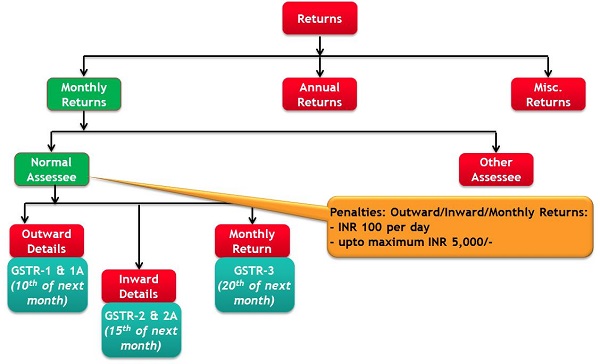

1) Return filing process for Normal Assessee:

1) Return filing process for Normal Assessee:

Step 1: Supplier (GSTR-1):

Cover all outward supplies effected during/in earlier tax period and submit GSTR-1;

Step 2: Recipient (GSTR-2):

- GSTR-2A (of recipient) shall be auto-generated based on GSTR-1 filed by Supplier;

- Following shall also be made available with recipient for preparation of GSTR-2

- Part-A of GSTR-2A showing inward supplies & DN/CN of suppliers;

- Part-B of GSTR-2A showing ITC transferred to recipient by ISD as per GSTR-6;

- Part-C of GSTR-2A showing TDS deducted by deductor as per GSTR-7;

- Part-D of GSTR-2A showing TCS collected by E-commerce operator as per GSTR-8;

- Recipient shall correct any mistake in GSTR-2 on basis of auto-populated GSTR-2 & 2A and BOA;

- Recipient shall mention ITC ineligible on inward supplies relating to non-taxable supply/ personal use of goods/ etc. in GSTR-2;

- Any correction made by recipient in GSTR-2 shall be auto populated and made available using GSTR-1A to the supplier for making corrections in GSTR-1.

Note: GSTR 1 relevant details are auto-populated in GSTR-2A which is visible to recipient and GSTR-2 relevant details are auto-populated in GSTR-1A which is visible to supplier.

Also Read- GST Enrolment – HSN Codes- Exhaustive List

Step 3: Monthly return (GSTR-3)

- Part-A of GSTR-3 shall be auto-populated from GSTR-1 & GSTR-2 details of Assessee;

- Pay Tax as per GSTR-3 & fill the details in Part-B;

- Apply for refund in Part-B in case of balance in Electronic Cash Ledger (option of Assessee)

Step 4: Mismatch Report (GST ITC-1) (Assuming compliance for August)

- Communication of mismatch to both supplier and recipient latest by last date of the month in which mismatch being carried out (by Sept. end);

- If rectification not done by ___ date, then Output liability of recipient would be increased by such amount succeeding the month in GSTR-3 in which discrepancy communicated (i.e. of Oct.);

2) GST Return – Miscellaneous Points

a) Reduction of Sales Value of Invoice – Process

- Issuance of Credit Note (CN) by Supplier;

- Insertion of details in GSTR-1 by Supplier;

- Acceptance of CN in GSTR-2A by recipient.

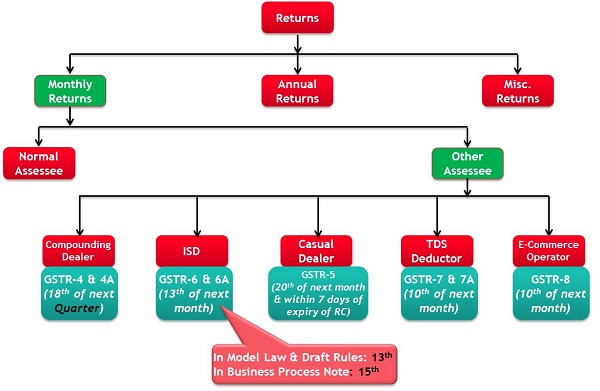

b) TDS Certificate shall be issued automatically in GSTR-7A on the basis of return filed by deductor in GSTR-7.

c) GSTR-1 (Sales Register)

- HSN Code Classification

| Condition | HSN Code required |

| Turnover in Preceding FY | |

| – Below 1.5 crore | Only description required |

| – Above 1.5 crore | HSN upto 2 digits |

| – Above 5 crore | HSN upto 4 digits |

| Voluntary | HSN upto 6/8 digits |

| Exports/ Imports | 8 digits |

- Accounting codes for Services is mandatory

- Requirement to mention Invoice level details:

| Transaction Type | Details required |

| B2B (Intra/Inter State transaction) | Invoice level details required |

| B2C :Inter State with Transaction value > 2.5 Lakh | |

| B2C :Inter State with Transaction Value < 2.5 Lakh | Summary details on basis of recipient required |

| B2C – Intra State Transaction |

d) GSTR- 2 (Purchase Register)

- Due date is 15th of the next month but data can be uploaded on daily, fortnight, weekly too.

e) GSTR-3 (Monthly Return Form)

- Part- A is fully automated;

- Only adjustment entries and challan information will be entered in Part-B;

- Cash ledger (tax deposit in cash and TDS/ TCS) will made separately for CGST , SGST and IGST

f) Mismatching:

- Any mismatch being rectified at a later stage would be shown in GST ITC-1;

- In case of reversal of interest paid on mismatch on account of rectification of returns, the refund amount shall be credited to electronic cash ledger in GST PMT-3

- The following case shall be assumed as no mismatch:

- If ITC claimed by Buyer is less than Output tax paid by Seller

- If Reduction of Output Liability by Supplier using Credit note is less than the ITC claim reduced in return by recipient.

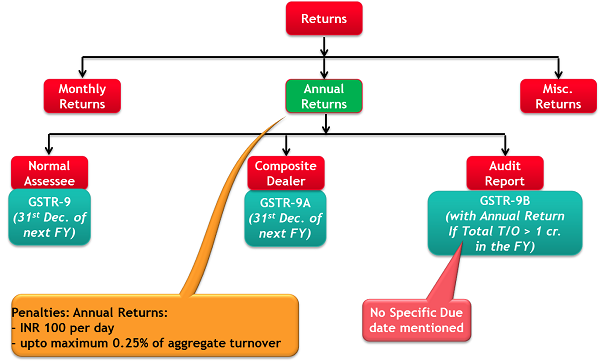

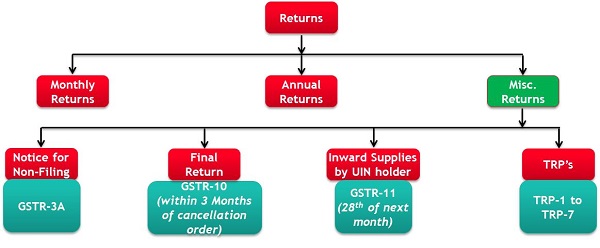

3) GST Return Forms and Due date of returns:

Hi Anshuman,

First, thank you for the compliments.

In regard to your doubt, would like to mention that the provisions as per Model Law (As mentioned in this article) are in contradiction with the Instructions as per GSTR-1 (As portrayed by your good-self).

However, as per meetings of GST Committee meeting on 30th Sept, the draft rules and forms were approved but the fine print would be available only after issuance of Act. Further, the Model Act itself is a draft and fine-print is still awaited.

Accordingly, this contradiction would probably be considered and resolved during the issuance of fine-print.

Sir,

First my compliments for writing the article in such a simple way for a complicated topic like this.

One doubt, you have mentioned that SAC is MANDATORY.

Is it not conflicting with the instructions in Form GSTR 1, as under :

INSTRUCTIONS for furnishing the information

4. HSN/SAC is NOT mandatory for taxable person whose aggregate turnover is less than 1.5 crores. HSN shall be restricted to maximum 8 digits. If

gross turnover in previous financial year is greater than Rs 5 crore, HSN should be minimum of 4 digits. If gross turnover in previous financial

year is equal to or greater than Rs 1.5 crore and less than 5 crore, HSN should be minimum of 2 digit and would be mandatory from the second

year of GST implementation. In case of Exports HSN should be 8 digits.

Kindly clarify and oblige.

Sir,

First my compliments for writing the article in such a simple way for a complicated topic like this.

One doubt, you have mentioned that SAC is MANDATORY.

Is it not conflicting with the instructions in Form GSTR 1, as under :

INSTRUCTIONS for furnishing the information

4. HSN/SAC is NOT mandatory for taxable person whose aggregate turnover is less than 1.5 crores. HSN shall be restricted to maximum 8 digits. If

gross turnover in previous financial year is greater than Rs 5 crore, HSN should be minimum of 4 digits. If gross turnover in previous financial

year is equal to or greater than Rs 1.5 crore and less than 5 crore, HSN should be minimum of 2 digit and would be mandatory from the second

year of GST implementation. In case of Exports HSN should be 8 digits.

Kindly clarify and oblige.