INTRODUCTION:-

GST law provide two event i.e. Taxable event & Charging Event, Taxable event in GST is supply of goods or service or both whereas Charging event in GST is time of supply i.e. At what time GST liability is to be paid. GST will be payable on every supply of goods or services or both unless otherwise exempted. In other words GST is applicable only if transactions constitute the supply, if there is no supply no GST will charged. Before the discussion we need to know definitions related to this article.

DEFINITION:-

Goods:- As per the Section 2(52) “goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply.

Motor vehicle:- As per Section 2(28) Motor vehicle Act, 1988, “motor vehicle” or “vehicle” means any mechanically propelled vehicle adapted for use upon roads whether the power of propulsion is transmitted thereto from an external or internal source and includes a chassis to which a body has not been attached and a trailer; but does not include a vehicle running upon fixed rails or a vehicle of a special type adapted for use only in a factory or in any other enclosed premises or a vehicle having less than four wheels fitted with engine capacity of not exceeding [twenty-five cubic centimeters]

GST on sale of old and used vehicle by an individual (not engaged in any business):-

As we discussed above GST liability raised only in case of supply of goods or service or both. The term supply has been defined under Section 7 of the CGST Act,2017 and in order to constitute a supply the sale should be made by a person in the course of furtherance of business.

In case a used car is sold by any individual (not engaged in any business), for purchasing a new car, for a consideration, it cannot be said to be in the course of furtherance of his business, and hence does not qualify to be a supply. Hence sale of old car does not amount of supply, no GST thereon will be applicable irrespective of the fact whether such sale is being made to another unregistered individual or a registered person/car dealer.

GST on sale of old and used vehicle by a GST registered person:-

In cases of registered person sold used car to any person then without any doubt such a supply will be taxable under GST Law and such a person needs to pay GST at applicable rates.

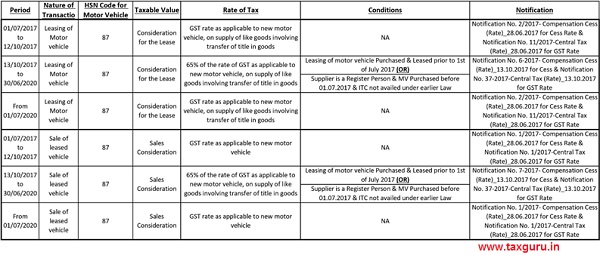

Rate of GST on leasing & Sale of Motor Vehicles-Notification No. 37/2017 – Central Tax (Rate)_13.10.2017:-

Notification No. 37/2017 – Central Tax (Rate)_13.10.2017 provides the abatement of 35% to the lesser who is into the business of leasing of motor vehicles. In other words, GST will be levied on 65% of the applicable GST Rate on such Motor Vehicles. The benefit of this notification shall available till 1st July, 2020 subject to fulfilment of below mentioned conditions,

Conditions:-

(I) Condition 1:- The Motor Vehicles was purchased by lessor prior to 1st July, 2017 and supplied on lease before 1st July, 2017.

(II) Condition 2:- i) The supplier of Motor Vehicle is a registered person.

ii) Such Supplier had purchased the Motor Vehicle prior to 1st July, 2017 and has not availed input tax credit of Central Excise Duty, Value Added Tax or any other taxes paid on such vehicles.

The above-mentioned Condition No. 1 is relevant to those who are in to the business of leasing of the Motor Vehicles. However, the second condition is applicable to all registered persons. It may be noted that the condition for Non-Availment of input tax credit is applicable to the dealers covered by condition no. 2 and not to the dealer covered by condition no. 1.

It may be noted that the leasing companies who have purchased the motor vehicle prior to 1st July, 2017 and supplied such vehicles on lease before 1st July 2017 and availed Input Tax Credit under VAT at the time of purchase of such vehicle will be liable to pay GST at the rate of 65% of the applicable GST Rate. Even though Input Tax Credit has been claimed under VAT on such Vehicles.

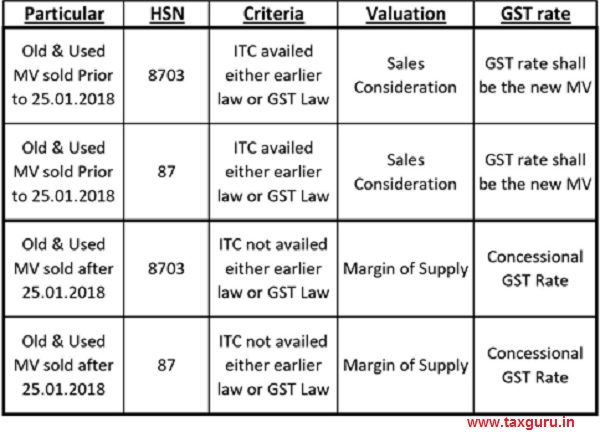

Reduction in GST Rate for sale of Old / Used Motor Vehicles-Notification No. 8/2018 – Central Tax (Rate)_25.01.2018:-

Major relief given by the government to the supplier of old / used Motor Vehicles through Notification No. 8/2018 – Central Tax (Rate)_25.01.2018. After the Implementation of GST Law, Old / Used Motor Vehicles were to be taxed at the same percentage of GST as applicable to New Motor Vehicle i.e. 28% plus Cess as applicable. To make old/used Motor Vehicle more affordable, on recommendation of GST Council, Government has issued Notification No. 8/2018 – Central Tax (Rate)_25.01.2018. Apart from that, Government also issued notification to exempt cess on sale of old/used Motor Vehicles i.e. Notification No. 1/2018-Compensation Cess (Rate)_25.01.2018.

Applicability:- The above said notifications are in effect from 25th January 2018. (This notification shall not apply in case of motor vehicles given on lease.)

Conditions:- The supplier of such goods has not availed input tax credit as defined in clause (63) of section 2 of the Central Goods and Services Tax Act, 2017, CENVAT as defined in CENVAT Credit Rules, 2004 or the input tax credit of Value Added Tax or any other taxes paid, on such goods.

Valuation:-

If Depreciation Claimed u/s 32 of Income Tax Act 1961:- In case of a registered person who has claimed depreciation under section 32 of the Income-Tax Act,1961(43 of 1961) on the said goods, the value that represents the margin of the supplier shall be the difference between the consideration received for supply of such goods and the depreciated value of such goods on the date of supply, and where the margin of such supply is negative, it shall be ignored.

In Other Case:- In any other case, the value that represents the margin of supplier shall be, the difference between the selling price and the purchase price and where such margin is negative, it shall be ignored.

Person Dealing In Buying And Selling Of Second Hand Goods (Rule 32(5) of CGST Rule 2017.):-

Where a taxable supply is provided by a person dealing in buying and selling of second hand goods i.e. used goods as such or after such minor processing which does not change the nature of the goods and where no input tax credit has been availed on the purchase of such goods, the value of supply shall be the difference between the selling price and the purchase price and where the value of such supply is negative, it shall be ignored.

Provided that the purchase value of goods repossessed from a defaulting borrower, who is not registered, for the purpose of recovery of a loan or debt shall be deemed to be the purchase price of such goods by the defaulting borrower reduced by five percentage points for every quarter or part thereof, between the date of purchase and the date of disposal by the person making such repossession.

This rule shall be applicable to those who deal in buying and selling of second hand goods. Hence, this shall be equally applicable to dealers in the business of buying and selling of Second Hand Motor Vehicles. Due to it is a special provision concessional rates of GST on sale of old vehicles would not be applicable on the outward supplies by such old & used car dealers and normal rate of GST would be applicable.

Payment of tax under reverse charge on purchase of used vehicle by a registered person from Government:-

As per Notification No. 4/2017-CT (Rate) Dated 28-6-2017 amended vide Notification No. 36/2017-Central Tax (Rate), dated 13-10-2017, w.e.f. 13-10-2017 in case of used vehicles, supplied by Central Government, State Government, Union territory or a local authority, the registered person receiving the supply is liable to pay tax under reverse charge.

In case of sale of used vehicles supplied by Government to unregistered person, respective department of Central Government, State Government, Union territory or a local authority should obtain GST registration and pay GST as per CBIC Circular No. 76/50/2018-GST Dated 31-12-2018.

Summary of the GST Rates on sale of Old/Used Motor Vehicles as per Notification No. 8/2018-Central Tax (Rate)_25.01.2018.

GST Implication to “Lessors”:-

GST Implication to “Other than Lessors”:-

Summary on Sale of Old & Used MV:-

GST Implication in present scenario:-

For Leasing of Motor Vehicles:-

Taxable Value:- Consideration for the Lease.

Rate of Tax:- GST rate as applicable to new motor vehicle, on supply of like goods involving transfer of title in goods.

For Sale of Leased Motor Vehicle:-

Taxable Value:- Sales Consideration.

Rate of Tax:- GST rate as applicable to new motor vehicle.

For New Motor Vehicle Dealer:-

Taxable Value:- Sales Consideration.

Rate of Tax:- GST rate as applicable to new motor vehicle.

For Old / Used Motor Vehicle Dealer (Second Hand Motor Vehicle Dealer):-

Taxable Value:- Margin of Supply (Provided ITC not availed either earlier law or GST Law) OR Sales Consideration (If ITC availed)

Rate of Tax:- GST rate as applicable to new motor vehicle.

For Old / Used Motor Vehicle sold by registered person (E.g. Motor car used by registered person for business purpose.):-

Taxable Value:- Margin of Supply (Provided ITC not availed either earlier law or GST Law) OR Sales Consideration (If ITC availed)

Rate of Tax:- Concessional Rate of GST (Provided ITC not availed either earlier law or GST Law) OR GST rate as applicable to new motor vehicle (If ITC availed)

DISCLAIMER:-

This is strictly my personal opinion. Above discussion cannot be considered as our professional or legal advice. Users shall consider legal provisions or take advice from experts before taking action on it.

Author Bio

I am planning to buy back the leased car from my own company which I was using for the last 4 years. The leasing company is invoicing me 28% GST () & 17% CESS on the buyback value. Is it a valid tax calculation? I understood that old cars should have 18% GST only. Please clarify and help in countering them incase they are charging me inappropriately