Analysis of GST Rates on Job Work

Few things which needs to be kept in mind before proceeding further

1. Do not take the meaning of job work in general sense

The definition of Job work is specifically given in section 2 (68) of the CGST Act, 2017 which says that “Job work means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “job worker”shall be construed accordingly.”

Therefore if the goods belong to an unregistered person (URP) then the activity of treatment or process doesn’t qualifies to be Job work.

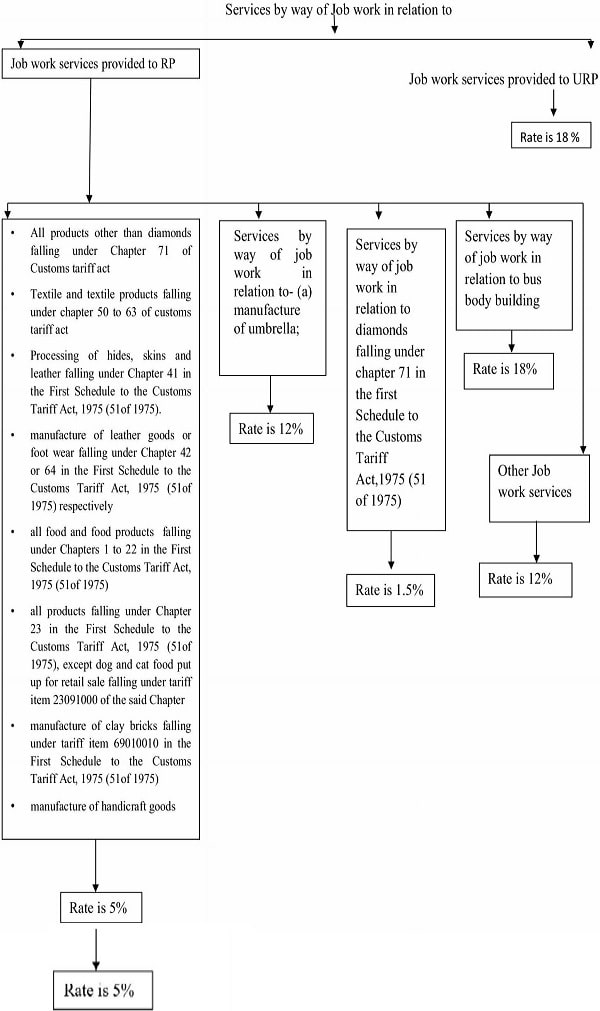

2. The above exhaustive defination of job work therefore generates the need to delve deeper into heading no 9988 of the Services Rate Notification No 11/2017 – CT (R)

3. Heading No 9988 of Rate Notification No 11/2017 – CT (R) cannot be read in casual manner. Therefore for any easy and in depth understanding the following analysis is provided -:

- Services by way of any treatment or process on goods belonging to another person, in relation to —

a) Printing of newspapers

b) Printing of books (including Braille books), journals and periodicals

c) Printing of all goods falling under Chapter 48 or 49, which attaract CGST @2.5% or NIL

Rate of GST is 5% (Irrespective of the fact whether such services are provided to registered person or unregistered person)

- Services by way of any treatment or process on goods belonging to another person, in relation to printing of all goods falling under Chapter 48 or 49, which attract CGST @ 6%

Rate of GST is 12% (Irrespective of the fact whether such services are provided to registered person or unregistered person)

- Tailoring Services — Rate of GST is 5% (Irrespective of the fact whether such services are provided to registered person or unregistered person)

- Services by way of printing of all goods falling under Chapter 48 or 49 [including newspapers, books (including Braille books), journals and periodicals], which attract CGST @6 per cent. or 2.5per cent. or Nil, where only content is supplied by the publisher and the physical inputs including paper used for printing belong to the printer.

Rate of GST is 12% (Irrespective of the fact whether such services are provided to registered person or unregistered person)

Author Bio

Job work to government agencies(URP) ,printing of school books which is tax free rate will be 5% ?

Since you are writing article on 17 Nov 2021, why aren’t you mentioned the latest rates under Chapter 48/49 which is 18%? Please clarify.

The GST rates have been changed wef 01/10/2021

I think there has been some misunderstanding. The GST rates have been changed w.e.f 01.10.2021 on certain “GOODS” falling under chapter 48/49. However my article is on Job work “SERVICES” on which there is no change in GST Rates w.e.f 01.10.2021

Sir,

Is it required to follow Job work procedure i.e. filing ITC-04 Return etc. for goods for which we have not taken ITC credit.

We are an Electricity Board. Electricity is exempted from GST. We have taken GST Registration for sale of scrap, for GST payment under RCM etc. We do not take ITC credit for Inputs viz Transformers, Poles, Cable, Conductors. We do not take ITC credit for Input services.

We frequently send Transformers for repair purpose. After job work the Transformers are returned back to us.

Are we required to follow Job work procedure for sending transformers for repair purpose and to file ITC-04 Returns.

Your valued opinion is requested

1. Firstly if you are sending goods for job work then it doesn’t matters whether you are

availing ITC or not. You have to comply with the provisions of job work i.e remove the

goods under the cover of delivery challan (Rule 55 challan) and furnish the details of all

such challans in Form ITC -04

2. Secondly, In my opinion, Repairing service does not amounts to Job work for the

reasons cited below-:

a. Service rate notification No 11/2017 (CT) (R) itself distinguishes between job work

and repair & maintenance by classifying Job work services under SAC code 9988

and repair & maintenance services under SAC code 9987

b. Job Work is processing or working upon goods supplied to the job worker, so as to

complete a part or whole of the process resulting in the manufacture or finishing of

an article or any operation which is essential for the afore-mentioned process but

repairing service signifies working on something which is already in existence and is

a contract for treatment or process for maintenance and removal of the defects.

3. Therefore in my opinion you need to send the transformers for the repair under the cover

of delivery challan (Rule 55 of the CGST Rules). However you are not required to file

Form ITC 04 as in my opinion repairing service doesn’t amounts to Job work.

Thank you very much for your detailed clarification sir.

As per your above diagram other job work Services Gst Rate is 12%, my doubt is when there is manufacturing process is involved i.e material is used for job work purpose what is the Gst rate on Job work. Ex: Zinc coating on steels the party sent Ms Steel for G.I.Purpose the Job worker used Zinc Ingots for G.I.Purpose and also for heating purpose power oil used, both products are consumed and not goes to the material but used for jobwork purpose. So I request you let me know the GST Rate is 12% or 18%.

Use of material by the job worker is irrelevant for determining GST rates on job work services. What matters is the registration status of your principal.

If your principal is registered in GST then GST rate on your job work services will be 12%

If your principal is unregistered in GST then GST rate on your job work services will be 18%.