways and when the same is directly transferred to railways.

DISCUSSION & FINDINGS:

13. We have considered the submissions made by the applicant in their application for advance ruling as well as at the time of personal hearing. We also considered the issue involved, on which advance ruling is sought by the applicant, relevant facts & the applicant’s interpretation of law.

13.1 At the outset, we would like to state that the provisions of both the CGST Act and the GGST Act are the same except for certain provisions. Therefore, unless a mention is specifically made to such dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provisions under the GGST Act.

14. In the instant case, the applicant has sought advance ruling in respect of following question:

“Whether supply to be made by the applicant of Wear Plates and Tamping Tools as manufactured specifically as per RDSO Drawing directly to the Railway Authorities as per the Order received from M/s Trio Enterprise, should be fall under HSN 86040000 & classified under Chapter 86 and should be taxed GST @ 5%?”

15. On going through the submission given by the applicant, we find that the applicant is having factory at Survey No. 428/1, Village-Nana Fofalia, Dabhol, Vadodara, Gujarat-391210, engaged in the manufacture of Wear plats & Tampering tools.

16. The applicant submitted that:

(i) M/s Trio Enterprise has got order from Railways and given as a back to back order to the applicant for manufacturing of Tamping Tool and Wear Plates as per RDSO drawings as mentioned in the work order as received from Railways. Copy of the POs as received by M/s Trio Enterprise from Railways and as issued by M/s Trio Enterprise to the Applicant for said supply also submitted by them. So, both the products are specifically manufactured as per RDSO drawings by the applicant and supplied to M/s Trio Enterprise, which ultimately supplied as a back to back supply to the Railways by Trio Enterprise. So, there is no general usage of the said product as covered above.

(ii) In their submission supra, they have attached photographs of both the products along with the photographs of Railway Track Maintenance Machines (Ballast Cleaning Machinery & Tie Tamping Machinery) along with the place where both the products are fixed in the abovementioned machinery and working of the same. This also justifies the usage of the products is only for Railways and not for general use.

(iii) The ‘Wear plates’ and ‘Tamping tools’ supplied by them are used as parts of the Railway Track Maintenance Vehicles viz. the Ballast Cleaning Machine and the Tie Tamping Machine and, hence, both products should fall under HSN Code 86040000 as a part of track maintenance vehicles.

(iv) As per Notification No. 1/2017-Central Tax(Rate), dated 28th June, 2017 entry No. 238 covers rate of tax liable @ 2.5% CGST and @ 2.5% SGST in total taxable @ 5%.

(v) Further reference is to be given to Clarification on supplies made to the Indian Railways classifiable under any chapter, other than Chapter 86– regarding, F. No.354/1/2018-TRU, Circular No. 30/4/2018-GST, dated 25th January, 2018.. As Chapter 86 covers parts also for the specified items, the same should be supplied @ 5% to Railways.

(vi) Further, w. e. f. 1st October, 2019, as per Notification No.14/2019-Central Tax (Rate) dated 30th September, 2019, it would be liable to be taxed @ 6% CGST and @ 6% SGST in total taxable @ 12% as per new entry No. 205D in Schedule II.

(vii) Considering abovementioned facts, as the Wear plates and Tamping tools are manufactured as per the RDSO specification, the applicant should charge GST @ 5% before 30-09-2019 and @ 12% after 01-10-2019 to M/s Trio Enterprise.

(viii) Further, they also relied upon the AAR judgment in the case of Shree Construction, dtd.11-7-2018, by Maharashtra Authority of AAR where subcontractor is allowed to charge rate of tax to Main Contractor as applicable to main contractor if the work is performed for railways and when the same is directly transferred to railways.

17. In this regard, first we have gone through the usage of the products in question i.e. “Wear Plates” and “Tamping Tools” and classification thereof, as described by the applicant in subject application, which reads as under:

Wear Plates used in Ballast Cleaning Machine: Considering the vertical thrust coming on railway track, the track is required to be cushioned with specific size of ballast (Grit/Kapachi) to transfer the vertical thrust to the soil. During working over the period of time, this ballast becomes rigid due to accumulation of fine dust, mud and sand particles and creating hurdles to maintain track up to the standard with use of track tampers, thus requires periodic cleaning and screening. Ballast Cleaning Machine is an important Track Maintenance Vehicle used to clean ballast. Ballast below track is removed by cutter bar and conveyed up to screens thru TURF (Red arrow marked line shows the movement of ballast) by chain. The TURF is lined with various wear plates as per machine design and due to continuous friction between ballast, wear plates and chain, the wear plates get wear out during working, which needs to be replaced time to time to protect basic body of machine. As the machine cannot work without wear plates and BCM machine is a very important self-propelled track maintenance vehicle, wear plates of BCM should fall under HSN code 86040000 as a part of track maintenance vehicle.

Tamping Tool used in Tie Tamping Machine: Railway track is cushioned with ballast to absorb the vertical thrust generated by the train running on it with high speed. Due to continue jerks and vibration, it gets loose and unorganized which is required to be tamped time to time. Tie Tamping Machine is another self-propelled track maintenance vehicle which does ballast tamping work and Tamping Tools is the key component of machine which get wear out after few days of working due to friction between ballast and tools. These tools required being replaced time to time to keep the machine and in turn the railway track working. As tamping tool is important part of this self-propelled track maintenance vehicle, it should fall under HSN code 86040000.

17.1 From the above submission, we find that the ‘Wear Plates’ and the ‘Tamping Tools’ are used in the Ballast Cleaning Machine and the Tie Tamping Machine, respectively. These machines are used for the servicing and maintenance of the railway track lines.

18. Further, we have also perused the photographs of both the products, viz. ‘Wear Plates’ & ‘Tamping Tools’ along with the photographs of Railway Track Maintenance Machines viz. Ballast Cleaning Machinery & Tie Tamping Machinery, the place where both the products are fixed in the abovementioned machineries and working of the same and we find that the Ballast Cleaning Machine and the Tie Temping Machine are self-propelled Track Maintenance Vehicles of the Railway. The Ballast Cleaning Machine is used to clean ballast (Grit/Kapachi) and without ‘Wear Plates’ it cannot run. Whereas, the Tie Tamping Machine is used for ballast (Grit/Kapachi) tamping work. Tamping Tools is the key component of the Tie Tamping Machine, which get wear out after few days of working due to friction between ballast and tools. These tools required being replaced time to time to keep the machine and in turn the railway track working. Thus, ‘Wear plates’ and ‘Tamping tools’ supplied by the applicant are having specific use and are essential parts of the Ballast Cleaning Machine and the Tie Tamping Machine of railways, respectively.

19. In view of the above, we come to the conclusion that the applicant has specifically manufactured the products, viz. ‘Tamping Tool’ and ‘Wear Plates’ as per RDSO drawings of the Railway and supplied the same to M/s Trio Enterprise, which ultimately supplied as a back to back supply to the Railways by M/s Trio Enterprise. Said ‘Wear plates’ and ‘Tamping tools’ are having specific use and are essential parts of the Railway Track Maintenance Vehicles viz. the Ballast Cleaning Machine and the Tie Tamping Machine.

20. In order to determine the classification and the tax liability under GST in respect of supply of the goods viz. ‘Wear plates’ and ‘Tamping tools’ to Railways by the applicant, we are required to refer to the Notification No. 1/2017-Central Tax(Rate), dated 28th June, 2017 containing the sub-headings as well as the rates of Central GST applicable to various goods, which are covered under 6 Schedules, as below:

(i) 5 per cent. in respect of goods specified in Schedule I,

(ii) 6 per cent. in respect of goods specified in Schedule II,

(iii) 9 per cent. in respect of goods specified in Schedule III,

(iv) 14 per cent. in respect of goods specified in Schedule IV,

(v) 5 per cent. in respect of goods specified in Schedule V, and

(vi) 125 per cent. in respect of goods specified in Schedule VI.

Further, Explanations (iii) and (iv) of the said Notification read as under:

(iii) “Tariff item”, “sub-heading” “heading” and “Chapter” shall mean respectively a tariff item, sub-heading, heading and chapter as specified in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975).

(iv) The rules for the interpretation of the First Schedule to the Customs Tariff Act, 1975 (51 of 1975), including the Section and Chapter Notes and the General Explanatory Notes of the First Schedule shall, so far as may be, apply to the interpretation of this notification.

21. As claimed by the applicant that Wear plates’ and ‘Tamping tools’ should fall under HSN Code 86040000 as a part of Railway Track Maintenance Vehicle, we have to examine the said entry as appearing in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) and Chapter Note 3 of Chapter 86, which reads as under:

“Chapter 86: Railway or tramway locomotives, rolling-stock and parts thereof; railway or tramway track fixtures and fittings and parts thereof; mechanical (including electro-mechanical) traffic signalling equipment of all kinds.

Chapter sub-heading 8604 00 00: Railway or Tramway Maintenance or Service Vehicles whether or not Self Propelled (For Example, Workshops, Cranes, Ballast Tampers, Track Liners, Testing Coaches and Track Inspection Vehicles)”.

Chapter Note 3 of Chapter 86: References in Chapters 86 to 88 to “parts” or “accessories” do not apply to parts or accessories which are not suitable for use solely or principally with the articles of those Chapters. A part or accessory which answers to a description in two or more of the headings of those Chapters is to be classified under that heading which corresponds to the principal use of that part of accessory.

22. Further, we have also referred the Explanatory Notes to the HSN. As per Explanatory Notes to HSN code 86.04, “the vehicles covered by this heading, whether or not self-propelled, are specially designed for use e.g. in the installation, servicing and maintenance of the permanent way and structures alongside tracks.” It further states that the heading includes “Self-propelled Vehicles for track maintenance (in particular, railway track lines) equipped with one or more engines which not only power the working machines mounted thereon (i.e. track-setters, ballast tampers etc.) and propel the vehicle while work in progress but also enable it to travel rapidly along the track, as a Self-propelled Unit, when the working machines are not in operation. (Ref. Sl. No. 9)”.

23. Thus, the Chapter sub-heading No.8604 00 00 covers only the ‘Railway or Tramway Maintenance or Service Vehicles whether or not Self Propelled’. However, this sub-heading is totally silent about the parts of the said vehicles.

24. We further note that the classification of parts and accessories of all the vehicles, aircraft or equipment concerned of Chapter 86 is provided in subheading No. 8607, which reads as under:

“8607 parts of railway or tramway locomotives or rolling stock:

860711 Truck assemblies for self-propelled vehicles

860712 Other truck assemblies

860719 Other, including parts Axles and parts thereof

860721 Air brakes and parts thereof

860729 Other Brakes and parts thereof

860730 Hooks and other coupling devices, buffers and parts thereof

860791 Other parts of locomotives

860799 Other Parts of railway or tramway locomotives or rolling stock.”

25. As already mentioned that the Ballast Cleaning Machine and the Tie Tamping Machine are used for the servicing and maintenance of the railway track lines. Both are self-propelled Track Maintenance Vehicles of the Railway. Therefore, undoubtedly, both the Ballast Cleaning Machine and the Tie Tamping Machine will fall under sub-heading No.8604 00 00. Further, the applicant has ‘specifically manufactured the products, viz. ‘Tamping Tool’ and ‘Wear Plates’ as per RDSO drawings of the Railway and supplied the same to M/s Trio Enterprise, which ultimately supplied as a back to back supply to the Railways by M/s Trio Enterprise. Said ‘Wear plates’ and ‘Tamping tools’ are parts of the Railway Track Maintenance Vehicles viz. the Ballast Cleaning Machine and the Tie Tamping Machine. We further note that there is no specific sub heading provided for the parts of said Railway Track Maintenance Vehicles falling under Chapter sub-heading No.86040000 of the Customs Tariff Act, 1962 and, therefore, we hold that said ‘Wear plates’ and ‘Tamping tools’, being parts of the said Railway Track Maintenance Vehicles, are classifiable under residuary entry of Chapter 86 i.e. sub-heading No. 860799 (Other Parts of railway or tramway locomotives or rolling stock), as extracted herein above.

26. To determine the rate of GST in respect of the products in question, we have gone through the respective entries of the Chapter heading 8604 and 8607 in the Notification No. 1/2017-Central Tax(Rate), dated 28th June, 2017 (hereinafter referred to as the said notification) and find that the goods of Chapter heading 8604 and 8607 are covered in Entry at Sl. No.238 & 241 of the Schedule I of said Notification, which read as under:

Schedule I-2.5%

| S. No. | Chapter/Heading/ Subheading/ Tariff item | Description of goods |

| 238. | 8604 | Railway or tramway maintenance or service vehicles, whether or not self-propelled (for example, workshops, cranes, ballast tampers, track-liners, testing coaches and track inspection vehicles) |

| 241. | 8607 | Parts of railway or tramway locomotives or rolling-stock; such as Bogies, bissel-bogies, axles and wheels, and parts thereof. |

It can be seen from above that goods of Chapter heading 8604 & 8607 attract GST @ 5%.

26.1 We have also perused the Circular No. 30/4/2018-GST, dated 25th January, 2018. issued from F. No.354/1/2018-TRU as quoted by the applicant, wherein it has been clarified that;

- “only the goods classified under Chapter 86, supplied to the railways attract 5% GST rate with no refund of unutilised input tax credit and

- other goods [falling in any other chapter], would attract the general applicable GST rates to such goods, under the aforesaid notifications, even if supplied to the railways.”

It can be seen from above clarification that all the goods classified under Chapter 86, supplied to railway will attract 5% GST.

26.2 We further note that the Notification No.14/2019-Central Tax (Rate) dated 30th September, 2019 amended the Notification No. 1/2017-Central Tax(Rate), dated 28th June, 2017 (w. e. f. 1st October, 2019), resulting that the goods of Chapter heading 8604 and 8607 would be liable to be taxed @ 6% CGST and @ 6% SGST (in total taxable @ 12%) as per new entry Nos. 205D & 205G in Schedule II, as extracted below:

Schedule II- 6%

| S. No. |

Chapter/Heading/ Subheading/ Tariff item | Description of goods |

| 205D. | 8604 | Railway or tramway maintenance or service vehicles, whether or not self-propelled (for example, workshops, cranes, ballast tampers, track-liners, testing coaches and track inspection vehicles) |

| 205G. | 8607 | Parts of railway or tramway locomotives or rolling-stock; such as Bogies, bissel-bogies, axles and wheels, and parts thereof. |

It can be seen from above that goods of Chapter heading 8604 & 8607 would attract GST @ 12% w. e. f. 01.10.2019.

27. In view of the above, we hold the classification of the “Wear plates” and “Tamping Tool” manufactured specifically as per RDSO Drawing and supplied to the Railways through M/s Trio Enterprise, being a parts of a self-propelled track maintenance vehicles (viz. the Ballast Cleaning Machine & the Tie Tamping Machine), under chapter sub-heading 860799 (Other Parts of railway or tramway locomotives or rolling stock), and, hence, same will attract GST @ 5% under S. No. 241 of the Schedule I till 30.09.2019 and w. e. f. 01.10.2019, @12% under S. No.205G of the Schedule-II to the Notification No.01/2017- Central Tax (Rate) dated 28.06.2017, as amended.

28. In light of the above discussions, we rule as under –

RULING

Question: “Whether supply to be made by the applicant of Wear Plates and Tamping Tools as manufactured specifically as per RDSO Drawing, directly to the Railway Authorities as per the Order received from M/s Trio Enterprise, should fall under HSN 86040000 & classified under Chapter 86 and should be taxed GST @ 5%?”

Answer: No. The products, “Wear plates” and “Tamping Tool” manufactured specifically as per RDSO Drawing and supplied to the Railways through M/s Trio Enterprise, being a parts of a self-propelled track maintenance vehicles (viz. the Ballast Cleaning Machine & the Tie Tamping Machine), are classifiable under chapter sub-heading 860799 (Other Parts of railway or tramway locomotives or rolling stock), and, hence, same would attract GST @ 5% under S. No. 241 of the Schedule I till 30.09.2019 and w. e. f. 01.10.2019, @12% under S. No.205G of the Schedule-II to the Notification No. 1/2017-Central Tax(Rate), dated 28th June, 2017, as amended.