To improve and simply, GST Council approved concept of new simplified format of GST returns in its 28th GST Council meeting held on 21st JULY,2018.

Revised Formats are proposed to implement with effect from 1st April,2019 on trial basis and if it operates well then such formats will become mandatory with effect from 1st July,2019, as decided in 31st GST Council meeting. However, due to lack of technical support only GSTR-1, GSTR-3B (Summary return) are continue till March,2020..

The GST Council officially unveiled three new GST returns forms names GST RET-1 “NORMAL Form”, GST RET-2” SAHAJ Form” and GST RT-03 “SUGAM” Form . The new GST returns forms will be introduce on trial basis from Nov,2019 to Mar,2020 along with existing returns i.e. GSTR-1,GSTR-2 AND GSTR-3B etc.,

Now, we see how New GST Returns Scheme Normal, Sahaj and Sugam Forms are prepare and upload in the GSTN Site. What are the procedures we have to follow to prepare New GST Return Forms i.e. Normal, Sahaj and Sugam.

Dear colleagues, firstly we have to refer what are the conditions to choose each form of your client. The conditions are as below:

A) Aggregate turnover of the last Finance Year i.e 2018-19 as per definition of ‘AGGREGATE TURNOVER” under GST Law,2017,

B) Whether your client is having E-Commerce transactions or not

C) Your client cannot make supplies through E-Commerce Operators on which tax is required to be collected U/s. 52.

The Following table will help you to understand what are the options available to you on the basis of aggregate turnover :

| Turnover | New Return Form | Frequency of Filling of Form | Description |

| Turnover Above Rs.5 Cr. | Form GST RET-1 | Normal (Monthly) | If your client is new registered taxpayer turnover will be decided on the basis of self-declaration made by them on estimated turnover. |

| Turnover Up to Rs.5 Cr.. | Form GST RET-1 | Normal (Monthly) | If your client already registered tax payer it will be decided on the basis of last year turnover. |

| Turnover Up to Rs.5 Cr. | Form GST RET-1 | Normal (Quarterly) | If your client already registered tax payer it will be decided on the basis of last year turnover. |

| Turnover Up to Rs.5 Cr. | Form GST RET-2 | SAHAJ (Quarterly) | If your client already registered tax payer it will be decided on the basis of last year turnover. |

| Turnover Up to Rs.5 Cr. | Form GST RET-3 | SUGAM (Quarterly) | If your client already registered tax payer it will be decided on the basis of last year turnover. |

Note:

1). Aggregate Turnover above Rs.5 Cr. Form GST RET-1 is applicable. No option to choose Form GST RET-1 (Normal-Quarterly) ( GST RET-2 –SAHAJ) and GST RET-3 – SUGAM) . so, If your client is having aggregate turnover more than of Rs.5 Cr.as per GST Law, for the last Financial Year he would be File Form GST RET-1 monthly is mandatory.

2). Change in periodicity of the return filling ( from quarterly to monthly and vice versa) would be allowed only once at the time of filling the first return by a taxpayer.

3). Periodicity of return filing will remain unchanged during the next Financial Year , unless changed before filling the first return of that year.

If your client’s aggregate turnover up to Rs.5 Cr. there are an options to switch over from one return to other return. The following table will help you for better under -stand:

| Return | Switch over to | Conditions |

| Normal (Quarterly) | SUGAM or SAHAJ | Only once in a Financial Year at the beginning of any quarter. |

| Sugam | Sahaj | Only once in a Financial Year at the beginning of any quarter. |

| Sahaj | Sugam or Quarterly (Normal) | More than once in a Financial Year at the beginning of any quarter. |

| Sugam | Quarterly (Normal) | More than once in a Financial Year at the beginning of any quarter. |

As per GST Council and Central Government says that under new system you will be filling single return only. But practically this single return is divided into following three forms.

1. GST ANX-1,

2. GST ANX-2

3. Form GST RET ; (1/2/3).

1. GST Annuxure-1 , you have to fill up Outward Supplies and also Inward Supplies i.e. liable to pay RCM.

2. GST Annuxure-2 , you have to fill up Inward Supplies ( Auto Populated through your suppliers GST Annuxure-1).

3. Form GST RET-(1,2,3) Main Return with summary of liability and Input Tax Credit

> In existing return system i.e. GSTR-1 and GSTR-3B taxpayer cannot enter negative figures but this new system you have been fixed negative figures.

> Option of filling NIL returns through SMS will be there. ( There is no necessity further processes of return)

> If you file NIL returns through GST Portal will take directly to signature tab. So, irrelevant activity will not be required.

> All supplies relating to Schedule III shall be reported under “NO SUPPLY” in the main return. It will include HIGH SEA SALE AND BONDED WAREHOUSE SALES also.

> HSN code for services shall be reported at six digit level or more irrespective of the turnover during the preceding financial year .

> Outward supplies liable to RCM will be reported only by recipient and not by supplier.

> Invoices of any preceding period not uploaded earlier can also be uploaded during the current month. The liability on such invoices will be paid during the current month but these invoices will be clubbed with the respective tax period after filing return of the current month.

INDEX

| S.NO. | NAME | DESCRIPTION |

| PROFILE UPDATION | ||

| 1. | Profile Option | Intimation of option for return periodicity and type of quarter return |

| FORM GST RET-01 (Regular/Quarterly/Normal) | ||

| 2. | FORM GST ANX-1 | Annexure of outward supplies, imports and inward supplies attracting RCM. |

| 3. | FORM GST ANX-2 | Annexure of inward supplies |

| 4. | FORM GST RET-1 | Monthly/Quarterly (Normal) return |

| 5. | FORM GST ANX-1A | Amendment to FORM GST ANX-1 |

| 6. | FORM GST RET-1A | Amendment to FORM GST RET-1 |

| FORM GST PMT -08 | ||

| 7. | FORM GST PMT-08 | Payment of self-assessed Tax |

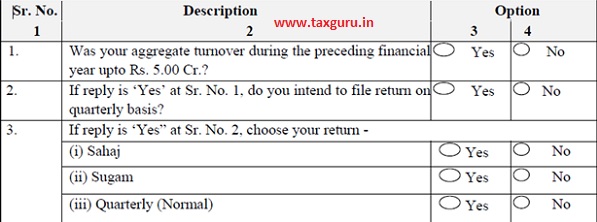

Profile Updation:

Intimation of option for return periodicity and type of quarterly return.

Note : Before filling FORM GST RET-1, these following Important Points to be remember.

1. Periodicity of filing return will be deemed to be monthly for all taxpayers unless quarterly filing of the return is opted for.

2. For newly registered taxpayers, turnover will be considered as zero and hence they will have the option to file monthly, Sahaj, Sugam or Quarterly (Normal) return.

3. Change in periodicity of the return filing (from quarterly to monthly and vice versa) would be allowed only once at the time of filing the first return by a taxpayer.

4. The periodicity of the return filing will remain unchanged during the next financial year unless changed before filing the first return of that year.

5. The taxpayers opting to file quarterly return can choose to file any of the quarterly return namely – Sahaj, Sugam or Quarterly (Normal).

6. Taxpayers filing return as Quarterly (Normal) can switch over to Sugam or Sahaj return and taxpayers filing return as Sugam can switch over to Sahaj return only once in a financial year at the beginning of any quarter.

7. Taxpayers filing return as Sahaj can switch over to Sugam or Quarterly (Normal) return and taxpayers filing return as Sugam can switch over to Quarterly (Normal) return more than once in a financial year at the beginning of any quarter.

8. Taxpayers opting to file quarterly return as ‘Sahaj’ shall be allowed to declare outward supply under B2C category and inward supplies attracting reverse charge only. Such taxpayers cannot make supplies through e-commerce operators on which tax is required to be collected under section 52. Such tax payers shall not take credit on missing invoices and shall not be allowed to make any other type of inward or outward supplies. However, such taxpayers may make Nil rated, exempted or Non-GST supplies which need not be declared in the said return.

9. Taxpayers opting to file quarterly return as ‘Sugam’ shall be allowed to declare outward supply under B2C and B2B category and inward supplies attracting reverse charge only. Such taxpayers cannot make supplies through e-commerce operators on which tax is required to be collected under section 52. Such tax payers shall not take credit on missing invoices and shall not be allowed to make any other type of inward or outward supplies. However, such taxpayers may make Nil rated, exempted or Non-GST supplies which need not be declared in said return.

10. Taxpayers opting to file monthly return or Quarterly (Normal) return shall be able to declare all types of outward supplies, inward supplies and take credit on missing invoices.

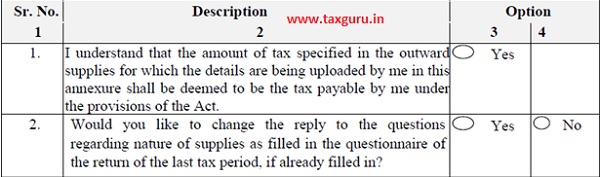

Dear Friends now you have to choose and uploading information in FORM GST ANX-1 you have to give answers to the following questioner in Part-A and Part-B after that FORM GST ANX-1 will be open for fill the data..

Part-A: Brief questions about relating the option given in previous tax period.

NOTE: In case the reply to question as S.No.2 is “YES” the following questionnaire will be opened for exe rising the option. In the first tax period, it would be open for all taxpayers.

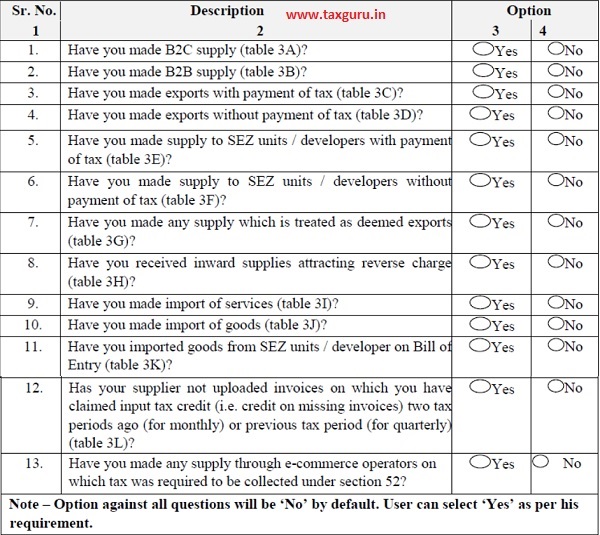

Part-B: Detailed Questionnaire:

–

3. Details of outward supplies, inward supplies attracting reverse charge and import of goods and services

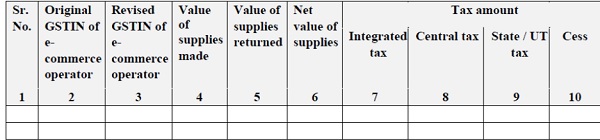

4. Details of the supplies made through E-Commerce operators liable to collect tax under section 52 (out of any outward supplies declared in table 3)

Instructions (FORM GST ANX-1).

A. General Instructions:

1. Terms used:

(a). GSTIN: Goods and Services Tax Identification Number

(b). UIN : Unique Identity Number

(c). HSN Code: Harmonized System of Nomenclature Code

(d). POS : Place of Supply (Respective State/UT)

(e). B2B : Supplies made to registered persons having GSTIN or UIN

(f). B2C : Supplies made to consumers and un-registered persons , not having GSTIN OR UIN

(g). Type of document: Invoice (including revised invoices), debit/credit note, bill of supply, bill of entry etc.,

(h). ARN : Acknowledgement Reference Number.

2. Registered person can upload the details of documents any time during a month/quarter to which it pertains or of any prior period but not later than the due date for furnishing of return for the month of September or second quarter following the end of the financial year to which such details pertains or the actual date of furnishing of relevant annual return whichever is earlier except that –

(i) the taxpayer filing the return on monthly basis will not be able to upload the details of documents from 18th to 20th of the month following the tax period.

(ii) the taxpayer filing the return on quarterly basis will not be able to upload the details of documents from 23rd to 25th of the month following the quarter.

3. Supplier can upload the documents for any supply on real time basis. Facility for accepting such documents by the recipient shall be made available. Details of documents uploaded by the supplier will be shown to the concerned recipient also on near real time basis.

4. Details of the documents issued during the tax period or of any prior period by the supplier and uploaded by him after filing of the return for such prior period will be accounted for towards the tax liability of the supplier in the return in which such details have been uploaded.

5. Advances received on account of supply of services shall not be reported here. The same shall be reported in Table 3C(3) and adjustment thereof shall be reported in table 3C(4) of FORM GST RET-1.

6. Recipient will get credit during a tax period on the basis of the details of documents uploaded by the supplier upto the 10th of the month following the month for which the return is being filed for. Such credit can be availed i.e. credited to the ledger of the recipient only on filing of his (i.e. recipient’s) return. There may be following two scenarios:

(i) If the recipient files his return on a monthly basis, say, for the month of January, 2019 on 20th February, 2019, he shall be eligible to take credit in his return based on the documents uploaded by the supplier up to the 10th of February, 2019 irrespective of whether the supplier files his return on monthly or quarterly basis.

(ii) If the recipient files his return on a quarterly basis (Normal, Sahaj or Sugam), say for the quarter January – March, 2019 on 25th April, 2019, he shall be eligible to take credit in his return based on the documents uploaded by the supplier upto the 10th of April, 2019 irrespective of whether the supplier files his return on monthly or quarterly basis.

7. Supplies attracting reverse charge will be reported only by the recipient and not by the supplier in this annexure. Such supplies shall be reported GSTIN wise and amount of tax and taxable value will be net of debit / credit notes and advance paid (on which tax has already been paid at the time of payment of advance), if any.

8. All suppliers with annual aggregate turnover of more than Rs. 5 crore and that in relation to exports, imports and SEZ supplies will upload HSN level data. HSN code shall be reported at least at six digit level for goods and at least at six digit level for services. Other taxpayers (turnover upto Rs. 5 crore) shall have an optional facility to report HSN code in the relevant table or leave it blank.

9. Tax amount shall be computed by the system based on the taxable value and tax rate. The tax amount so computed will not be editable except by way of issue of debit / credit notes. However, the tax amount under cess will be reported by the taxpayer himself.

10. Place of supply shall have to be reported mandatorily for all supplies. For intra-State supplies, the POS will be the same State in which the supplier is registered.

11. Tax rate applicable on IGST supplies can be selected from the drop down menu. For intra- State supplies, the tax rate shall be applied at half the rate of Integrated tax equally for Central tax and State / UT tax. Cess, if applicable, shall be reported under the cess column.

12. Value of supplies and amount of tax shall be reported in whole number or upto two decimal points at the most.

13. GSTIN/UIN of the recipient of supplies shall be reported in respect of supplies reported in table 3B, 3E, 3F and 3G.

14. GSTIN of the supplier shall be reported (wherever available) in table 3H, 3K and 3L from whom the supplies have been received. PAN may be reported in Table 3H if supplies attracting reverse charge are received from un-registered persons.

15. Wherever supplies are reported as net of debit/credit notes, the values may become negative in some cases and the same may be reported as such e.g. ( -100).

16. Details of documents of the period prior to introduction of the current return filing system can also be uploaded in the relevant tables of this annexure. Only those details shall be uploaded which have not been included in the erstwhile FORM GSTR-1. All supplies that are declared in this annexure will be accounted for payment of tax. Following scenarios may happen:

(i) Document has not been reported in FORM GSTR-1 and tax has also not been accounted for in FORM GSTR-3B – In this case, document shall be uploaded and tax shall also be paid along with applicable interest except in case of issuance of credit notes.

(ii) Document has not been reported in FORM GSTR-1 but tax has been accounted for in FORM GSTR-3B– In this case, document shall be uploaded and adjustment of tax accounted for shall be made in table 3C(5) of FORM GST RET-1, but in case of issuance of credit notes, upward adjustment shall be made in table 3A(8) of FORM GST RET-1.

(iii) Document has been reported in FORM GSTR-1 but tax has not been accounted for in FORM GSTR-3B – In this case, uploading of the document shall not be required but adjustment of tax shall be made in table 3A(8) or 3C(5) of FORM GST RET-1, as the case may be.

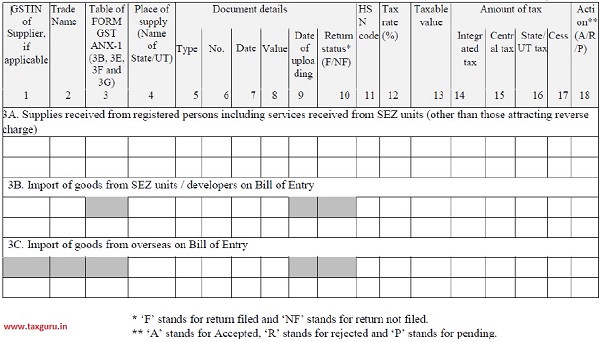

B. Table wise Instructions for fill up:

| Sr. No. | Table No. | Instructions for filling up. |

| 1 | 3A | All supplies made to consumers and u-registered persons (i.e. B2C) shall be reported in this table. Supplies shall be reported tax rate wise and net of debit/credit notes. HSN Code is not required to be reported in this table. |

| 2 | 3B | > All supplies (other than those attracting RCM) made to registered persons (GSTIN/UIN holders i.e. B2B) shall be reported in this table. Reporting of supplies made to Government department and other entities having TDS registration or through persons having TCS registration shall also be reported here. This would include amendments, if any.

> Supply of goods made by SEZ units/ developers to persons located in domestic tariff area (DTA) shall not be reported in this table as the same will be treated as imports by the recipient who shall report the same in table 3K. > Supply of services made by SEZ unit to persons located in domestic tariff area (DTA) shall be reported by the SEZ unit /developers in this table. > Supply of goods or services made to SEZ units/developers shall not be declared in this table and shall be reported in table 3E or 3F, as the case may be. > The “Value” in column 6 shall be the “invoice value” whereas the “taxable value” shall be reported in column 9. |

| 3 | 3C&3D | Export with payment of tax (IGST) shall be reported in table 3C while those without payment of tax shall be reported in table 3D. Shipping bill/Bill of export number available (till the date of filing of return) may be reported against export invoices. Details of remaining shipping bills can be reported after filling the return. A separate functionality for updation of details of shipping bill/ Bill of export in table 3C or table 3D will be made available on the portal. |

| 4. | 3E&3F | > All supplies made to SEZ units/developers shall be reported in table 3E &3F depending upon whether the supplies are made with payment or without payment of tax respectively. This would include amendments, if any.

> In case of supplies made with payment of tax, the supplier will have an option to select if the supplier or the SEZ units/ developers will claim refund on such supplies. If the supplier is not availing refund, only then the SEZ units/ developers will be eligible to avail input tax credit and claim refund for such credit after exports by them. |

| 5. | 3G | > All supplies treated as deemed exports shall be reported in this table. This would include amendments, if any,

> Supplies shall declare whether refund will be claimed by him or the recipient of deemed export supplies will be availing refund on such supplies. If refund is to be claimed by the supplier, then recipient will not be eligible to avail input tax credit on such supplies. |

| 6. | 3H | > All supplies attracting RCM shall be reported by the recipient. Only GSTIN wise details have to be reported. Invoice wise details are not required to be reported in this table.

> The amount of advance paid for such shall to be declared in the month in which the same was paid. > The value of supplies reported shall be net of debit/credit notes and advances on which tax has already been paid at the time of payment of advance, if any. > Where only advance had been paid to the supplier, on reporting the same, the credit shall flow to the return( FORM GST RET-1) and shall be reversed in table 4 of the said return. This credit can be availed only on receipt of the supply and issue of invoice by the supplier. |

| 7 | 3 I | > Import of services shall be reported in this table. The value of supplies shall be net of debit/credit notes and advances paid on which tax has already been pad at the time of payment of advance, if any. The amount of advance paid has to be paid declared in the month in which the same was paid. Invoice wise details are not required to be reported in this table.

> Services received from SEZ units/developers shall not be reported in this table. > Where only advance has been paid to the supplier, on reporting the same, the credit shall flow to the main return (FORMM GST RET-1) and shall be reversed in table 4 of the said return. This credit can be availed only on receipt f the supply ad issue of invoice by the supplier. |

| 8 | 3J | > Details of taxes paid on import of goods shall be reported in this table. These goods have already suffered IGST at the time of import and are not subject to taxation in this return. The exact amount of IGST and Cess paid at the port of import may be reported here, to avail input tax credit.

> Any reversal an account of in-eligibility of credit or otherwise is to be carried out in table 4B of the main return ( FORM GST RET-1). |

| 9. | 3K | > Goods received from SEZ units/ developers on Bill of entry shall be reported in this table by the recipient. These goods have already suffered IGST at the time of clearance into DTA and have been cleared on a Bill of Entry and are not subjected to taxation in this return.

> SEZ units/developers making such supplies shall not include such outward supplies in table 3B. > Reporting in table 3J and 3K shall be required till the time the data from ICEGATE and SEZ to GSTN system starts flowing online. |

| 10 | 3L | The recipient shall provide document wise details of the supplies for which credit has been claimed but the details of supplies are yet to be uploaded by the supplier (s) concerned as detailed below:

(i). Where the supplier has failed to report the supplies after a lapse of two tax periods in case of monthly return filers and after a lapse of one tax period in case of quarterly return filers. (ii). Where the supplier uploads the invoice subsequently (after reporting in this table by the recipient), then such credit has to be reversed by the recipient in table 4B(3) of the main return( FORM GST RET-1) as this credit cannot be availed twice. For example: in case where the supplier has made a supply in April but has not reported the same in FORM GST ANX-1 till 10th May and the recipient has claimed input tax credit by reporting the same in the main return (FORM GST RET-1) in table 4A(10) , reporting is required in the following situation: Where the supplier concerned has not uploaded the invoices in FORM GST ANX-1 of April, May or June tax period till 10th July, the recipient shall report the same, document wise in this table in FORM GST ANX-1 of June. |

| 11 | All Tables (3 series) | Debit / Credit notes issued by the supplier with respect to supplies other than supplies attracting RCM shall be reported in the respective tables. If debit/credit note is issued for the difference in tax rate only, then taxable value shall be reported as “Zero” , so that the liability computation is not disturbed. Only tax amount shall be reported in such cases. |

| 12 | 4 | Supplies made through e-commerce operators liable to collect tax under section 52 shall be reported at the consolidated level in this table even though these supplies have already been reported in table 3. |

C. Edit/Amendment of uploaded documents:-

1. Editing of documents up to the 10th of the following month:- Details of the documents uploaded up to the 10th of the following month may be edited by the supplier up to the said date (10th of the following month) only if such documents are not accepted by the recipient. If a document has already been accepted (up to 10th )by the recipient, then such document has to be reset / unlocked by the recipient and only then , it can be edited by the supplier up to the 10th of the following month, Following two scenarios may arise.

(i) In case, the recipient files his return on monthly basis, all the documents uploaded by any supplier (irrespective of the fact whether the supplier files his return on monthly or quarterly (Normal, Sahaj, Sugam) basis) shall be available for acceptance by such recipient up to the 10th of the month following the month for which the return is being filed. The supplier can edit the documents so accepted by the recipient only if the same are reset /unlocked by the recipient by the said date.

(ii) In case , the recipient files his return on quarterly ( Normal, Sahaj or Sugam) basis, all the documents uploaded by any supplier (irrespective of the fact whether the supplier files his return on monthly or quarterly (Normal, Sahaj, Sugam ) basis)shall be available for acceptance by such recipient up to the 10th of the month following the quarter for which the return is being filed. The supplier can edit the documents so accepted by the recipient only if the same are re-set/ unlocked by the recipient by the said date.

2. Supplier side Amendment: The return system provides for all editing or amendments from the supplier’s side only. The recipient will have the option to reset/ un-lock or reject a document but editing of or amendment to the same shall be made by the supplier only.

3. Edit/Amendment after 10th of the following month: The details of the documents uploaded by the supplier up to 10th of the month following the month or quarter for which the return is being for will be auto-populated and made available to the recipient in FORM GST ANX-2 to accept, reject or to keep the document pending.

4. Instructions regarding acceptance, rejection, or kept pending by the recipient may be referred to in the instructions to FORM GST ANX-2.

5. Documents rejected by the recipient shall be conveyed to the supplier only after filling of the return by the recipient.

6. The rejected documents may be edited before filing any subsequent return for any month or quarter by the supplier. However, credit in respect of the document so edited or uploaded shall be made available through the next open FORM GST ANX-2 for the recipient. However, the liability for such edited documents will be accounted for in the tax period (month or quarter) in which the documents will be accounted for in the tax period (month or quarter) in which the documents have been uploaded by the supplier.

7. Shifting of documents: In certain situations, the particulars of the document may be correct but the document has been reported in the wrong table. Therefore, when such documents are rejected by the recipient, instated of amending the document, a facility of shifting such documents to the appropriate table will be provided.

8. Amendment of documents relating to supplies made to persons other than persons filing return in FORM GST RET-1/2/3 (e.g. supplies made to composition taxpayers, ISD, UIN holders etc.) The documents relating to such supplies may be amended by the supplier at any time and the same shall not be dependent upon the action taken (accept/reject/pending) by the recipient.

Dear Colleagues I have completed my notes on FORM GST ANX-1 Annexure of outward supplies, imports and inward supplies attracting RCM. Instructions for filling FORM GST ANX-1 table wise. Now from tomorrow onward I have to provide my notes on FORM GST ANX-2 in detail instructions for how to fill the form and also table wise for better under -standing. Kindly provide your suggestions on my notes on FORM GST ANX-1.

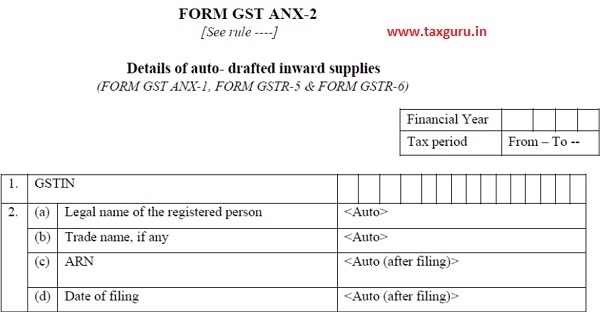

Detailed notes on FORM GST ANX-2 .

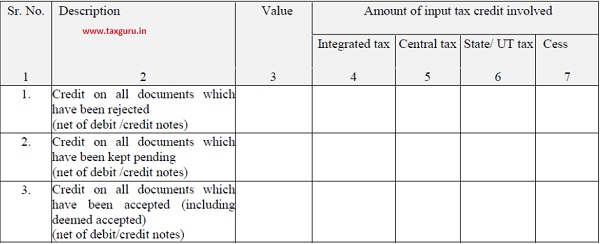

3.Inward supplies received from a registered person (other than the supplies attracting RCM) , imports and supplies received from SEZ units/Developers on Bill of Entry.

4.Summary of the input tax credit:

5. ISD credits received (eligible credit only)

Instructions (FORM GST ANX-2)

1. Details of documents uploaded by the corresponding supplier(s) [irrespective of the fact whether the supplier files his return on monthly or quarterly (Normal, Sahaj or Sugam) basis] will be auto-populated in this annexure on near real time basis and can be accepted or reset / unlocked by the recipient upto the 10th of the month following the month in which such documents have been uploaded. After that the procedure as outlined in Sr. No. 2 below will be applicable.

2. Recipient can take action on the auto-populated documents to – Accept, Reject or to keep pending on continuous basis after 10th of the month following the month in which such documents have been uploaded. However, in case of quarterly return filers communication of such rejected documents and any further action on such rejected documents shall be done only in the return for the next quarter.

3. Accepted documents will mean that supplies reported in such document have been received before filing of return by the recipient and the details given in the documents reported in FORM GST ANX-1 are correct.

4. Accepted documents would not be available for amendment at the corresponding supplier’s end. However, a separate facility to handle such cases will be provided.

5. For the purposes of the return process, any invoice with an error that cannot be corrected through a financial debit / credit note shall be rejected. For example-

(i) the recipient does not agree with some of the details such as HSN Code, tax rate, value etc. These are certain errors which cannot be corrected through debit/credit notes.

(ii) GSTIN of the recipient is erroneous and therefore, it is visible in the FORM GST ANX-2 of a registered person who is not concerned with the supply. These are certain errors which cannot be corrected through debit/credit notes.

6. Supplier can make corrections in the rejected documents through FORM GST ANX-1 as the rejected documents would be shown to the supplier.

7. Pending action will mean that the recipient has deferred the decision of accepting or rejecting the details of the invoices. There may be multiple reasons for the same such as supplies are yet to be received or the recipient decides that ITC is not to be taken for the time being etc.

8. The input tax credit in respect of pending invoices shall not be accounted for in table 4A of the main return (FORM GST RET-1) of the recipient and such invoices would be rolled over to FORM GST ANX-2 of the next tax period.

9. Pending invoices will not be available for amendment by the supplier until rejected by the recipient.

10. Any document, on which an affirmative action of either accepting the document or keeping the document pending or rejecting the document is not taken by the recipient in his FORM GST ANX-2, shall be deemed to be accepted upon filing of the return by him. Input tax credit on such deemed accepted documents shall be reflected / shown in table 4A of the main return (FORM GST RET-1).

11. Status of return filing (not filed, filed) by the supplier will also be made known to the recipient in FORM GST ANX-2 of the tax period after the due date of return filing is over. Recipients would be able to check the return filing status of the suppliers. This status, however, does not affect the eligibility or otherwise of input tax credit which will be decided as per the Act read with the rules made there under.

12. Trade name of the supplier will also be shown along with GSTIN. Legal name will be shown where trade name is not available.

13. Separate functionality would be provided to search and reject an accepted document on which credit has already been availed. Input tax credit availed on such document shall be shown for reversal in table 4B(1) of FORM GST RET-1 which may be adjusted in table 4A(11) of FORM GST RET-1 to arrive at the amount of input tax credit availed. However, such reversal of credit for the recipient will be with interest as per the provisions of the Act read with the rules made thereunder.

14. FORM GST ANX-2 will be treated as deemed filed upon filing of the main return (FORM GST RET-1) relating to the tax period.

15. The documents uploaded in FORM GST ANX-1 for month ‘M’ by a supplier who did not file his return for the previous two consecutive tax periods (M-1 and M-2 months)shall be made available to the recipient in FORM GST ANX-2 with an indication that the credit shall not be available on such documents. In other words, such documents will be visible to the recipient but the recipient cannot claim ITC on such inward supplies. However, the recipient can reject or keep such documents pending until filing of return by the supplier. For suppliers filing return on quarterly basis, this period will be one quarter i.e. if return of one quarter has not been filed, then recipient will not be able to claim credit on the invoices uploaded during next quarter.

Note – Table 3B and 3C shall be used after the data from the ICEGATE and SEZ (through ICEGATE) starts flowing to the GST system online. Thereafter, table 3J & 3K of FORM GST ANX-1 shall be discontinued. Data will be shown to the taxpayer as received from the ICEGATE.

Detailed notes on FOR GST RET-1(Monthly/Quarterly (Normal) Return.

3. Summary of outward supplies, inward supplies attracting reverse charge, debit / credit notes, etc. and tax liability.

4. Summary of inward supplies for claiming input tax credit (ITC)

5. Amount of TDS and TCS credit received in electronic cash ledger

6. Interest and late fee liability details.

7.Payment of tax.

7.Payment of tax.

8.Refund claimed from electronic cash ledger.

9. Verification

I hereby solemnly affirm and declare that the information given herein above,in FORM GST ANX-1 and FORM GST ANX-2 is true and FORM GST ANX-2 is true and correct to the best of my knowledge and belief and nothing has been concealed therefrom.

Place-

Date-

Signature

Name of Authorized Signature

Designation/Status

A. General Instructions:-

1. Facility to file Nil return through SMS will also be available if no supplies have been made or received.

2. After uploading details of supplies in FORM GST ANX-1 and taking action on the documents auto-populated in FORM GST ANX-2, the tax payer shall file the main return in FORM GST RET-1.

3. Information declared through FORM GST ANX-1and FORM GST ANX-2 shall be auto-populated in the main return (FORM GST RET-1).

4. The supplier can report excess tax collected from the recipients, if any, in the main return (FORM GST RET-1) under any other liability in Sr.No.8 of table 3A.

5. Rejection of the details of documents wrongly uploaded by supplier , pendency of suppliers not received but available in the auto-populated details of documents, reversals, adjustments etc., shall be auto-populated in table 4.

6. Amount of TDS/TCS shall be credited in the electronic cash ledger which will be based on return filled in FORM GSTR-7 and FORM GSTR-8 by deductors under section 51 and persons required to collect tax under section 52 respectively.

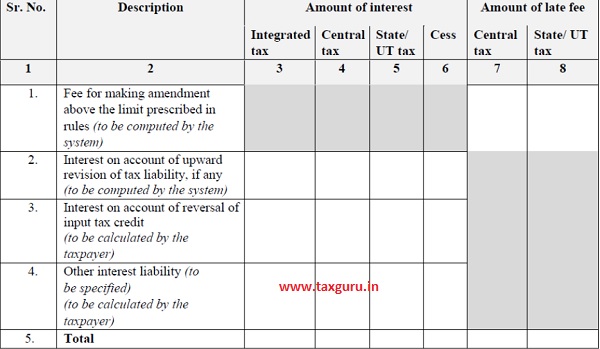

7. Interest and late fee to the extent of late filling of return, making late payment of taxes, uploading preceding tax periods, and invoices shall be computed by the system. Other interest due to reversals etc, shall be entered by the taxpayer on self-assessment basis.

8. Payment of tax can be made by utilizing ITC under the same head or cross-utilizing from other heads in accordance with the provisions of the Act read with the rules made thereunder. Balance payment of tax can be made in cash.

9. Suggested utilization of ITC will be made available in the payment table. However, taxpayer can make changes in the suggested ITC utilization as long as such changes are as per provisions of the Act read with the rules made thereunder.

10. Payment of tax on account of supplies attracting reverse charge, interest, fee, penalty and others shall be made in cash only.

11. Adjustment of negative liability of the previous tax period shall be allowed to be made along with the current tax period’s liability.

12. Viewing of the balance amount available in electronic cash and electronic credit ledger will be made available before making payment.

13. Value of inward supplies attracting reverse charge and import of services mentioned in table 3B will not be added to the turnover. Only the tax amount will be added to the computation of tax liability.

14. Facility of creating a challan for making payment will be made available if the balance in the electronic cash ledger is insufficient to discharge the liabilities.

15. Adjustment to liabilities or input tax credit relating to the period prior to the introduction of current system of return filing shall be reported in table 3 (tax liabilities) or table 4 (input tax credit), as the case may be.

B. Table specific instructions:-

| Table No | Part of the Table | Instructions |

|

3.

|

Summary Of outward supplies, inward supplies attracting RCM, Debit/Credit notes etc., and tax liability. | |

| A. Details of outward supplies | ||

| 1. | Taxable supplies made to consumers and un-registered persons will be auto-populated from table 3A of FORM GST ANX-1. The values will be net of debit/credit notes. | |

| 2. | Taxable supplies made to registered persons (other than those attracting RCM will be auto-populated from table 3B of FORM GST ANX-1. It includes all supplies made to persons having GSTIN or UIN. | |

| 3. | Exports made with payments of tax will be auto-populated from table 3C FORM GST ANX-1. | |

| 4. | Exports made without payment of tax will be auto-populated from table 3C of FORM GST ANX-1. | |

| 5. | Supplies made SEZ units/ developers with payment of tax will be auto-populated from table 3D of FORM GST ANX-1. | |

| 6. | Supplies made to SEZ units/developers without payment of tax will be auto- populated from table 3F of FORM GST ANX-1. | |

| 7. | Supplies made to registered persons which are treated s deemed exports will be auto-populated from 3G of FORM GST ANX-1. | |

| 8. | Liabilities relating to the period prior to the introduction of current return filling system and any other liabilities (including excess tax collected from the recipient , if any) to be paid shall be reported here by the taxpayer. | |

| B Details of inward supplies attracting reverse charge. | ||

| 1. | Inward supplies attracting reverse charge will be auto-populated from table 3H of FORM GST ANX-1 . The values will be net of debit /credit notes and advances on which tax has already been paid at the time of payment, if any. | |

| 2. | Import of services made during the tax period will be auto-populated from table 3-I of FORM GST ANX-1. The values will be net of debit / credit notes and advances on which tax has already been paid at the time of payment, if any. | |

| C.Details Of debit/credit notes issued , advances received/ adjusted and other reductions in liabilities. | ||

| 1. | Debit notes issued during the period in respect of supplies other than those attracting reverse charge will be auto-populated from the respective tables of FORM GST ANX-1. | |

| 2. | Credit notes issued during the period in respect of supplies other than those attracting reverse charge will be auto-populated from the respective tables of FORM GST ANX-1. | |

| 3. | Advances received on account of supplies of services during the period shall be reported by the taxpayer after giving effect to refund vouchers. The same may be used to adjust any advances reported wrongly earlier. | |

| 4. | Adjustment made out of advances reported earlier will be reported by the tax payer. Excess adjustment if any , made shall be accounted for in the next tax period’s return. | |

| 5. | Reduction in output tax liability on account of transition from composition levy to normal levy or any other reduction in liability shall be reported here by the taxpayer. | |

| D Details of supplies having no liability . | ||

| 1. | Supplies covered under GST but exempted from payment of tax or NIL rated shall be reported here. (For example, goods exempted under notification No.2/2017-Central Tax (ate) dated.28th June,2017, services exempted under notification No.12/2017-Central Tax (Rate) dated.28th June,2017 etc,). | |

| 2. | This is a residual entry for supplies not reported in any other column. Non-GST supplies and o supply specified in Schedule III shal be reported here. Supplies other than taxable and exempted /Nil rated supplies shall be reported here. However , it will exclude outward supplies attracting reverse charge. For the purpose of reporting here, non-GST supplies shall include supply of alcoholic liquor for human consumption, motor spirit (Commonly known, as petrol), high sped diesel, aviation turbine fuel, petroleum crude and natural gas. |

|

| 3. | Outward supplies attracting reverse charge on which tax is to be paid by the recipient shall be reported here. The values will be net of debit/credit notes. | |

| 4. | Supply of goods by SEZ units/developers to DTA on a Bill of Entry shall be reported here. This column is to be filled by SEZ units or developers only. | |

| E Total Value and tax liability. | ||

| 1. | Sum of part A,B,C and D will be the total value of supplies and that of liability and will be auto-computed. | |

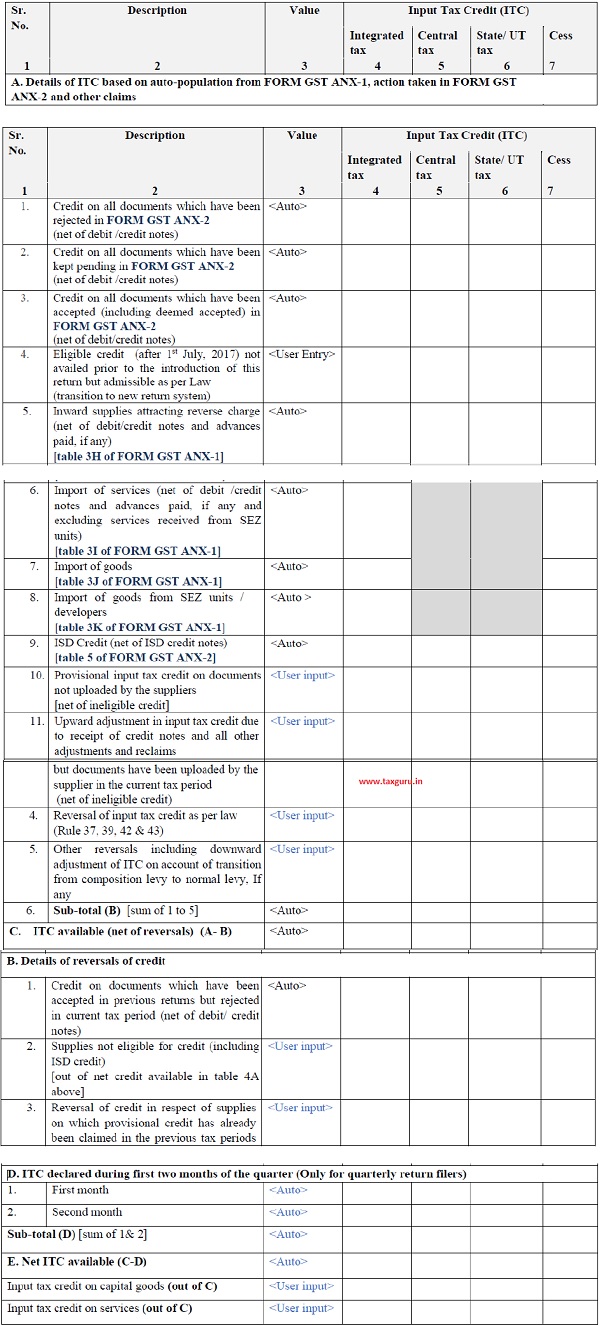

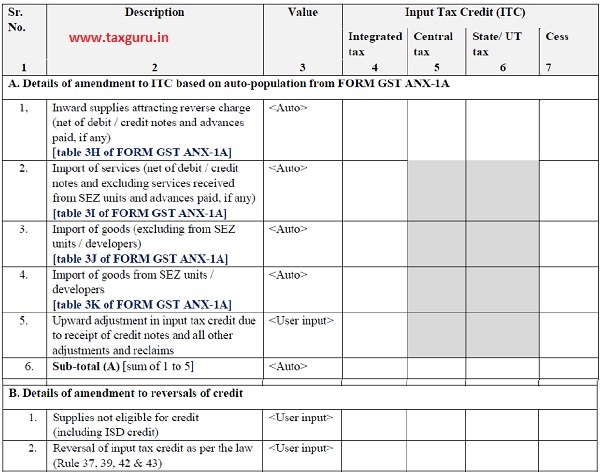

| A Details of ITC based on auto-populated from FORM GST ANX-1 and action taken in FORM GST ANX-2 and other claims. | ||

|

4.

|

1. | Amount of credit involved in the rejected documents in FORM GST ANX-2 before filing the return will be auto-populated here and will be net of debit/credit notes. |

| 2. | Amount of credit involved in the documents which have been kept pending in FORM GST ANX-2 will be auto-populated here and will be net of debit/credit notes. | |

| 3. | Amount of credit on all documents accepted (including deemed accepted)in FORM GST ANX-2 will be auto-populated here and will be net of debit/credit notes. | |

| 4. | If any eligible credit has not been claimed in FORM GST -3B due to non-receipt of supplies etc., the same can be claimed here. | |

| 5. | Credit on inward supplies attracting reverse charge as reported in table 3H of FORM GST ANX-1 will be auto-populated here and will be net of debit /credit notes and advances on which tax has already been paid at the time of payment, if any. | |

| 6. | Credit on import of services as reported in table 3-I of FORM GST ANX-1 will be auto-populated here. It will not include services received from SEZ units and will be net of debit/credit notes and advances on which tax has already been paid at the time of payment, if any. | |

| 7. | Credit on import of goods from overseas as reported in table 3 J of FORM GST ANX-1 will be auto-populated. It will not include goods received from SEZ units/developers. | |

| 8. | Credit on import of goods from SEZ units/ developers as reported in table 3K of FORM GST ANX-1 will be auto-populated. | |

| 9. | Credit distributed by ISD and reported in FORM GSTR-6 of the ISD as auto-populated in table 5 of FORM GST ANX-2 will be auto-populated here. | |

| 10. | Provisional credit on documents not uploaded by supplier(s) can be reported by the recipient for availing ITC to the extent provided in the Act red with the rules made thereunder. This ITC is other than that auto-populated in FORM GST ANX-2. | |

| 11. | i) There may be situations where a credit note was issued by the supplier against an invoice but the recipient had taken nil or partial credit on such invoice. Since acceptance of credit note will lead to reversal of credit, there may be instances where there will be a double reversal of credit for the recipient. In order to address the same, a facility has been provided for recipients to self-adjust any such loss of credit arising from issuance of credit notes by the supplier.

Illustrations: a) A supplier issues an invoice for Rs. 1000/- to the recipient in the month of May. The recipient accepts the invoice in his FORM GST ANX-2 and the credit involved in the said invoice gets auto-populated in his FORM GST RET-1. In the month of June, the supplier gives a credit note to the recipient who accepts the same in his FORM GST ANX-2. Upon acceptance of the said credit note, the credit involved therein is reversed and this gets reflected in FORM GST RET-1. No adjustment needs to be made in such a case. b) A supplier issues an invoice for Rs. 1000/- to the recipient in the month of May. The recipient accepts the invoice in his FORM GST ANX-2 but takes 50% credit on the said invoice in his FORM GST RET-1. In the month of June, the supplier gives a credit note to the recipient who accepts the same in his FORM GST ANX-2. Upon acceptance of the said credit note, the credit involved therein is reversed and this gets reflected in FORM GST RET-1. In such a case, the recipient may make an upward adjustment of 50% credit in this row as he had initially taken only 50% credit on the original invoice. c) A supplier issues an invoice for Rs. 1000/- to the recipient in the month of May. The recipient accepts the invoice in his FORM GST ANX-2 but takes no credit on the said invoice in his FORM GST RET-1. In the month of June, the supplier gives a credit note to the recipient who accepts the same in his FORM GST ANX-2. Upon acceptance of the said credit note, the credit involved therein is reversed and this gets reflected in FORM GST RET-1. In such a case, the recipient may make an upward adjustment of 100% credit in this row as initially he had not taken any credit on the original invoice. ii) Any other reclaim of ITC can also be reported here. |

|

–

| B Details | Reversals of credit. |

| 1. | If a document is rejected by the recipient after accepting and filing return of any tax period, then the value and amount of ITC will be autopopulated here, in the return filed immediately after such rejection. Credit availed on such document will be reversed. The amount will be net of debit / credit notes. |

| 2. | Out of the credit available in table 4A, the recipient shall report the amount of ineligible credit. ISD credit is also part of credit available in table 4A and shall also be taken into account accordingly for declaring ineligible credit. It shall not include any credit claimed in table 4A (10) in respect of supplies not uploaded by the supplier during the tax period which is already net of ineligible credit. |

| 3. | Documents of supplies uploaded subsequently by suppliers on which credit has already been claimed on provisional basis in the previous tax periods by reporting on self-assessment basis in table 4A(10) shall be reported by recipient here. As the credit was claimed on missing invoices on net of ineligible credit basis earlier, the values should be reported as net of ineligible credit only. |

| 4. | Reversal of input tax credit under rule 37, 39, 42 & 43 shall be reported here, if applicable. |

| 5. | Any other reversal including ineligible credit on import of services, downward adjustment of ITC on account of transition from composition levy to normal levy, etc. not covered by Sr. no. 1 to 4 shall be reported here. |

| C. | Input Tax Credit available after reversal. |

| 1. | Difference of credit available in table 4A and reversal of credit reported in table 4B will be the amount of credit available during the tax period. |

| D. | ITC declared during firs two months of the quarter ( only for quarterly return filers) |

| 1. | ITC declared during first two months of the quarter shall be auto-populated from FORM GST PMT-08 at Sr.No.1&2 for first month and second month respectively. |

| E. | Net ITC available |

| 1. | Difference of credit reported in table 4C and table 4D will be the net ITC available during the tax period and will be posted to the electronic credit ledger for utilization. |

| ITC on | Capital goods and services. |

| Out of credit available in table 4C, ITC claimed on capital goods and ITC claimed on services shall be reported here. |

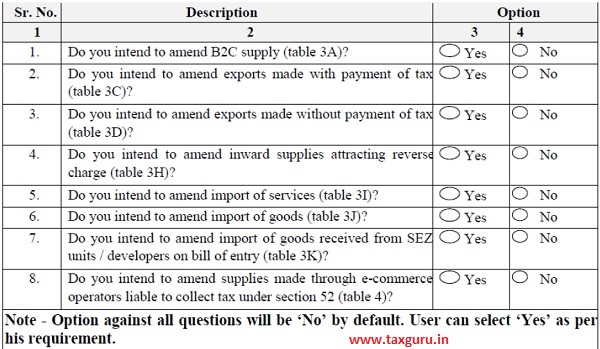

AMENDMENT TO FORM GST RET-1 (including FORM GST ANX-1).

Questioner for filing FORM GST ANX-1A i.e. Amendment to FORM GST ANX-1.

–

3. Amendment to the details of the outward supplies, inward supplies attracting reverse charge and import goods and services

4. Amendment to the details of the supplies made through e-commerce operators liable to collect tax under section 52.

Instructions ( FORM GST ANX-1A).

1. The amendment will be based on the tax period and for invoices/documents reported therein earlier.

2. If missing details of documents pertaining to the tax period “T” have been reported in the return of the tax period “T+n”, then amendment of such documents shall be made by amending return of the tax period “T”.

3. Amendment to FORM GST ANX-1 can be filed before the due date for furnishing f return for the month of September following the end of the financial year or the actual date of furnishing relevant annual return, whichever is earlier. The amendment to FORM GST ANX-1 can be filed as any times as provided in the Act read with the rules made thereunder.

4. Filing process will be similar to the processing of filling of return inform GST ANX-1. The annexure will be deemed to have been filled upon filing of return in FORM GST RET-1.

5. Amendment of invoice, debit/ credit notes shall be carried out through this annexure in relation to table 3A,3C,3D,3H,3 I , 3J and 3K of FORM GST ANX-1.

6. Providing original document details will be mandatory for amending the same except in case of B2C Supplies in table 3A, Table 3H and table 3 I of FOR GST ANX-1.

7. Missing documents of prior period (s) shall not be reported in this annexure but can be reported in FORM GST ANX-1 itself.

8. The invoices/documents on which refund has already been claimed by the supplier / recipient shall not be open for amendment.

9. For changing the value or any other particular under Table 4, the original GSTIN shall be re-entered as revised GSTIN and then the value or any other particular may be amendment.

10. Amendment in relation to table 3B,3E,3F and 3G shall be carried out in FORM GST ANX-1 of the maim return (FORM GST RET-1) itself.

3. Amendment to summary of outward supplies, inward supplies attracting reverse charge and tax liability.

4. Amendment to summary of inward supplies for claiming input tax credit (ITC).

5.Interest and late fee details.

6.Payment of tax.

Instructions filling of FORM GST RET-1A.

1. Filling process of amendment return will be similar to the filing process of original return FORM GST RET-1.

2. Entries made by the taxpayer in the main return (FORM GST RET-1) which were not auto-populated shall be editable in this return.

3. Amendment return can be filed for a tax period i.e. either a Month or a Quarter, as provisions of the Act read with the rules made there under.

4. Frequency of filling and period within which it is to be filed will be as per provisions of the Act read with the rules made there under.

5. Payment can be made if liability arises due to filing of amendment return. If liability becomes negative then no refund shall be paid. However, the negative liability becomes negative liability will be carried forwarded to the main return (FORM GST RET-1) of next tax period where adjustment can be made.

6. Payment process will be similar to that of the main return ( FORM GST RET-1). ITC available in the electronic credit ledger can be utilized for payment of liability as per the provisions of law read with rules made there under.

7. Revised values shall be reported wherever amendment is required in the returns already filled. For example, if the original value reported was Rs.100/- and revised value is Rs.120/- then Rs.120/- shall be reported in these tables.

8. Amendment to ITC (upward/downward adjustment ) shall be reported in the main return ( FORM GST RET-1) and not to be taken to the amendment return.

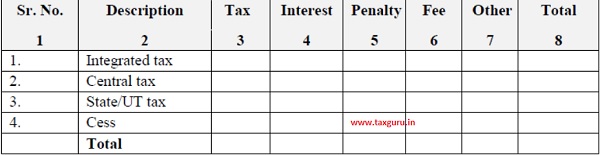

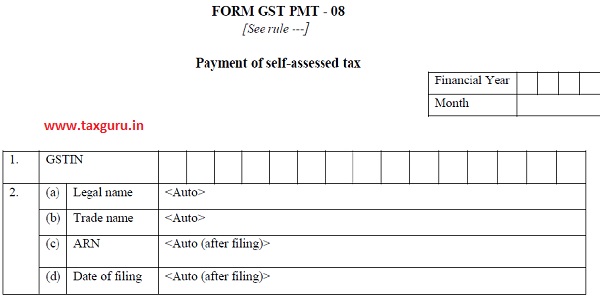

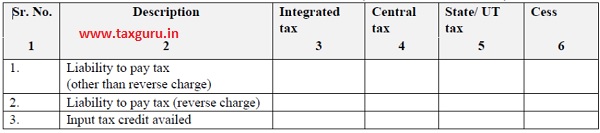

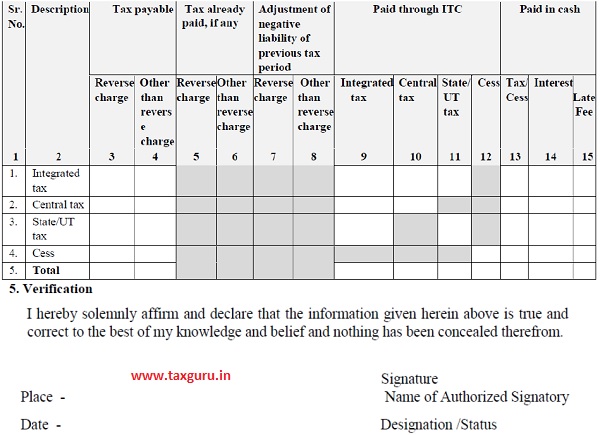

3. Summary of self-assessed liability and input tax credit (ITC) availed.

4. Payment of tax.

Instructions for fill up FORM GST PMT-08.

1. Taxpayers opting to file the return on quarterly basis have to make payment on monthly basis on the supplies made during the month.

2. Only eligible ITC shall be claimed through this FORM.

3. Payment of self-assessed liabilities shall be made for the first two months of the quarter.

4. Credit of the tax paid during the first two months of the quarter shall be available at the time of filing the return for the quarter.

5. Payment of the self –assessed liability shall be made by 20th of the month succeeding the month to which the liability pertains.

6. Liability can be settled out of balance in electronic credit ledger or electronic cash ledger as the case may be.

7. Liability and input tax credit availed shall be based on self – assessment subject to adjustment in the main return of the quarter.

8. Excess input tax credit claimed or short liability stated will be liable for levy of interest under section 50 of the Act.

9. The declaration shall also be required to be filed if no supplies have been made during the month.

10. Late payment will attract interest at the rate specified in section 50 of the Act.

Author Bio