Introduction to Budget 2021 – 22

The Goods and Services Tax (GST) has completed around 3 years of its implementation. GST has been recently known for increasing compliance burden on taxpayers in view of simplifying tax systems and making it online.

Further, GST was introduced with a motive to remove cascading effect by introducing a system of seamless flow of credit, however, the word “seamless” has been done away with due to insertion of various restrictions in form of Rule 86B, 36(4), 2A reconciliation and such others.

The Union Budget 2021 – 22 has finally announced on 1st February, 2021. From a taxpayer to a tax expert, everyone had some expectations from the Finance Minister, Smt. Nirmala Sitharaman.

Trade & Industry in view of hardships faced during this 3 years, expected department to be taxpayer-friendly system with an introduction of various measures in order to make it Truly “Good & Simple Tax”. The proposals made by Finance Minister are elaborated and analysed in detail in below paras.

(1) GSTR 1 be filed & Communication of Details – to avail Input Tax Credit [Clause 100]

A new clause (aa) to sub-section (2) of the section 16 of the CGST Act is proposed to be inserted to provide that input tax credit on invoice or debit note may be availed only when the details of such invoice or debit note have been

> furnished by the supplier in the statement of outward supplies and;

> such details have been communicated to the recipient of such invoice or debit note.

Analysis: –

Before insertion of clause (aa), recipient was supposed to file return u/s 39 of CGST Act, and supplier shall pay taxes so as to avail input tax credit.

With insertion of clause (aa), supplier is supposed to show the details of such invoice or debit note in GSTR – 1, then ITC would be eligible to recipient. The, communication clause was already mentioned in section 37(1) of CGST Act, however, now it has became the condition to avail ITC.

Such details will be communicated to recipient of supply, which can be seen in user services > Communication between taxpayers. Recipient is required to accept the same. In case of discrepancy a taxpayer can communicate with the recipient for issues like payment related issues or any other issue. In order to communicate with the suppliers, a taxpayer need to click on “Compose” tab.

(2) No requirement of GST Audit by CA / CMA u/s 35(5) [Clause 101 & 102]

As per section 35(5) of CGST Act, GST Audit is performed by CA / CMA if aggregate turnover exceeds specific limit (Rs. 5 crore for FY 2019-20). However, the said section is being proposed to be deleted, meaning thereby there would be no requirement of GST Audit to be done by CA/CMA.

A consequent amendment has been made in section 44 of CGST Act, so as to remove the mandatory requirement of furnishing a reconciliation statement (GSTR 9C) duly audited by specified professional and to provide for filing of the annual return on self certification basis.

It provides for the Commissioner to exempt a class of taxpayers from the requirement of filing the annual return.

Thus, GST Audit by CA / CMA would not be required once such section is notified. At present such provision is not notified. It is expected to be notified from FY 2021-22.

(3) Interest to be charged u/s 50(1) on Net Cash Liability [Clause 103]

CBIC has clarified that the amendment in Section 50 was made prospectively in view of technical limitations. Also it had clarified that no recoveries will be made for the past period to provide retrospective relief as decided by the GST Council.

Vide Finance Bill, 2021; government has finally proposed to give legal validity to charge interest on net cash liability retrospectively w.e.f 1st July, 2017.

Section 50 of the CGST Act is being amended, retrospectively, to substitute the proviso to sub-section (1) so as to charge interest on net cash liability with effect from the 1st July, 2017.

(4) Recovery in case of seizure & confiscation of goods & conveyance in case of Fraud shall be proceeded separately [Clause 104]: –

Section 74 of CGST Act, provides for assessment of person in case of fraud, wilfull misstatement, etc. For instance, as per section 64 of CGST Act, where the taxable person to whom the liability pertains is not ascertainable and such liability pertains to supply of goods, the person in charge of such goods shall be deemed to be the taxable person liable to be assessed and liable to pay tax and any other amount due under this section.

Thus, notice can be issued to person in charge of goods. Accordingly, the main person & person in charge of goods are separate.

As per explanation 1 to section 74, where the notice under the same proceedings is issued to the main person liable to pay tax and some other persons, and such proceedings against the main person have been concluded under section 73 or section 74, the proceedings against all the persons liable to pay penalty under sections 122, 125, 129 and 130 are deemed to be concluded.

However, Finance Bill, 2021 proposes to recover tax separately in for contravention under section 129 (Detention, seizure and release of goods and Conveyances in transit) & 130 (Confiscation of goods or conveyances and levy of penalty.)

Thus, now amended explanation provides that, where main person has paid taxes, then proceedings u/s 122 & 125 shall be deemed to be concluded (not for section 129 & section 130).

(5) Insertion of meaning of Self Assessed Tax [Clause 105]

Section 75 (12) of CGST Act, provides that where any amount of self-assessed tax in accordance with a return furnished under section 39 (GSTR – 3B) remains unpaid, either wholly or partly, or any amount of interest payable on such tax remains unpaid, the same shall be recovered under the provisions of section 79.

CBIC has proposed to clarify the meaning of self assessed tax by insering an explanation to Section 75(12), which states that, “self-assessed tax” shall include the tax payable in respect of details of outward supplies furnished under section 37 (GSTR – 1), but not included in the return furnished under section 39 (GSTR 3B).

Thus, due care shall be excersised while filing GSTR – 1, because the details filled in GSTR – 1 but short paid in GSTR 3B, would amount to self assessed tax not paid in GSTR 3B.

Other Aspects & Effects: –

> It is pertinent to note that if person has self-assessed its tax liability then he is required to pay the same within 30 days for becoming due, otherwise penalty will be levied even if paid before issuance of show cause notice (SCN) or paid within 30 days of issuance of SCN. [S. 73(11)]

(6) Enlarging the Scope of Provisional Attachement [Clause 106]

As per section 83(1) of CGST Act, there were only few cases where provisional attachement can be done i.e. where during the pendency of any proceedings under section 62 (Assessment of Non-filers) or section 63 (Assessment of unregistered persons) or section 64 (Summary assessment) or section 67 (Inspection, search & seizure) or section 73 or section 74.

However, vide Finance Bill, 2021 it has been proposed that, where, after the initiation of any proceeding under Chapter XII (Assessment), Chapter XIV (Inspection, Search, Seizure and Arrest) or Chapter XV (Demands and Recovery), the Commissioner is of the opinion that for the purpose of protecting the interest of the Government revenue it is necessary so to do, he may, by order in writing, attach provisionally, any property, including bank account, belonging to the taxable person or any person specified in Section 122(1A) of CGST Act (person who retains benefit of transaction), in such manner as may be prescribed.

With this, the government has enlarged the scope of provisional attachement which was limited to assessment pending section 62, 63, 64, 67, 73 & 74 to various chapters as enumerated above.

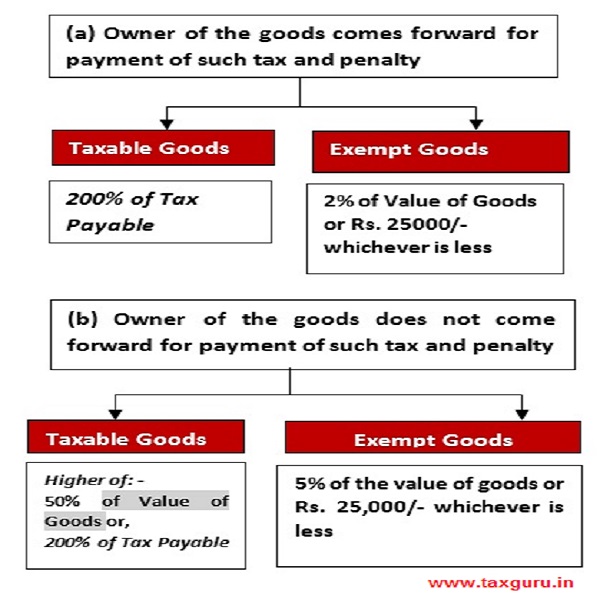

(7) Pre – Deposit for Appeal against detention, seizure and release of goods and conveyances in transit – 25% of Penalty [Clause 107]

A person appealing before appellate authority shall pay amount of Tax, interest, fine, fee & penalty, as is admitted, in full; and pre-deposit of sum equal to 10% of remaining amount of tax in dispute (not interest & penalty) (subj. to max Rs. CGST 25 crores, SGST 25 crores) before appeal. [S. 107(6)].

Vide, Finance Bill, 2021, a person appealing before appellate authority against order of detention, seizure & release of goods shall pay amount of 25% of penalty as pre-deposit.

(8) Plethora of Amendments in Section 129 of CGST Act [Clause 108]

If a person who has transport goods while in transit in contravention of provisions, such goods & conveyance in which goods were transported shall be liable for detention or seizure & shall be released on payment of below penalty or security: –

(2) The provisions of sub-section (6) of section 67 shall, mutatis mutandis, apply for detention and seizure of goods and conveyances. (Seeks to be omitted vide Finance Bill, 2021)

(2) The provisions of sub-section (6) of section 67 shall, mutatis mutandis, apply for detention and seizure of goods and conveyances. (Seeks to be omitted vide Finance Bill, 2021)

Notice to Pay Penalty be passed within 7 days of Detention or Seizure, Order to be passed within 7 days from service of such order [Section 129(3)]: –

The proper officer detaining or seizing goods or conveyance shall issue a notice within seven days of such detention or seizure, specifying the penalty payable, and thereafter, pass an order within a period of seven days from the date of service of such notice, for payment of penalty.

Disposal of Seized Goods or Conveyance to recover penalty [Section 129(6)]: –

Where the person transporting any goods or the owner of such goods fails to pay the amount of penalty within 15 days from the date of receipt of the copy of the penalty order, the goods or conveyance so detained or seized shall be liable to be sold or disposed of otherwise, in such manner and within such time as may be prescribed, to recover the penalty payable.

However, the conveyance shall be released on payment by the transporter of penalty as computed above or Rs. 1,00,000/-, whichever is less.

In case of perishable or hazardous in nature or are likely to depreciate in value with passage of time, the said period of 15 days may be reduced by the proper officer.

Tax & Interest on such goods can be determined without providing opportunity for being heard: –

As per section 129(4) of CGST Act, no tax, interest or penalty shall be determined under sub-section (3) without giving the person concerned an opportunity of being heard.

(9) Amendments in Section 130 of CGST Act [Clause 109]

Section 130 of CGST Act, was a non-obstante clause, meaning thereby Section 130 of CGST Act would prevail over other provisions of the act. Further, section 130 is punishable offence u/s 122 where penalty is Rs. 10,000/- or Amount Equal to Tax evasion whichever is higher.

In view of non-obstante clause, it would be difficult for government to levy penalty in excess of what provided in section 122 of CGST Act.

Vide Finance Bill, 2021, it is proposed to remove non-obstante clause from section 130.

(10) Amendment in Redemption Fine [Clause 109]

As per section 130(2), Maximum fine for redemption (release) of Confiscated Goods [S. 130(2) of CGST]

(a) Market value of the confiscated goods

(-) Tax chargeable thereon or,

(b) Penalty u/s 129(1) Penalty equal to 100% of the tax payable on such goods whichever is higher.

Maximum fine for redemption (release) of Confiscated Conveyance [S. 130(2) of CGST]

(No Change)

Tax payable on the goods being transported.

(11) Reduction in Penalty u/s 130 of CGST Act [Clause 109]

A person who was paying fine in lieu of confiscation of goods or conveyance was supposed to pay tax, penalty & other charges as well in view of section 130(3) of CGST Act. However, the said provision is proposed to be omitted vide Finance Bill, 2021.

(12) Power to Collect Statistics [Clause 110]

The Commissioner or an officer authorised by him may, by an order, direct any person to furnish information relating to any matter dealt with in connection with this Act, within such time, in such form, and in such manner, as may be specified therein.

(13) Bar on Disclosure of Information [Clause 111]

No information of any individual return or part thereof with respect to any matter given for the purposes of section 150 or section 151 shall, without the previous consent in writing of the concerned person or his authorised representative, be published in such manner so as to enable such particulars to be identified as referring to a particular person and no such information shall be used for the purpose of any proceedings under this Act “without giving an opportunity of being heard to the person concerned”

(Amendments are in Bold Italic & Strike through)

(14) Amendment in Section 168 of CGST Act [Clause 112]

Section 168 of CGST Act empowers the Competent Authority to issue orders, instruction or directions to the lower authorities to bring in uniformity in the implementation of the Act.

The purpose is to bring in uniformity in the implementation of the Act; and it is binding on all GST officers. There are various commissioners who are empowered to issue such orders, instructions or directions. Vide CGST Amendment Act, 2019; following Commissioners under section 44 (1) (relating to annual return) / 52(4) (relating to monthly TCS Return) / 52(5) (relating to annual return for ECO) are further being empowered to issue orders, instructions or directions.

Since section 44 will not have subsection after notifying the amendment, words subsection (1) is proposed to be deleted.

(15) Supply of goods by unincorporated association to members shifted from Schedule II to Section 7(1)(aa) (w.r.e.f. 1st July, 2017) [Clause 99 r/w 113]

It may be noted that determination of an activity as whether or not a supply is the task of schedule I r/w Section 7(1) of CGST Act whereas to classify a supply in goods or services is the department of schedule II.

Schedule II can in no way determine an activity as a supply if the same activity falls out of purview of schedule I.

Accordingly, the supply of goods by unincorporated association to its members is proposed to be shifted by inserting section 7(1)(aa) which would read as “the activities or transactions, by a person, other than an individual, to its members or constituents or vice versa, for cash, deferred payment or other valuable consideration.

Explanation.–For the purposes of this clause, it is hereby clarified that, notwithstanding anything contained in any other law for the time being in force or any judgment, decree or order of any Court, tribunal or authority, the person and its members or constituents shall be deemed to be two separate persons and the supply of 77 activities or transactions inter se shall be deemed to take place from one such person to another.

(16) Changes proposed in respect of Zero- Rated supply [Section 16 of IGST Act] [Clause 114]

“Zero rated supply” means any of the following supplies of goods or services or both, namely: –

(a) export of goods or services or both; or

(b) supply of goods or services or both for authorised operations to a Special Economic Zone developer or a Special Economic Zone unit

(Bold, Italics, underlined are proposed to be inserted)

Section 16(3) to only limited upto Zero rated supply under LUT: –

As per Finance Bill, 2021, following is proposed to be zero rated supply u/s 16(3) of IGST Act.

A registered person making zero rated supply shall be eligible to claim refund of unutilised input tax credit on supply of goods or services or both, without payment of integrated tax, under bond or Letter of Undertaking, in accordance with the provisions of section 54 of the Central Goods and Services Tax Act or the rules made thereunder, subject to such conditions, safeguards and procedure as may be prescribed.

As per proviso to section 16(3), the registered person making zero rated supply of goods shall, in case of non-realisation of sale proceeds, be liable to deposit the refund so received under this sub-section along with the applicable interest under section 50 of the Central Goods and Services Tax Act within 30 days after the expiry of the time limit prescribed under the Foreign Exchange Management Act, 1999 for receipt of foreign exchange remittances.

(Note: Government is only for supplier of goods)

Time Limit under FEMA [Regulation 9 of Foreign Exchange Management (Export of Goods and Services) Regulations, 2015: –

In ordinary case: The amount representing the full export value of goods / software/ services exported shall be realised and repatriated to India within nine months from the date of export.

However, where the goods are exported to a warehouse established outside India with the permission of the Reserve Bank, the amount representing the full export value of goods exported shall be paid to the authorised dealer as soon as it is realised and in any case within fifteen months from the date of shipment of goods.

Extension of period: Further the Reserve Bank, or subject to the directions issued by that Bank in this behalf, the authorised dealer may, for a sufficient and reasonable cause, extend the period of nine months or fifteen months, as the case may be.

For the purpose of this regulation, the “date of export” in relation to the export of software in other than physical form, shall be deemed to be the date of invoice covering such export.

The same has been made in line with Rule 96B of CGST Rules, 2017.

Further, government may prescribe,

(i) a class of persons who may make zero rated supply on payment of integrated tax and claim refund of the tax so paid;

(ii) a class of goods or services which may be exported on payment of integrated tax and the supplier of such goods or services may claim the refund of tax so paid.

Thus, it may be inferred that, government intends to reduce claims of refund on payment of integrated tax because, such claims are directly credited to bank account without in depth scrutiny of documents. Accordingly, it may prescribe classes of taxpayers who can claim such refund.

Furthermore, it may prescribe certain goods or services on which such refunds can be claimed.