In terms of para 2.52 of the Indian Foreign Trade Policy (2015-2020) exports proceeds from Nepal and Bhutan can be realized in Indian rupees. However, in GST law, Export of Goods and Export of Services are treated differently

Rupee Exports of Goods to Nepal and Bhutan will be treated at par with export to any other country as definition of ‘export of goods’ under IGST Law attaches no condition other than ‘taking goods out of India to a place outside India’.

Sec 2(5) of IGST Act : “export of goods” with its grammatical variations and cognate expressions, means taking goods out of India to a place outside India;

However in case of export of services, in case export proceeds are received in Indian rupees, it will not qualify as ‘export’ as the definition of ‘export of services’ mandates receipt of payment in ‘convertible foreign exchange’.

Sec 2(6) of IGST Act : “export of services” means the supply of any service when,––

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service in convertible foreign exchange; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8;

Because of this controversy & confusion over payment realization for service exports, trade is representing for quite some time. For example for export of goods to these countries transport services are provided to Nepal / Bhutan importers by Indian transport companies and also for their exports to India. When these services are being provided to a place outside India from a place in India, a qualifying condition attached to in the definition of Export of Services is realization of payment in freely convertible currency. If the payment is not received in freely convertible currency, then such services will not be treated as exports and in such situations the service provider has to discharge the tax liability. Whereas as per treaty between these countries payments can be made in Indian Rupee.

Exemption on Supply of Services Associated with Transit Cargo to Nepal and Bhutan

To remove the confusion a Notification No. 30 / 2017, Central Tax (Rate), 29th September, 2017 was released to amend the Notification No. 12/2017- Central Tax (Rate), dated the 28th June, 2017 by exempting tax on Supply of services associated with transit cargo to Nepal and Bhutan (landlocked countries). But this notification served limited purpose.

Exemption to Supply of services having place of supply in Nepal and Bhutan, against Payment in Indian Rupees

Further the Central Government vide Notification No. 42/2017- Integrated tax(Rate) dated 27th October, 2017 made the amendment in the Notification No. 9/2017- Integrated Tax (Rate), dated the 28th June, 2017 whereby a new entry have been inserted in the exemption notification, namely, Supply of services having place of supply in Nepal or Bhutan, against payment in Indian Rupees.

Though this great relief was provided to the service providers to these two countries by way of exemption from GST, a missing point is related to availment of Input Tax Credit (ITC). If such services are exempted then ITC cannot be claimed.

Recommendations made by the GST Council in the 23rd meeting at Guwahati on 10th November, 2017

Exports of services to Nepal and Bhutan have already been exempted from GST. It has now been decided that such exporters will also be eligible for claiming Input Tax Credit in respect of goods or services used for effecting such exempt supply of services to Nepal and Bhutan.

Comment :

This is a welcome measure. The Notification is awaiting.

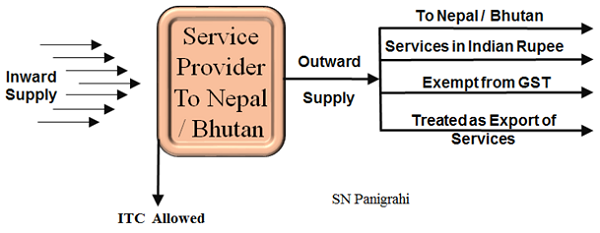

In a nutshell Service to Nepal / Bhutan shall be treated as Export of Services irrespective of realization of payment in Indian Rupee. Such services are exempt from payment GST and allowed ITC.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author Can be reached @ snpanigrahi1963@gmail.com

Author Bio

Dear sir

Please let us know the following

1.i am registerd dealer in GST-

2 want to send material to nepal/Bhutan

what will be the GST liability can we raise the Invoice with IGS Full tax amount

Please advise

I have properiter business man i have gst number how can i sold my second hand machinery to nepal or how can i make the invoice chaged igst or not what is the producers to send goods from road ways trasports what document reuired to send machinery

Dear Sir,

We export to Nepal with IGST.

We want to know that export to Nepal is exempted (No need tax on export to nepal) if yes in which section is applicable.

Please help me

Bal Kishan Sharma

9871594842

I dont have iec code Can i sale goods to nepal as customer is ready to pay gst

Sir,

Export goods to bhutan by Road Transport with payment of IGST. Now filing GSTR-1 and need shipping bill and bill of lading for refund. what to do for refund claim.

Dear Sir,

Whether notification to effect the following decision of GST Council has been issued? if so, kindly provide details.

Recommendations made by the GST Council in the 23rd meeting at Guwahati on 10th November, 2017

Exports of services to Nepal and Bhutan have already been exempted from GST. It has now been decided that such exporters will also be eligible for claiming Input Tax Credit in respect of goods or services used for effecting such exempt supply of services to Nepal and Bhutan.

(G Alagesan)

Hello sir,

you have told us which is important for ‘export of services to nepal’

very understandable….

and i think you have very good understanding about EXPORT TO NEPAL AND BHUTAN,

SO, I request to you for providing information about “HOW TO EXPORT GOODS TO NEPAL AND BHUTAN AND MOST IMPORTANT MATTER I.E. HOW TO GET REFUND OF IGST PAID ON SAID GOODS???”

I hope, you will provide such information very shortly through your ARTICLE…

Dear Mr. Panigrahi,

This has reference to your post “GST-on-export-of-services-to-nepal-and-Bhutan” wherein it has been concluded that GST is not applicable in case of Supply of Service to Nepal and Bhutan. I am into research and testing and we test products on behalf of clients. One of my client is based out of Nepal and Bhutan. They send their products to us in India for Testing. Testing is done in India. Kindly clarify if GST is payable/ applicable on the same. My client is drawing reference from this post and saying that GST is not applicable. My email is Satishpoddar@efrac.org

We export shipments from Bhutan to outside India . In that case some operation process done in Kolkata.

We charge shipper include GST , but Shipper doesn’t want to pay GST charge .Though CFS charges us GST amount.

So, make us confirm GST in case of Export shipment applicable or not.

dear sir

we are igst paid goods sale for nNepal

party accept materil & send me bill of lading,invoice copy

sir i want to claim the IGST refund for nepal Invoice in which we charge Igst amount

which process we should take in this matter plz help

Mukesh

I export the goods to Nepal . can i received

expor amount in indian rupees or neapli

convert money

In Gst export to nepal, how to make the invoice. Do we need to charge IGST or we need to make tax free using L.U.T scheme.

Can you help me under stand.

Is there any notification till date which allows the exporter of services to Nepal (against Indian currency), to avail Input credit. Because the general provisions don’t allow availment of credit on NIL rated supplies.

In case billing address was chennai and place supply was nepal , what is the procedure ???????

Dear Sir,

Bhutan export clearance under LUT ?

DEAR SIR,

FOR EXPORT TO NEPAL WHAT SHOULD WE MENTION IN GSTR1 PORT CODE

SIR WHAT DOCUMENT IS NEED FOR SUPPLY IN NEPAL I HAVE A SMALL UNIT OF SURGICAL BANDAGE I WANT TO SUPPLY IN NEPAL. SO I WANT TO KNOW THE DOCUMENT IS NEED TO SUPPLY IN NEPAL

My Company is in UAE and my sub contractor (vendor) is from mumbai and he is providing me exhibition services in Gujrat.

How will be treat in GST and what are the procedure?

Hello sir,

I am from Nepal. I am trying to import nephthalene balls from a factory in Raipur. Do I have to pay GST on it. What is the procedure for it….p

Dear Sir

What is the procedure of exports of Goods to Nepal & Bhutan if the export proceeds receive in INR . Will the exporter have to all the Custom Procedure to exports the goods ?

Can the exporter take the benefits of ” Export Obligation ” if the proceeds are received in INR ?

Kindly guide us in detiails

sir, i need to know whether LUT and/ or BOND is required in order to raise invoice with NIL GST for export of consultancy services to Nepal.

also, were architectural consultancy services exempted from charging GST for export of services to NEPAL?

I read your article on export of goods and services to Nepal and Bhutan

It is written in.very simple language and very detailed. One. I need to speak to you my cell no is 9167778782. Kindly give me a call or SMS me your contact detail.

Regards

Pawan Gupta

Manager Taxation.