GST on Joint development agreements (i.e Ratio deal)

A. Taxability in the hands of landowner

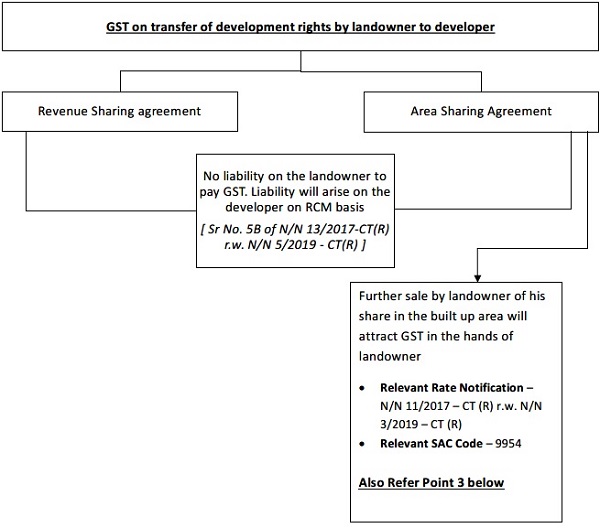

1. Landowner will transfer development rights of his land to the developer for development of residential or commercial apartments.

2. In consideration for transfer of development rights, landowner can get payment, either in terms of money (i.e revenue sharing) or in terms of share in built-up area (i.e area sharing) or a combination of both.

3. Item 5 (b) of Schedule II read with Item 5 of Schedule III needs to be considered while determining GST liability of landowner. Meaning thereby if the landowner sells his share after completion certificate or first occupation whichever is earlier, then on sale of such share no GST liability will arise.

B. Taxability in the hands of Developer

1. Landowner will transfer development rights of his land to the developer for development of residential or commercial apartments.

2. In consideration of transfer of development right, developer can pay, either in terms of money (i.e revenue sharing) or in terms of share in built-up area (i.e area sharing) or a combination of both.

3. Development rights given for construction of residential apartments

3.1. Manner of calculating exemption

Amount of exemption =

GST Payable on TDR or FSI or both for construction of project × carpet ar. of residential apts.

Total carpet area of residential and commercial apartments in project

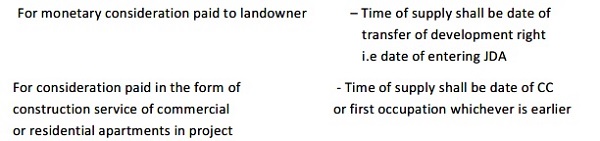

3.2. Time of Supply (Point of Taxation) of development rights

Liability of GST on TDR attributable to unsold residential apartments as on the date of CC shall arise on date of CC or first occupation, whichever is earlier. [N/N 06/2019 – Central Tax (Rate)]

3.3. Valuation of development rights

Value = Monetary consideration paid to landowner + Value of similar apartments charged by the developer from the independent buyers nearest to the date of transfer of TDR or FSI

[ Instruction 1A of N/N 12/2017 – Central Tax (Rate) read with N/N 04/2019 – Central Tax (Rate)]

3.4. How to calculate tax on development rights attributable to unsold residential apartments

GST shall be payable lower of A or B [ Sr. No. 41A of N/N 12/2017 – Central Tax (Rate) read with N/N 04/2019 – Central Tax (Rate)]

B. 1% of value of unbooked affordable residential apartments or 5 % of value of unbooked other than affordable residential apartments

Value shall be taken as value of similar apartments nearest to the date of CC or first occupation, as the case may be. [ Instruction 1B of N/N 12/2017 – Central Tax (Rate) read with N/N 04/2019 – Central Tax (Rate)]

3.5. GST Rate on development rights

a. SAC Code – 9972

b. GST Rate – 18%

Development rights given for construction of commercial apartments

4.1. Time of Supply (Point of Taxation) of development rights [N/N 06/2019 – Central Tax (Rate)]

4.2. Valuation of development rights

Same as point 3.3 above

4.3. GST Rate on development rights

Same as point 3.5 above

5. GST on construction service of apartments given to landowner by the developer for transfer of development rights

5.1. Time of Supply (Point of taxation) [N/N 06/2019 – Central Tax (Rate)]

Date of issuance of completion certificate (CC) or first occupation, whichever is earlier.

5.2. Valuation of such construction service

Value shall be equal to total amount charged for similar apartments in the project from the independent buyers, nearest to the date on which development right or FSI is transferred. [Instruction 2A of N/N 11/2017 – Central Tax (Rate) r.w. N/N 03/2019 – Central Tax (Rate)]

5.3. GST Rates [N/N 11/2017 – Central Tax (Rate) r.w. N/N 03/2019 – Central Tax (Rate)]

a. SAC Code – 9954

b. GST Rates- 1% , 5%, 12% (effective GST Rates) (1% – affordable residential apt., 5% – other than affordable residential apt., 12% – commercial apts.)

GST on Joint development agreements (wherein land is given by landowner to the developer for development of plots)

A. Taxability in the hands of landowner

1. GST on transfer of development rights

Landowner is not liable to pay GST. Developer will pay GST on RCM basis on such rights

[(N/N 13/2017 – Central Tax (Rate) r.w. N/N 5/2019 – Central Tax (Rate) ]

2. In consideration of transfer of development right, landowner can get payment, either in terms of money (i.e revenue sharing) or in terms of share in plots (i.e area sharing) or a combination of both.

3. When the landowner will sell his share of plots, no GST will arise as it is covered under item 5 of Schedule III (neither supply of goods nor supply of service)

B. Taxability in the hands of Developer

1. GST on transfer of development rights

1.1. Developer will pay GST on RCM basis on development rights given by landowner.

1.2. Time of Supply – Date of transfer of development rights i.e date of entering into JDA

1.3. Valuation of supply – Value of land on the date of transfer of development right

1.4. GST Rates – 18% (SAC code – 9972)

2. When the developer will sell his share of plots, no GST will arise as it is covered under item 5 of Schedule III (neither supply of goods nor supply of service)

Author Bio

in a RREP Project we have A B C wing Buildings and landowner allotted constructed flats in A & B wings and 2 Shops in C wing .

So my query is we have to pay gst on development rights in a residential if and only if on unsold portion ,if all the flats are sold before completion then it is exempt right?

Completion certificate should consider building wise or Project wise?

how to calculate value of those landowner flats as value of similar apartment means we should consider the same carpet area value sold to independent buyers?

commercial -shops allotted to land owner how we take proportion of commercial and value ?

My name is Ashvini. My sister, brother and I have a jda with a builder for a JV. it was area sharing and we got 7 flats out of 10. On completion do we the land owners have to pay gst and if yes what will be the value on which it has to be paid

what is the time of supply in case of a revenue sharing jda

SIR PLEASE CLARYFY TDS CONSEPT WAS THERE BEOFRE 01.04 .2019 OR ITS CAME EFFICTIVE FROM THE SAID DATE

VERY VERY VERY ………….. EXCELLENT ELABRATION ON JDA

TIME OF SUPPLY IS ON THE DATE OF CC ISSUED OR FC WHICHVER IS EARLIER

THANK YOU SIR

What is the difference between JDA (ratio deal) and JDA (wherein land is given by landowner to the developer for development of plots) ie the two cases have different GST rules?

EXCELLENT ARTICLE AND POST. LOT OF DOUBTS CLEARED. AFTER READING THIS ARTICLE I FELT LIKE GIVING BENGALI SWEET SANDESH TO SANDESH JAIN.

Thanks for the appreciation. Any feedback or correction on the post is welcomed