GST Registration: Caution, Compliance and Consequence in case of Defaults –Part-1

With the introduction of GST in India in July 2017, indirect taxation law has been drastically changed. Now, compliance and procedural part is same in whole India which was customized by each state (in VAT/ Sales Tax Regime) according to their needs before the introduction of GST Law. GST Law has been introduced with very harsh provisions, which has been liberalized to some extent by government according to demand of the economy still it is very harsh, if not adequate attention has been taken by traders to GST Provisions.

Currently, economy is facing the heat of slow down and traders are also getting very liberal because till date no actions are taken by GST Department against GST Defaulters because still after the passage of more than 2 years GST Portal is still running in hit and trial mode, because on the last date of GST Return Filing almost every month it creates problems.

In today discussion, I am going to elaborate some mandatory compliance under GST Law, which are not properly done by traders or incompletely done by traders due to unawareness of GST provisions and its penalty.

Registration process under GST has been made so simple that, even a normal person can do GST Registration itself due to which persons take GST Registration itself and due to unawareness of law becomes defaulter at later stage. Major Non Compliance and their consequence are given below:-

1. Furnishing of Wrong information at time of Registration: It was observed that, some persons are taking GST Registration on wrong address on the basis of rent agreement or taking GST Registration on premises from where they are not operating.

Consequence- Furnishing of wrong Information Attracts Section 122 (1) (xii) under which penalty can be levied is higher of Rs.10, 000/- or tax due from such person under per Act.

2. GST Return Filing: As on date, registered person has to file GSTR-3B on monthly basis and GSTR-1 on Monthly/Quarterly basis as applicable on him according to turnover, but major non compliance is observed at this part. Registered Persons are not filing their GSTR-3B and if they are filing GSTR-3B, in many cases they are not Filing GSTR-1.

Without filing of GSTR-1, counter purchasing party in not getting tax credit on purchase made by them. This is going to become very crucial matter from October 19 Month GST Return because as per recent notification dealers are not going to get GST Credit in excess of 20% of GST Credit reflecting in GSTR-2A while filing GSTR-3B

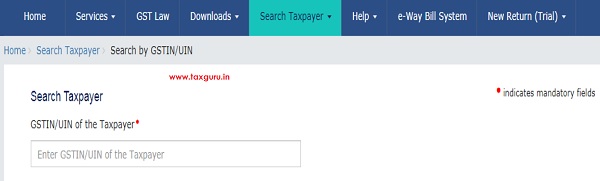

It is suggested to all registered persons that, before dealing with new vendor kindly check his GST return filing status from GST Portal – Search option, to avoid any litigation at later stage.

Consequence: Non Filing of GST Return (GSTR-3B) attracts a late fee of Rs.20/- Per Day in case of Nil Return and Rs.50/- Per day, other than Nil Return restricted to Rs.10000/-

3. Nil Return Filing: In many cases, it was observed that, dealers continually starts filing Nil Return even they are working under that GST number and receiving Payment also under their bank account, after taking GST Registration, now GST Department is taking care of them and starts sending Suo- Motto cancellation Order.

Consequence: Cancellation of GST Number and in case of fraud with Government (In case working firm and filing Nil Return), penalty may be levied is higher of Rs.10000/- or amount equivalent to tax/ input tax credit.

4. E-Way Bill –Non Issuance/ Wrong Issuance – After the implementation of E-Way bill, now it is mandatory for a registered person that, if they are sending goods from 1 state to other or within state, above a threshold limit (As specified) then it is mandatory to generate E-Way Bill. It was observed that, in many cases dealers are moving goods from 1 place to others; especially in case of Intra state transaction without generating E-Way Bill. In this situation, it must be noted that, dealer has to provide Bill wise detail in GSTR-1 from which it can be easily tracked, whether E-Way has been Generated or Not.

Consequence: Above situation may attract penalty u/s 122 (1) (xiv) or u/s 122 (1) (xviii) which is higher of Rs.10000/- or amount equivalent to tax/ input tax credit.

Further, this situation may also be considered U/s -129 of CGST Act, 2017 related to Detention, seizure and release of goods and conveyances in transit.

5. Wrong Business Premises Address: In GST Regime, currently GST Number has been allotted on the basis of Information provided at time of GST Registration and no physical verification of premises has been done before allotment of GST Number. Some dealers are misusing this option and taking GST Registration at wrong address or after change of address from 1 place to other, no amendment has been done in GST Records, to curb this situation some states as started conducting physically verification of premises on random basis.

Consequence: In such situation, it is observed that, GST Department issues show cause notice to the dealer and if not satisfied with reply or no reply is submitted, and then Issue suo-motto cancellation Order.

Further, it Attracts Section 122 (1) (xii) under which penalty can be levied is higher of Rs.10,000/- or tax due from such person under per Act

6. Stock Register and Sale/ Purchase Invoice: This default is commonly observed in case of small dealers, they are not maintaining stock register, which is an integral part of GST Compliance Part. Even, some dealers are not maintaining proper Sale/ Purchase Invoices records also, which is a penal offence under GST Law.

Consequence: This non compliance attracts, Section 122 (1) (xvi), under which penalty can be levied higher of Rs.10000/- or amount equal to the tax/input tax credit.

This article is for the purpose of information and shall not be treated as a solicitation in any manner and for any other purpose whatsoever. It shall not be used as a legal opinion and not be used for rendering any professional advice. This article is written on the basis of the author’s person experience and provision applicable as on date of writing of this article. Adequate attention has been given to avoid any clerical/arithmetical error, however; if it still persists kindly intimate us to avoid such error for the benefits of others readers.

The Author can be reached at mail –shivsharma786@gmail.com and Mobile/Whatsapp – 9911303737/ 9716118384

Author Bio