INTRODUCTION

Under the previous indirect tax regime, the Indian hospitality industry was liable to pay multiple indirect taxes such as VAT, Luxury tax and service tax. But with the commencement of GST regime, the Indian hospitality industry is expected to garner the benefits of standardized and uniform tax rates throughout the country. The industry can also get the benefit of better utilization of Input Tax Credit. It is expected that GST will reduce costs for customers, will harmonize the taxes as well as will help in reducing business cost.

Indian economy is going through the phase of rapid urbanization, increasing awareness of western lifestyle, empowerment of women. These resulted in higher disposable income which have than contributed to the enhancement of the growth of Hotel and restaurant industry. With the implementation of GST, it is expected that the industry is going to boom in the near future.

India’s Goods and Services Tax (GST) has brought a huge impact on the hospitality industry, whether you run a tiny guesthouse or a large luxury hotel. As we discuss about the Hospitality Industry, now days a number of services are added in the list of services provided by the hotel Industry previously.

Contribution to India’s GDP

- Tourism in India accounts for 7.5 per cent of the GDP and is the third largest foreign exchange earner for the country.

- The tourism and hospitality sector’s direct contribution to GDP in 2016, is estimated to be US$47 billion.

- The direct contribution of travel and tourism to GDP is expected to grow at 7.2 per cent per annum, during 2015 – 25, with the contribution expected to reach US$160.2 billion by 2026.

Hospitality & Tourism in Pre GST context

- Multiple taxes – VAT, Service Tax, Luxury Tax

- Concept of bundled services

- Cascading effect of tax

Hospitality & Tourism – under GST

- Benefits of standardized rates

- Easy & better utilization of input tax credit

- Better growth

- Clarity for consumers

- Administrative ease

SERVICES PROVIDED BY HOTELS IN INDIA

- Accommodation services

- Serving Food in Hotel Restaurant and in hotel room

- Cab services for tourist

- Foreign currency exchange service

- Renting out premises for events

- Food catering services

- Laundry services

- Business support services

- Personal Grooming & wellness services

- Food and beverage services at Indian Railways

- Food services through E commerce operator

- GST Rates of Hotels based on tariff FROM 1.7.2017 TO 30.9.2019

- Hotel Accommodation Service-GST Rates of Hotels based on tariff with effect from 1.10.2019

- COMPOSITION SCHEME FOR RESTAURANT

- Place of Supply-For Hotels

- Place of Supply-For Restaurants, Out door Catering Services

- Out door Catering/Mandap Keeper Services (GST Rates)

- Food ordered through e-commerce operator:

- Delivery fee charged bye-commerce operator from buyers

- GST liability on the ancillary services provided:

- TDS or TCS compliance:

- Cross Charge and ISD:

- Foreign Currency Exchange Services (Rule 32(2)(a&b))

Page Contents

- GST Rates of Hotels based on tariff FROM 1.7.2017 TO 30.9.2019

- Hotel Accommodation Service-GST Rates of Hotels based on tariff with effect from 1.10.2019

- COMPOSITION SCHEME FOR RESTAURANT

- Place of Supply-For Hotels

- Place of Supply-For Restaurants, Out door Catering Services

- Out door Catering/Mandap Keeper Services (GST Rates)

- Food ordered through e-commerce operator:

- Delivery fee charged bye-commerce operator from buyers

- GST liability on the ancillary services provided:

- TDS or TCS compliance:

- Cross Charge and ISD:

- Foreign Currency Exchange Services (Rule 32(2)(a&b))

GST Rates of Hotels based on tariff FROM 1.7.2017 TO 30.9.2019

| TARIFF PER NIGHT | GST RATE |

| LESS THAN 1000 | NO TAX |

| 1000-2499 | 12% with full ITC |

| 2500-7499 | 18% with full ITC |

| Greater than or equals to 7500 | 28% with full ITC |

Hotel Accommodation Service-GST Rates of Hotels based on tariff with effect from 1.10.2019

| Transaction Value per Unit (in Rs) per Day | GST Rate |

| Rs. 1000 and less | Nil |

| Rs. 1001 to Rs. 7500 | 12% with Full ITC |

| Rs. 7501 and above | 18% with Full ITC |

Comparison pre GST & GST

| PARTICULARS | AMOUNT | AMOUNT |

| Basic Room | Before GST | After GST |

| Room Tariff | 2700 | 2700 |

| Luxury Tax (say@10%) | 270 | – |

| Service Tax @9% | 243 | – |

| GST @12% | – | 324 |

| Total Bill | 3213 | 3024 |

COMPARISON OF PRE GST AND POST GST

| PARTICULARS | AMOUNT | AMOUNT |

| Room with complimentary breakfast | Before GST | After GST |

| Room Tariff | 2200 | 2200 |

| Complimentary breakfast | 500 | 500 |

| Luxury Tax (say@10%) | 220 | – |

| Service Tax @9% | 198 | – |

| VAT@14.5%(onfood) | 73 | – |

| GST@12% | – | 324 |

| Total Bill | 3191 | 3024 |

Comparison pre GST& GST

| PARTICULARS | AMOUNT | AMOUNT |

| Room with complimentary breakfast | Before GST | After GST |

| Room Tariff | 8000 | 8000 |

| Complimentary breakfast | 2500 | 2500 |

| Luxury Tax (say@10%) | 800 | – |

| Service Tax @9% | 720 | – |

| VAT @14.5%(on food) | 363 | – |

| GST@18% | – | 1890 |

| Total Bill | 12383 | 12390 |

IN THE GST ERA

| SL NO | Room Rent | GST Rate |

| 1 | All standalone restaurant irrespective of air conditioning | 5% without ITC |

| 2 | Food Parcels (or take away) | 5% without ITC |

| 3 | Restaurants in hotel premises having room tariff of less than Rs 7500 per unit per day | 5% without ITC |

| 4 | Restaurants in hotel premises having room tariff of Rs 7500 and above per unit per day(even for as ingle room) | 18% GST with fullI TC |

| 5 | Indian Railways Catering and Tourism Corporation Ltd. or their licensees/ Indian Railways | 5% without ITC |

| 6 | Out door catering services other than in premises having daily tariff of unit of accommodation of Rs7501 | 5% without ITC |

| 7 | Catering in premises with daily tariff of unit of accommodation is Rs 7501 and above | 18% with ITC |

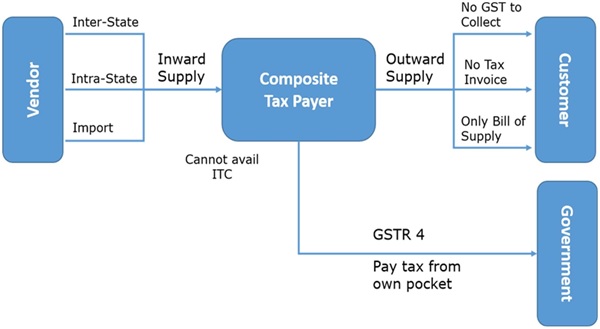

COMPOSITION SCHEME FOR RESTAURANT

| SL NO | CONDITION | ANSWER |

| 1 | Turnover Limit | 1.5.CRORE |

| 2 | Tax Rate | 5% |

| 3 | Other Condition | Should not been gaged in any services other than restaurant (special exception carved out for services like interest and exempt services)

Restaurant cannot make interstate outward supply of goods. Cannot supply any items exempt under GST. They cannot supply goods through a ne-commerce operator Restaurants cannot avail any input tax credit They can not collect taxes from the customer |

–

PLACE OF SUPPLY Section 12 of IGST Act 2017

How to determine place of supply in case of hotel industry:

| SL NO | PARTICULARS | PLACE OF SUPPLY |

|

1 |

Accommodation by a hotel, inn, guest house, home stay club or campsite (Section 12(3) of IGST Act 2017) | Location of immovable property |

| 2 | Accommodation by a hotel for organising marriage or reception or matters related there to official, social, cultural, religious, or business function | Location of immovable property |

| 3 | Any services ancillary to the above | Location of immovable property |

|

4 |

Restaurants or catering services, personal groomig, fitness, beauty treatment, health services (Section 12(4) of IGST Act 2017) | Location where services are actually performed |

Place of Supply-For Hotels

Case-1 Supplier, Recipient and Hotel property located in India

When supplier, recipient and hotel property is located in India–It shall be the place where the Hotel is located.(Sec 12 of IGST Act 2017)

Case-2 Supplier and Recipient are located in India but Hotel property is located out side India

When supplier and recipient property is located in India but hotel property is located out side India– It shall be the place of the recipient. (Sec 12 of IGST Act 2017)

Case-2 Supplier or Recipient are located out side

When supplier or recipient are located outside India–It shall be place where Hotel is located. (Sec 12 of IGST Act 2017)

Place of Supply-For Restaurants, Out door Catering Services

The place of supply of restaurant and catering services, person grooming, fitness, beauty treatment, health service including cosmetic and plastic surgery shall be the location where the services are actually performed [Sec 12(4)] of IGST Act 2017]

Restaurant service means supply, by way of or as part of any service, of goods, being food or any other article for human consumption or any drink, provided by are saturate, eating joint including mess, canteen, whether for consumption on or away from the premises where such food or any other article for human consumption or drink is supplied.

Out door catering means supply, by way of or as part of any service, of goods, being food or any other article for human consumption or any drink, at Exhibition Halls, Events, Conferences, Marriage Halls and other out door or in door functions that are event based and occasional in nature.

Hotel accommodation means supply, by way of accommodation in hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes including the supply of time share usage rights by way of accommodation.

Out door Catering/Mandap Keeper Services (GST Rates)

| SL NO | TYPE OF RESTAURANTS | GST Rate (upo 30/09/2019) notification no. 11/2017-CT (Rate) | GST Rate (with effect from 01.10.2019) Notification No. 20/2019-CT (Rate) dated 30/09/2019 amending the original notification no. 11/2017-CT (Rate) |

| 1 | Standalone catering services | 18%with ITC | 5% without ITC |

| 2 | Normal/composite outdoor catering within hotels (Where room tariff is less than Rs 7,500) | 5% without ITC | |

| 3 | Normal/composite outdoor catering within hotels (Where room tariff is more than or equal to Rs 7,500 | 18% with ITC |

Food ordered through e-commerce operator:

Cloud kitchens, delivery kitchens and or food delivery applications would be covered by the definition of e-commerce operators.

Most of the see-commerce operator sinter in to contracts with the restaurant owners and offer restaurant search and delivery services through their website or mobile application.

Customer places order by using their website or apps.

Aggregators are responsible to take customer order from the restaurant premises and deliver the food to end consumer.

The entire transaction in relation to food or daredevil e-commerce operator is divided into 2 parts: –

Food is delivered by thee-commerce operator’s hired/contracted delivery boy from restaurant premises to place of buyer. Bill of restaurant is handed over to the buyer

In this case GST charged by the restaurant will be rate of restaurant services, i.e.,5%.

Delivery fee charged bye-commerce operator from buyers

E-commerce operator will charge GST at 18% from customers on delivery charges collected from the customer and it shall not form part of restaurant services but would be classified under HSN9968, being apart of postal & courier service

| SL NO | Particulars | Amount (Rs.) |

| 1 | Room Tariff Charges | 10000 |

| 2 | Discount @ 30% | 3000 |

| 3 | Net Value | 7000 |

| 4 | GST @ 12% | 840 |

| 5 | Total payable | 7840 |

| 6 | Service fee of E Commerce Operator (40% of 3) | 2800 |

| 7 | GST on service fee @ 18% | 504 |

| 8 | Total bill of E Commerce Operator | 3304 |

| 9 | Net payable to hotel by E Commerce Operator | 4536 |

GST liability on the ancillary services provided:

Different treatments followed by different entities with respect to following services:

- Sale of Cigarettes and other tobacco products

- Sale of Hukkah

- In room dining

- Sale of cool drinks / aerated water

- Mini bar sales (sale of snacks, beverages, etc. which are already provided in the room)

TDS or TCS compliance:

- TDS provisions would be applicable for the services provided to Govt. departments, PSU, etc. Certain amount of GST would be deducted by such Govt. entities and file TDS returns.

- With effect from 1st October 2018, TCS provisions applicable for the bookings done through E- commerce Operators.

- The E-Commerce Operators shall collect one percent of the net value of taxable supplies made through it where the consideration with respect to such supplies is to be collected by the operator and file TCS Returns.

- Presently, most of the hotels are not aware of such provision.

- The hotel should check and accept the entries in the TDS and TCS returns filed by customer/e- commerce operators

- So that the amount would be credited to electronic cash ledger of the entity.

Cross Charge and ISD:

There would be temporary shifting/transferring of human resources from one entity to other entity/other branch of same entity in different State. There as on could be for staff shortage or for providing training, etc. GST needs to be discharged for the said services provided.

If the resources are sent outside it can have considered as export of service Subject fulfillment of conditions specified for export of services, with respect to common services received of the head office of the entity, the option of ISD needs to be examined for transferring the common credits to the respective units

Input tax credit related:

Section 17(5)(c) of CGST Act 2017 states that

Food, beverages, club memberships and others

ITC is not for the supply of following goods or services or both:

Food and beverages

Outdoor catering

Beauty treatment

Health services

Cosmetic and plastic surgery

However, ITC will be available if the category of inward and outward supply is same or the component belongs to a mixed or composite supply under GST.

ITC Provision for Hotel

- Hotels and Restaurants are different service providers.

- Therefore, Hotels can available ITC under the GST Act on the following inward supplies.

- All movable furniture like tables and chairs etc.

- Interiors and decorative items which are movable in nature etc.

- AC, Fans, DG Selts, Invertors, CCTV cameras and ele, items etc.

- Expenditure made for repair and maintenance of hotel building which is not capitalized.

- Other general inward supply like GST paid on bank charges, Insurance and Stationary, Security charges.

- Passenger lifts & Central Air Conditioning plant

- Motor car for transportation of customer

Reversal of credit

- Sec.17(2) read with rule 42 and 43 speaks that ITC is required to be reversed if exempted supply is provided by the registered taxable person.

- Sec.2(47)”exempt supply” means supply of any goods or services or both which attracts nil rate of tax or which may be wholly exempt from tax under section 11, or under section 6 of the Integrated Goods and Services Tax Act, and includes non-taxable supply;

- The Hotel cum restaurant is having big impact of the said provision and following circumstances creates lots of dilemma for them

- Accommodation services provided below Rs:-1000

- Sales of liquor from the restaurant-Non-GST Supply

- Restaurant service, banquet services and outdoor catering services where 5% tax is paid with no ITC

- Rent a cab service provided to the customer

- Whether all above services are required to be treated as exempted supply of services or not.

Rent a Cab for Tourists-

In cases where cab services provided by the hotels to their guests there is a option lying with hotel to provide the cab services as complimentary to them just like airport pickups and drop facilities are included in the package provided with the hotels or where cab are provided for the sightseeing of city or for intercity travel then the cab charges are to be paid by the service receivers extra apart from the accommodation charges. Now we have to ascertain the GST rate charged on the bill of cab, In such methodology, since the hotel/restaurant is providing one or more services to the guest as a mixed supply, the taxability of the consideration shall be decided based upon the principles of interpretation as provided in Section 8 of the Central Goods and Services Act, 2017.

Vide sub-section (74) of Section 2, if two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply then such supply is considered as Mixed and shall be treated as supply of that particular service which attracts the highest rate of tax. In the instant case, the accommodation service assumes the highest rate of GST and accordingly the rate of GST applicable to the accommodation service shall be applied on the entire consideration received from the guest.

1. Foreign currency exchange service- 18% GST with Full ITC

2. Renting out premises for events-18% GST with Full ITC

3. Food catering services-18% GST with Full ITC

4. Laundry services-18% GST with Full ITC

5. Business support services-18% GST with Full ITC

6. Personal Grooming & Wellness Services-18% GST with Full ITC

Foreign Currency Exchange Services pro Issues-Time of supply and advance receipt voucher/tax invoice

Whether cancellation charges collected from the customer will be treated as supply under the GST Act or not?

Hotel who has received advance of Rs:-1500/- per day per room prior to coronavirus pandemic and hotel has paid tax @ 12% on receipt of advance and after coronavirus pandemic if hotel have to give the said room below Rs.1000- What is the recourse with the hotel?

If in the above case tax invoice is prepared instead of advance receipt voucher Due care is required to take for adjustment of advance while filing GSTR 1 and GSTR 3B in case of hotel accommodation.

Foreign Currency Exchange Services (Rule 32(2)(a&b))

In case of currency exchange to its guest 18% with ITC Credit, but valuation shall be done as per valuation rules(b)

| Sl No | Currency exchanged | Value of Supply |

|

1 |

Up to₹1,00,000 |

1% of the Gross Amount of currency exchanged or Rs. 250 whichever is higher |

| 2 | Exceeding ₹1,00,000 and up to ₹10,00,000 | ₹1,000+0.50% of the (gross amount of currency exchanged–₹1,00,000) |

| 3 | Exceeding₹10,00,000 | ₹5000+0.1% of the (gross amount of currency exchanged –₹10,00,000) |

Or value shall be equal to the difference in the buying rate or the selling rate, as the case may be, and the Reserve Bank of India reference rate for that currency at that time, multiplied by the total units of currency

For example, on 20th September 2018, Mr. Aconverted USD 100 into INR 6,500 (INR 65 per USD). RBI‘s reference rate at the time of exchange was Rs.64. Now the value of supply will be:(65-64) *100=INR100.GST will be levied on INR 100.

If the RBI reference rate for a currency is not available, the value shall be 1% of the gross amount of INR provided or received by the person who is changing the money.

In above example, if the RBI reference rate is not available then 1% of INR 6,200 i.e INR 62 will be the value of supply of service and GST will be levied on INR 62.

SOME RELEVANT JUDGEMENTS

M/s. Safarire treat judgment of the Hon’ble Orissa HC

Safari Retreats Private Limited Vs Chief Commissioner of Central Goods & Service tax (Orissa High Court)

- Appeal Number: W.P. (C) No. 20463 of 2018 Date of Judgement/Order: 17/04/2019

- Where inputs are consumed in the construction of an immovable property which is meant and intended to be for the provision of taxable output services, whether input tax credit was available to the assesse?

Facts: M/s Safari Retreats Private Limited (“the Petitioner”) is engaged in carrying on business activity of constructing shopping malls for the purpose of letting out of the same to numerous tenant and lessees. The Petitioner purchased cement, steel, sand, aluminium, wires, etc., in bulk. Additionally, it also availed services like consultancy service, architectural services, legal and professional service etc. As these supplies were taxable, the Petitioner had accumulated input tax credit in respect of purchases of inputs and input services. It applied for availing credit, however, by applying section 17 (5) (d) of the CGST Act, the Revenue took a view that input tax credit shall not be available in respect of goods and services or both received by a taxable person for construction of an immovable property (other than plant and machinery) on his own account including when such goods or services or both are used in the course of furtherance of business. The benefit of input tax credit was denied to the Petitioner

M/s M/s Safari Retreats Private Limited

- Held that the very purpose of the Act was to make uniform provisions for levy, collection of tax and to prevent multi taxation. Considering the provision under section 17(5)(d), the narrow construction of interpretation put forth by the department is frustrating the very objective of the Act, inasmuch as the petitioner in that case has to pay huge amount of tax without any basis.

- In the instant case, the petitioner has retained the property and is not using it for its own purpose, but it is letting out the property, which is covered under the GST law, but still the petitioner has to pay huge amount of GST, to which he is not liable.

- In that view, the provision of section 17(5)(d) is to be read down and the narrow restriction as imposed, is not required to be accepted, the very purpose of the credit is to give benefit to the assessee.

- If the assessee is required to pay GST on the rental income arising out of investment on which it had paid GST, it is required to have the tax credit paid on inputs and input services.

M/S. Kusum Ingots & Alloys Ltd vs Union Of India And Anr on 28 April, 2004 (SC)

- CASE NO.: Appeal (civil) 9159 of 2003

- The court must have the requisite territorial jurisdiction. An order passed on writ petition questioning the constitutionality of a Parliamentary Act whether interim or final keeping in view the provisions contained in Clause (2) of Article 226 of the Constitution of India, will have effect throughout the territory of India subject of course to the applicability of the Act.

- Irrespective of above observation referred to above, it is in the nature of a precedent or an obiter, coming from the Apex Court, this would bind all subordinate Courts.

Pending litigation

- Bamboo Hotel and Global Centre (Delhi) Pvt. Ltd [W.P.(C) 5457/2019]

- The constitutional validity of the restriction under Section 17(5)(d) of the CGST Act Contention

- The CGST Act allows ITC to a person undertaking the construction of immovable property but not to a person renting out immovable property. By virtue of this judgment, ITC is being allowed on renting of immovable property service but not on the construction of property on own account. This dichotomy lacks the intelligible differentia and thus, is violate of Article 14 of the Constitution.

- Gogte Infrastructure Development Corporation Ltd. Advance Ruling

- No. KAR ADRG 2/2018 delivered on 21.3.2018

- the learned advance ruling authority was whether hotel accommodation and restaurant services provided to employees and guests of SEZ units could be treated as zero rated supplies under the Integrated Goods and Services Tax Acts, 2017?

- circular no. 48/22/2018 – GST dated 14.6.2018 wherein a contrary view has been expressed for short term accommodation, conferencing, banqueting etc. provided by restaurant

- Section 7(5)(b) of the IGST Act being a specific provision would prevail over the general provisions of place of supply and hence even accommodation services if provided to an SEZ unit will be an inter-State supply of services

Will construction of a lift/elevator be considered as an immovable property (where ITC is not available) or movable property or Plant & machinery (where ITC is available)?

Let us refer to the advance ruling in the case of Jabalpur Hotels Private Limited (Madhya Pradesh AAR) where a similar issue was raised.

Facts of the Case:-

Jabalpur Hotels Private Limited was incorporated with an object to construct Hotel in Jabalpur.

Company started construction of Hotel and completed a major part of its work.

The Hotel was in construction stage and the promoters of the hotel had some doubt on the issues of ITC and hence preferred to file Advance Ruling before the Authority.

This application sort advance ruling for input credit on Lift used in hotel.

The applicant sought ruling on availability of ITC of tax paid on Lift purchased and installed by the applicant in the hotel building, particularly with reference to blocked credit as defined under the provisions of Section 17(5) of the GST Act.

In the instant case based on the above observations, the AAR thus held that the applicant shall not be entitled to avail input tax credit of tax paid on procuring the lift to be installed in the hotel building, as the same is blocked in terms of Section 17(5)(d) of the CGST Act 2017, as the lift become an integral part of the building.

TUI India (P.) Ltd. [2019] 107 taxmann.com 414 (AAR – New Delhi)-Plce of Supply of Service in case of Hotel Booking

Facts-It is observed that booking of Hotel Accommodation is being done by the applicant on behalf of the clients as per their specific requirement. It has been submitted by the applicant that the invoice by the foreign Hotel Aggregator (M/s. DOTW) is being issued in the name of the applicant where name of the Hotel, the period of stay and name of the B2B or B2C client is also mentioned. However, the invoice to the client is issued by the applicant. Also, the applicant charges the same amount from Indian client for the Hotel Accommodation which is paid by the applicant to the foreign Hotel Aggregator i.e. DOTW. In addition, the applicant charges Service Fee/Convenience Fee from the clients which is retained by the applicant and is not remitted to the foreign Hotel Aggregator i.e. DOTW.

Held-Hence, from proviso to section 12(3) of the IGST Act, 2017, it is observed that if the location of hotel is outside India, the place of supply of hotel accommodation service is the location of recipient of service i.e., India. Hence, In this case, since, the applicant is covered in the definition of supplier and is located in India, even though the hotel is located outside India, the place of supply of service will be India.

Accordingly, applicant is liable to pay GST under Section 9(1) of the CGST Act, 2017, being taxable person as per Section 2(107) of the said Act In respect of the said supply. The supply of services by the applicant as an agent on behalf of DOTW cast a responsibility on the applicant to also collect and/or deposit GST on the taxable supply of goods or services, even, if they are acting only as an agent of DOTW. The contention of the applicant that they are acting as a pure agent and they are not supplying the said services on their own account are not relevant as they are admittedly acting as an agent of DOTW and agents are covered in the definition of “supplier” as per section 2(105) of the CGST Act, 2017, and are liable to pay GST as per Section 9(1) of the CGST Act, 2017.

Acharya Shree Mahashraman Chaturmas Pravas Vyavastha Samiti Trust [2019] 110 taxmann.com 282 (AAR – KARNATAKA)-Place of Supply incase the applicant is working as an intermediary

Regarding the sixth question, it is observed that the applicant intends to book hotel rooms to the pilgrims from outside and the supply of service is by the hotel to the pilgrims and the applicant is facilitating the supply of accommodation service to the pilgrims by the hotel.

16.1 The term “intermediary” is defined in clause (13) of section 2 of the Integrated Goods and Services Tax Act, 2017 as under:

‘(13) “intermediary” means a broker, an agent or any other person, by whatever name called, who arranges or facilitates the supply of goods or services or both, or securities, between two or more persons, but does not include a person who supplies such goods or services or both or securities on his own account’

16.2 It is not disputed that the applicant arranges the supply of services and facilitates the supply and hence would be squarely covered under the definition of “intermediary”.

16.3 Regarding the tax liability on the transaction, it is seen that the applicant collects’ the’ advance for booking of rooms on behalf of pilgrims from outside the Slate and acts as an agent of the pilgrims. The applicant holds the money and pays the consideration to the service provider at the end of the stay and in case of any balance, he would refund the same to the pilgrims. The payment is made on behalf of the pilgrim and the applicant does not hold any title to the services so procured and supplied and hence acts as a “pure agent” of the recipient of supply, only if the supplies procured by the applicant from the third party are in addition to the services he supplies on his own account. If he is a “pure agent” he is not liable to pay tax on the said turnover and if he is not supplying any service, then he would be a procuring agent for services and is liable to tax.

Case-4-Para 5.5.4 of Educational Guide 2012 regarding what if a service is not directly related to immovable property?

The place of provision of services rule applies only to services which relate directly to specific sites of land or property. In other words, the immovable property must be clearly identifiable to be the one from where, or in respect of which, a service is being provided. Thus, there needs to be a very close link or association between the service and the immovable property. Needless to say, this rule does not apply if a provision of service has only an indirect connection with the immovable property, or if the service is only an incidental component of a more comprehensive supply of services.

For example, the services of an architect contracted to design the landscaping of a particular resort hotel in Goa would be land-related. However, if an interior decorator is engaged by a retail chain to design a common décor for all its stores in India, this service would not be land related.

Examples of services which are not land-related

Repair and maintenance of machinery which is not permanently installed. This is a service related to goods.

Advice or information relating to land prices or property markets because they do not relate to specific sites.

Land or Real Estate Feasibility studies, say in respect of the investment potential of a developing suburb, since this service does not relate to a specific property or site.

Services of a Tax Return Preparer in simply calculating a tax return from figures provided by a business in respect of rental income from commercial property.

Case-5-Meaning of the Words “in relation to”– Doypack Systems Pvt Ltd v. Union of India: AIR 1988 SC 782:-

“49. The expression “in relation to” (so also “pertaining to”), is a very broad expression which presupposes another subject matter. These are words of comprehensiveness which might both have a direct significance as well as an indirect significance depending on the context…” “… In this connection reference may be made to 76 Corpus Juris Secundum at pages 620 and 621 where it is stated that the term “relate” is also defined as meaning to bring into association or connection with. It has been clearly mentioned that “relating to” has been held to be equivalent to or synonymous with as to “concerning with” and “pertaining to”. The expression “pertaining to” is an expression of expansion and not of contraction.” (emphasis supplied).

Case-ISPRAVA Hospitality (P.) Ltd.2020] (AAR – MAHARASHTRA)

Facts of the Case-

Applicant was proposing to give out entire Luxurious Villas, consisting of multiple rooms, on rent to various customers in the State of Maharashtra. The question is whether, as per Notification No. 11/2017-Central Tax (Rate) dated 28 June 2017, as amended, the entire Villa will be treated as ‘per unit’ or the individual rooms inside the Villas will be treated as ‘per unit’.

The applicant will be charging rent for the entire Villa and not as per room basis. Further, at any given point of time only one customer will be entitled to take the Villa on lease.

Observations by AAR

It was observed by AAR that applicant was treating entire Villa as one unit and therefore will give the same on rent to only one customer for any particular given date. In other words, two different clients will not be able to book the same Villa for the same period i.e. if the particular Villa is booked by one client at a given date then another client will not able to book the same Villa on the same day.

Further the applicant had no intention to rent out rooms inside the Villa, individually and therefore there was no question of the individual rooms being treated as ‘per unit’ as per the above said Notification.

The ‘pattern of renting’ in relation to usage of the property provides the context’ or ‘perspective’ in determination of unit of accommodation. In a hotel, a room constitutes ‘a unit’ whereas in a hostel, a bed may constitute ‘a unit’, as tariff is also declared accordingly.

In the present case applicant, themselves have mentioned that, rent is proposed to be offered to clients on per day basis for entire villa. The two different clients will not be able to book the same villa and there will be no option of booking particular room of the villa. Interested clients need to book the entire villa. Thus, it is crystal clear that villa per say is ‘indivisible unit’ in applicant’s business parlance, and the declared tariff is only for the villa as a whole. Hence, the expression “per unit” in the present case will be the entire villa.

Held

In the applicant’s case the entire Villa will be treated as “per unit” as specified under Entry no. 7 of the Notification No. 11/2017-CT’. (Rate) dated 28.06.2017

Gujarat ruling may add to meal costs’

The Gujarat Authority for Advance Ruling has said that supply of food services to canteens at industries and offices is in the nature of ‘outdoor catering’ and the buyer is liable to pay goods and services tax (GST) of 18%.

Under the GST regime, outdoor catering attracts 18% tax, while for canteen services it is 5%. However, there was confusion as to how food supplied to canteens through third-party catering should be treated and taxed.

According to experts, the issue was whether such supplies be treated as canteen services and taxed at 5%, or treated as outdoor catering and taxed at 18% under GST.

While it had been clarified that catering services to railways and educational institutions would be taxed at 5%, catering services to office and industry canteens had remained a grey area. Service providers were charging different rates leading to disputes with customers. Industry players had also sought clarification from the Finance Ministry and the GST Council on the issue, according to reports.

Rashmi Hospitality Services, an industrial canteen contractor, had been charging clients with in-house canteens at their factories, a GST of 18%. However, one of its customers had asked to be charged GST at 12%. Rashmi had moved the authority seeking clarification on the issue.

The authority ruled that Rashmi was providing service from premises other than its own to the client and that it should be treated as ‘outdoor catering service’ and taxed at 18%.

It also noted the expression of outdoor catering was not defined under the Central Goods and Services Tax Act as also that of the Gujarat Goods and Services Tax Act. However, the authority pointed out that in a judgement, the Allahabad High Court had observed that taxable catering service cannot be confused with who has actually consumed the food, edibles and beverages supplied by the caterer.

The High Court has also held that the taxability or the charge of tax does not depend on whether and to what extent the person engaging the service consumes the edibles and edibles supplied, wholly or in part, it added.

“The said Ruling would open up a Pandora’s box for industries as well as employees, with increased cost of meals for employees or for businesses; where the cost of meals is borne by businesses. The input tax credit is also not available,” Abhishek Jain, partner, EY, said.

He also pointed out that while the ruling by the authority was not binding on other States to follow, it definitely set a precedent on the vexing issue.

Impact on Indian Economy-

As an outcome of the lowered costs to end consumers, we can expect an increase in the consumption of services in this industry. At the same time, with compliance and regulatory hurdles easing out, we can hope to see a lower churn and increased profitability for the business owners. Both aspects combined, will result in distinct long-term benefits and possibly result in an increased contribution to the GDP by this sector. GST is a mixed bag of better and easier rules and regulations, and increased costs and compliances.