Detailed Analysis of GST Notifications issued on 29th August, 2021 for Amnesty Scheme & Extension of time-limit to apply for revocation in certain cases

1.0 Late Fees Amnesty Scheme in respect of GSTR 3B for the period July, 2017 to April, 2021 increased from 31st August, 2021 to 30th November, 2021 [NN 33/2021 – CT dated 29th August, 2021]

Government has announced Amnesty Scheme for Late Fee Waiver in respect of returns on 1st June, 2021 in respect of below returns: –

- Form GSTR 3B (Notification 19/2021 – CT dated 1st June, 2021)

- Form GSTR 1 (Notification 20/2021 – CT dated 1st June, 2021)

- Form GSTR 4 (Notification 21/2021 – CT dated 1st June, 2021)

for the period July, 2017 to April, 2021 provided the same is filed between 1st June, 2021 to 31st August, 2021 as follows:

| Sr. No. | Nature of Return | Late Fee Capped under Amnesty Scheme |

| 1 | Nil Return | Rs. 500 per return (CGST – Rs. 250, SGST – Rs. 250) |

| 2 | Other than Nil Return | Rs. 1,000 per return (CGST – Rs. 500 & SGST – Rs. 500) |

By virtue of Notification 33/2021 – Central Tax dated 29th August, 2021, government has extended the time-limit upto which amnesty for reduced late fee in respect of GSTR 3B (not in respect of GSTR 1 & GSTR 4) can be availed. The last date to avail the late fee Amnesty Scheme is now extended to 30th November, 2021 instead of 31st August, 2021.

(Nil return does not means tax payable is nil, Nil returns means no details for furnishing in returns).

Impact & Analysis of Author:

(i) It is imperative to note amnesty has been provided on 1st June, 2021 for filing of GSTR 3B, 1, & 4 however, extension till 30th November, 2021 have been granted only for filing of form GSTR 3B.

(ii) The government is implementing Rule 59(6) of CGST Rules, w.e.f. 1st September, 2021. Upon the execution of the specified rule, the system shall check that prior to the furnishing of the GSTR-1/IFF of a tax-period the mentioned has been furnished or not:

a) GSTR-3B for the past 2-month tax periods (for monthly filers),

b) GSTR-3B for the past quarterly tax period (for quarterly filers) according to the concern. The system shall limit the filing of the GSTR-1/IFF till Rule-59(6) is complied with.

On tapping the submit button of GSTR-1 this check shall operate and the system shall provide you with the error message if the condition of Rule-59(6) has not been met. It might be noted that the records that have been saved in GSTR-1 shall get saved and furnishing of the records shall be allowed after the compilation of Rule-59(6).

Thus, from 1st September, 2021; if GSTR – 3B is not filed for 2 tax period (monthly) / 1 tax period (quarterly), system will not allow filing of GSTR – 1. So the first step assessee would be required to do is filing GSTR 3B at the earliest so that GSTR 1 can be filed so as to mitigate late fee on filing of GSTR 1. In a Nutshell, government has played a mischief by extending only GSTR 3B amnesty, even when the fact is clear that both goes hand in hand.

Author’s Comments: In my humble opinion, GSTR – 1 Amnesty should also be extended to 30th November, 2021 so as to benefit the taxpayers. Clarification is awaited on this aspect.

Further, on reading rule 138E of CGST Rules, it can be understood that if being a person other than composition person, has not furnished the GSTR 1 / IFF for any two months or quarters, as the case may be, shall not be allowed to generate E – way bill.

(iii) Government has not given due consideration to other filers of returns before 1st June, 2021. The government should ponder their attention in re-crediting the late fees paid by other registered persons so as to maintain equitability among taxpayers, otherwise it will lose the interest of timely filers.

2.0 Due date to Apply for Revocation of Cancellation of Registration fell between 1st March, 2020 to 31st August, 2021 extended to 30th September, 2021 [NN 34/2021 – CT dated 29th August, 2021]

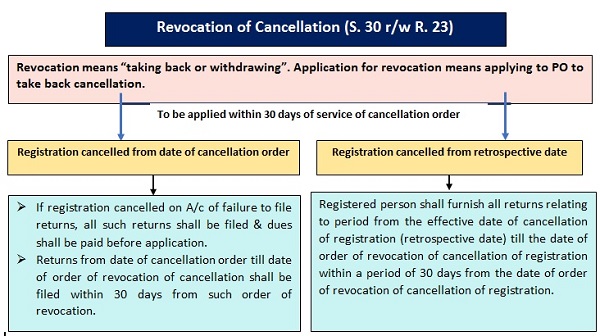

Preface to Revocation of Registration: Cancellation of registration is a two sided mechanism, meaning thereby, tax payer also can apply for cancellation or proper officer may also on his own motion cancel taxpayers’ registration (after following proper procedure). Provisions of revocation of cancellation comes into force when proper officer on his own motion decides to cancel the registration. Accordingly, the tax payer who do not want his registration to be cancelled, applies of revocation (taking back) of cancellation. Section 30 read with Rule 23 describes the procedure in relation to cancellation of registration.

Brief Note on Revocation: A brief summary of revocation procedures have been elucidated with below diagram:

|

Other points:

|

A taxpayer will only intend to apply for revocation when cancellation of registration has been done against his will. Thus, it is imperative to note when proper officer cancels the GST Registration of a taxpayer. As per Section 29(2) of CGST Act,

A. A registered person has contravened such provisions of the Act or the rules made thereunder as may be prescribed; or

Prescribed Contraventions [Rule 21 of CGST Rules, 2017]

The registration granted to a person is liable to be cancelled, if the said person,-

(a) Does not conduct any business from the declared place of business; or

(b) Issues, invoice or bill without supply of goods or services or both in violation of the provisions of this Act, or the rules made thereunder; or

(c) Violates the provisions of section 171 of the Act or the rules made thereunder (Anti-profiteering).

(d) Violates the provision of rule 10A (Furnishing of Bank details)

(e) Avails input tax credit in violation of the provisions of section 16 of the Act or the rules made thereunder; or,

(f) Furnishes the details of outward supplies in FORM GSTR-1 under section 37 for one or more tax periods which is in excess of the outward supplies declared by him in his valid return under section 39 for the said tax periods; or

(g) Violates the provision of rule 86B (Specified persons shall pay GST @ 1% in cash inspite of having ITC)

B. A person paying tax under section 10 has not furnished returns for three consecutive tax periods; or

C. Any registered person, other than a person specified in clause (b), has not furnished returns for a continuous period of six months; or

D. Any person who has taken voluntary registration under sub-section (3) of section 25 has not commenced business within six months from the date of registration;

E. Registration has been obtained by means of fraud, wilful misstatement or suppression of facts:

However, that the proper officer shall not cancel the registration without giving the person an opportunity of being heard.

Further during pendency of the proceedings relating to cancellation of registration, the proper officer may suspend the registration for such period and in such manner as may be prescribed.

As per Notification 34/2021 – Central Tax, where a registration has been cancelled under Section 29(2)(b) or 29(2)(c) [Non filing of returns] of CGST Act and the time limit for making an application of revocation of cancellation of registration under section 30(1) of CGST Act* falls during the period from the 1st March, 2020 to 31st August, 2021, the time limit for making such application shall be extended upto the 30th September, 2021.

*As per Section 30(1) of CGST Act, any registered person, whose registration is cancelled by the proper officer on his own motion, may apply to such officer for revocation of cancellation of the registration in the prescribed manner within 30 days from the date of service of the cancellation order.

However, such period may, on sufficient cause being shown, and for reasons to be recorded in writing, be extended

(a) by the Additional Commissioner or the Joint Commissioner, as the case may be, for a period not exceeding thirty days;

(b) by the Commissioner, for a further period not exceeding thirty days, beyond the period specified in clause (a). (Extension time is notified w.e.f. 1st January, 2021)

[Note: If appeal is already filed before appellate authority against cancellation order (due to lapse of time-limit to apply for revocation of cancellation order), the same cannot be withdrawn (even if application of revocation time-limit is extended) as GST portal does not allow to withdraw appeal unlike withdrawal of refund application functionality]

3.0 Extension in EVC Facility for filing GSTR 3B & GSTR 1 by companies [NN 32/2021 – CT dated 29th August, 2021]

The filing of Form GSTR 3B & GSTR 1/IFF by companies using electronic verification code (EVC), instead of Digital Signature Certificate (DSC) has already been enabled for the period from 27th April, 2021 to 31st August, 2021. The said period has been further extended to 31st October, 2021.

Author’s Comments: It shall be noted that, after Introduction of facility of Aadhar Authentication u/s 25(6A) to 25(6C) of CGST Act, the authorised signatories have gained authenticity, thus the signing of GSTR 3B/1/ IFF by DSC shall be scrapped out.

Relevant Press Releases/ Notifications:-

| Title | Notification No. | Date |

|---|---|---|

| CBIC extends 3 due dates under GST on 29th August 2021 | Release ID: 1750236 | 29/08/2021 |

| Due date of filing of application for revocation of cancellation of GST registration extended | Notification No. 34/2021-Central Tax [G.S.R. 600(E)] | 29/08/2021 |

| GSTR-3B Late fee amnesty scheme extended till 30.11.2021 | Notification No. 33/2021-Central Tax [G.S.R. 599(E)] | 29/08/2021 |

| CBIC allows filing of FORM GSTR-3B & GSTR-1/ IFF using EVC till 31.10.2021 | Notification No. 32/2021-Central Tax [G.S.R. 598(E)] | 29/08/2021 |

Revocation of GST registration is being done just like that. In order to restore its a nightmare. Is it part of ease of doing business?