Important Note: – Author in no manner through this article encourage any person to indulge in such activities. This article is only meant to understand the intent of law behind rule 86B which helps to curb fake invoicing.

Preface to Frauds under GST & Intent of Law to bring Rule 86B

Government with a motive to curb fake invoicing is taking a stringent steps by making changes in GST Law, which in turn has created chaos in Industry. Before praising / criticising the Rule, let us understand the Intent of law, its impact on industry and various taxable persons.

Inorder to decipher this rule, we must understand how frauds are taking place by fake invoices by taking an example.

Method 1: –

How Fraud Takes Place – Part 1

How do they actually do?

- FMCG Companies issues valid tax invoice on Departmental stores (in our example). Supposing, Rs. 100 plus GST Rs. 18

- Departmental stores sell this goods to B2C (i.e. consumer) at supposing 150 plus GST i.e., 177. However, consumer does not require tax invoice. Hence, now departmental store will issue tax invoice to FAKE Company having GST Number. Accordingly, fake company will avail ITC of such tax invoice.

- Fake company will make payment to Departmental Stores by NEFT / Bank means.

- The cash collected from consumer by departmental store will be given to fake company after retaining % of commission.

- Now, we know that fake company has Input Tax Credit.

- Now this fake company will find out certain firms which are in need of ITC to set off against their tax liabilities.

- Fake company will issue tax invoice to Needy firm. Needy firm will avail ITC & will pay certain % of commission to fake company to issue tax invoice.

This is how, fake company serves its purposes of taking fraud ITC & passing on to needy firms.

In order to curb these fake invoicing by fake companies, GST Law has been amended to insert rule 86B, let us understand how will it help in mitigating such evasions.

How do they actually do?

- Many suppliers purchase their products in white (i.e. with proper tax invoice), however the selling dealer might have to sell goods in cash to avoid payment of tax on value addition or as per market practice.

- It will result in accumulation of ITC to seller. Thus, he issues tax invoice on fake company with lesser profit than actual (pays GST on lesser value addition).

- Now fake company will have input tax credit. It passes on the fake ITC to the needy firms who are seeking to reduce their output tax liability by issuing fake tax invoice.

- Needy firms will pay commission to fake firm to pass on ITC.

Analysis of Rule 86B [Notification No. 94 /2020 – Central Tax dated 22nd December, 2020]

(1) Turnover > 50 Lakhs per month – 1% of Gross Output Tax Liability shall be payable in Cash: – As per rule 86B, notwithstanding anything contained in these rules, the registered person shall not use the amount available in electronic credit ledger to discharge his liability towards output tax in excess of ninety-nine per cent. of such tax liability, in cases where the value of taxable supply other than exempt supply and zero-rated supply, in a month exceeds fifty lakh rupees. (Proviso discussed below)

Analysis: –

1. Rule 86B overrides all other CGST Rules meaning thereby, even if any rule (e.g. R. 88B) asks for utilisation of ITC, rule 86B shall be followed if the same is applicable to an applicant.

2. As per the said rule, if a regd. person supplies taxable supply (NOT EXEMPT NOR EXPORT OF GOODS OR SERVICES WITH OR WITHOUT LUT) in a month more than Rs. 50,00,000/-, 1% of such tax liability shall be paid in Cash.

Example: –

If rate of Tax on certain product is 18%, & a firm is supplying taxable goods & services amounting to Rs. 60,00,000. The amount of Rs. 10,800 [Rs. 60,00,000 x 18% x 1%] shall be payable in Cash.

- Law only takes into consideration Taxable Supply, meaning thereby exports & exempt supplies do not attract GST.

3. It shall be noted that, fake companies also pay their GST but through input tax credit. The intent of law is to curb fake invoicing by requiring him to pay tax in cash.

4. The terms “such liability” shall mean Gross Liability on Taxable outward supplies, which would not include tax payable on procurements taxable under reverse charge mechanism payable in cash.

(2) Proviso to Rule 86B – Rule 86B not to Apply in certain cases: –

(a) The said person or the proprietor or karta or the managing director or any of its two partners, whole-time Directors, Members of Managing Committee of Associations or Board of Trustees, as the case may be, have paid more than one lakh rupees as income tax under the Income-tax Act, 1961(43 of 1961) in each of the last two financial years for which the time limit to file return of income under subsection (1) of section 139 of the said Act has expired; or

Notes: –

- If a regd. person had paid income tax of more than Rs. 1,00,000/- in preceding 2 financial years then Rule 86B shall not be applicable. Here, income tax payment shall be considered as paid even when paid through deduction of TDS. There is no requirement of payment being made only in cash (incl. bank).

- When MAT is payable (as per section 115JB) it shall also be construed as Income Tax.

- The government basically assumes that fake companies might not have paid income tax of more than Rs. 1,00,000/- in last 2 financial years. However, it is imperative to note that income tax of Rs. 1,00,000 would not be a big deal if a fake company is dealing in crores.

(b) the registered person has received a refund amount of more than one lakh rupees in the preceding financial year on account of unutilised input tax credit under clause (i) of first proviso of sub-section (3) of section 54; or

(c) the registered person has received a refund amount of more than one lakh rupees in the preceding financial year on account of unutilised input tax credit under clause (ii) of first proviso of sub-section (3) of section 54; or

Notes: –

- First proviso to section 54(3) stands for zero rated supplies made without payment of tax & second proviso to section 54(3) stands for refund on account of inverted duty structure. Thus, exporters claiming refund of ITC on export or inverted duty structure of more than Rs. 1,00,000/- in preceding financial year shall not be hit by rule 86B.

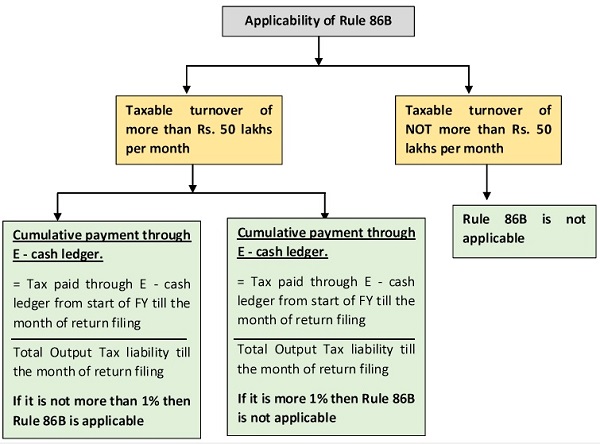

(d) the registered person has discharged his liability towards output tax through the electronic cash ledger for an amount which is in excess of 1% of the total output tax liability, applied cumulatively, upto the said month in the current financial year; or

Notes: –

- The said % has to be applied on cumulative basis. Let us take an example to understand the concept.

Month |

Sales(A) |

GST @ 18%(B) |

Cumulative Tax(C) |

Amount Actually paid thru Cash ledger(D) |

Cumulatively Paid(E) |

Cumulative %(F) = E/C |

Applicability of Rule 86B |

April |

58,00,000 |

10,44,000 |

10,44,000 |

25,000 |

25,000 |

2.3946% |

Applicable |

May |

52,00,000 |

9,36,000 |

19,80,000 |

5,000 |

30,000 |

1.5151% |

Not Applicable |

June |

75,00,000 |

13,50,000 |

33,30,000 |

12,450 |

42,450 |

1.2747% |

Not Applicable |

July |

85,00,000 |

15,30,000 |

48,60,000 |

– |

42,450 |

Less than 1% |

Applicable as sale is > than 50 Lakhs |

August |

44,00,000 |

7,92,000 |

56,52,000 |

– |

42,450 |

Less than 1% |

Not Applicable as sale is less than or equal to 50 Lakhs |

- In the above example, in case of May & June, since cumulative % of tax paid through E – cash ledger is more than 1% thus, rule 86B is not applicable as per clause (d) of proviso to rule 86B.

- In the month of July, since turnover of taxable supply is more than Rs. 50 lakhs & cumulative % of tax paid through e – cash ledger is not more than 1%, rule 86B would be applicable

- In case of August, since turnover of taxable supply is not more than Rs. 50 lakhs, rule 86B is not applicable, thus the question of checking of cumulative payment through e – cash ledger 1% does not arise.

- Tax payment of Reverse charge mechanism through E – cash ledger shall not be considered in computing 1% of output tax payment through E – cash ledger.

In a nutshell, in the following sequence a registered person shall check the applicability of rule 86B.

(e) the registered person is –

(i) Government Department; or

(ii) a Public Sector Undertaking; or

(iii) a local authority; or

(iv) a statutory body:

It is further provided that the Commissioner or an officer authorised by him in this behalf may remove the said restriction after such verifications and such safeguards as he may deem fit. Thus if a taxable person applies to commissioner then he may remove the restriction of rule 86B after due verification.

Other Aspects in relation to rule 86B: –

1. As per rule 59 of CGST Rules, a registered person, who is restricted from using the amount available in electronic credit ledger to discharge his liability towards tax in excess of ninety-nine per cent. of such tax liability under rule 86B, shall not be allowed to furnish the details of outward supplies of goods or services or both under section 37 in FORM GSTR-1 or using the invoice furnishing facility, if he has not furnished the return in FORM GSTR-3B for preceding tax period.

2. Rule 86A provides for blocking of input tax credit by proper officer if it is found that a registered person has availed fraudulent ITC. In light of NN 94/2020 – CT, if a person violates rule 86B i.e. pays in excess of 99% through Input Tax credit having taxable turnover more than Rs. 50 lakhs, proper officer has power to block the ITC utilisation of such persons.

Concluding Remarks: –

1. Government in order to curb tax evasion, has made stringent rules which in turn brings genuine taxpayers into ambit. However, as per proviso restrictions of rule 86B may not applicable to such registered person.

2. The said rule of 86B is not a full proof rule to stop fake invoicing however, such step would discourage fraudsters to engage in such rackets.

3. It is requested to genuine tax payers to not get panic due to insertion of this rule, as the intention of govt. is very clear to curb fake invoicing and not to target genuine businesses.

Then in your example what amount to be deposited in July Month, balance amount i.e. Rs. 6150/- (4860000*1%-42450) or Rs. 15300/- i.e. (1530000*%)

Hi Sir,

Please see the applicability in the month of Apr, cumulative tax discharge through electronic cash ledger is more than 1% Hope it should be not applicable. Anyway thanks for your detailed explanation.