Gorakhpur Chartered Accountants Association has in made a representation to Local GST Authorities for not allowing them to visit GST offices to Chartered Accountants allegedly by Few advocates and it is learnt by us that same is still continuing.

Also Read: CAs authorised to Appear before GST Authorities- Gorakhpur Commissioner clarifies

Full text of their representation dated 13/02/2020 is as follows:-

Gorakhpur Chartered Accountants Association

To,

The Commissioner, UP Goods and Service Tax,

Gomti Nagar, Lucknow /

Additional Commissioner, Grade –I,

UP Goods and Service Tax, Taramandal, Gorakhpur /

Deputy Commissioner (Admin)

UP Goods and Service Tax, Taramandal, Gorakhpur

Sub: In the matter of Appearance of Chartered Accountants before the State GST Authorities at Gorakhpur

Dear Sir,

The Gorakhpur Chartered Accountants Association is a body consisting of practicing CA members from Gorakhpur and surrounding areas.

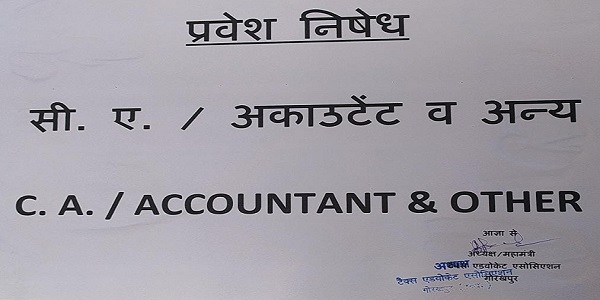

We would like to to bring to your kind notice that some of the advocates are regularly resisting forcefully to the member Chartered Accountants to enter the department’s premises and restricting practicing Chartered Accountants to appear before the State GST Authorities at Gorakhpur and to discharge their functions as Authorized Representative.

Sir, in this connection we would like to draw your kind attention towards our written representation submitted by our Association to Addl. Commissioner, Grade –I and Deputy Commissioner (Admin), UPGST, Gorakhpur in a meeting with them with our office bearers on 14.01.2020 wherein we have clarified our stand with regard to the appearance of Chartered Accountants before VAT/State GST Authorities citing the legal provisions of the statutes.

We have also sent our representation to the Tax Advocates Association, Gorakhpur to make them aware of our legal position to appear before the State GST Authorities as per the statutes.

We would also like to lay emphasis that the local authorities of the department have conceded to the legal provisions regarding appearance of Chartered Accountants in the meeting as aforesaid and the concerned local authorities have assured us that proper action will be taken to allow practicing Chartered Accountants to attend the office without any hindrances in future.

But it is regretful to mention that despite the assurance from the concerned local departmental authorities, our member Chartered Accountants are still resisted and prohibited by bunch of advocates to enter the department’s premises and to discharge their statutory functions on behalf of their clients.

LEGAL ASPECTS REGARDING APPEARANCE BEFORE GST AUTHORITIES:

In this connection, we would like to reproduce again the legal position regarding the appearance of Chartered Accountants under CGST/UPGST Act & Rules, which clearly empowers the Chartered Accountants expressly to appear before State GST Authorities.

Section 116 of UPGST Act, 2017–

Appearance by authorised representative

The Statutory Provisions of Sec. 116 referred above stipulates as under :

1) Any person who is entitled or required to appear before an Officer appointed under this Act, or the Appellate Authority or the Appellate Tribunal in connection with any proceedings under this Act, may, otherwise than when required under this Act to appear personally for examination on oath or affirmation, subject to the other provisions of this section, appear by an authorized representative.

(2) For the purposes of this section, the expression “authorised representative” shall mean a person authorised by the person referred to in sub-section (1) to appear on his behalf, being —

(a) his relative or regular employee; or

(b) an advocate who is entitled to practice in any court in India, and who has not been debarred from practicing before any court in India; or

(c) any chartered accountant, a cost accountant or a company secretary, who holds a certificate of practice and who has not been debarred from practice; or

(d) a retired officer of the Commercial Tax Department of any State Government or Union Territory or of the Board, who, during his service under the Government, had worked in a post not below the rank than that of a Group-B gazetted officer for a period of not less than two years.

Provided that such officer shall not be entitled to appear before any proceedings under this Act for a period of one year from the date of his retirement or resignation; or

(e) any person who has been authorized to act as a Goods and Services Tax Practitioner on behalf of the concerned registered person.

It is apparent form the reading of above that Section 116 provides for appearance by authorized representative in proceedings or appeals except in circumstances where personal appearance is required for examination or oath or affirmation. And “Authorised Representative” means –

— relative or regular employee

— Practising Advocate

— Practising CA, CWA or CS

— A retired government officer who had worked for not less than 2 years in a post not lower in rank than Group-B gazetted officer

— Goods and Services Tax Practitioner

Now we may conclude that after careful reading of the relevant statutory provisions mentioned here above, there remains no doubt whatsoever about the authority for Appearance of practicing Chartered Accountants before State GST Authorities.

And such, your honour is hereby requested to kindly bring the matter to the notice of all the concerned officers and advocates and their Associations on urgent basis to aware them all of relevant legal position so as not to resist the practicing Chartered Accountants from appearing and performing statutory functions as Authorized Representative before the State GST Authorities in future as per provisions of Section 116 of UPGST Act and CGST Act, 2017.

It is requested that necessary action may be taken in this regard at the earliest.

Thanking you,

(CA. Manish Mehrotra)

SECRETARY

Gorakhpur Chartered Accountants Association

Place: Gorakhpur

Dated: 13/02/2020

Encl : Copy of Representation submitted to the local authorities on 14.01.2020

*****

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

It is quite unfortunate that a section of the Ld. Advocates of Gorakhpur Region who resisted the CAs from entering the GST Ofice for pleading was fully ignorant of the basic Sec.116 of UPSGST Act, 2017. From such legal persons how a client can expect a fruitful and valid representation ? More over accountanc knowledge is the back boon of GST. To say, they do not the ABC of accountancy. Yes we have the monopoly over ACCOUNTANCY SUBJECT.

it is actually wrong procedure when chartered accountant require if every company /firm accountant

gst /sgst books of account not prepared by them what the chartered accoutant doing he is only for signature and every small big concerns are not emphasses the chartered accuotnat fees

ICAI and Council has been informed about the hindrance caused by TAA in appearance by CAs at GST Department, Gorakhpur with request for their taking up the issue suitably. Branch itself could do nothing officially in such matters, as per direction from ICAI and such members at large depend upon Council for help in this matter. Action from the Council in this serious matter is awaited to be shared with aggrieved members of Gorakhpur, deprived from right of practice at GST department. Hope that some thing positive will be shared soon because delayed justice is no justice after all.

Sir,

Please bring the Indian Penal Code’s provisions to the notice of advocate association’s that their act constitutes an offence under Section 339 indian penal code for causing “wrongful restraint” and is punishable under section 341 IPC which is triable by any judicial magistrate. Then they would cetainely like to avoid the conseuences of their illegal act.

Regards,

Virendra Sharma M-6395571172

Sir,

Please bring the Indian Penal Code’s provisions to the notice of advocate association’s that their act constitutes an offence under Section 339 indian penal code for causing “wrongful restraint” and is punishable under section 341 IPC which is triable by any judicial magistrate. Then they would cetainely like to avoid the conseuences of their illegal act.

Regards,

Virendra Sharma M-6395571172

*There should be some good ethics in every action of professional body. There is no such ethics seen evident in the action of ICAI since inception. All personal agenda of individual CA’s brought into action by CA Institute*

*Acting against transparency to bring monopoly is the only motto of Institute of Chartered Accountants of India*