1. Ineligible criteria to opt for Composition Scheme u/s 10(1) & 10(2A) [Clause 128 & Clause 129 of Finance Bill]:

As per Section 10 of CGST Act, below persons are ineligible to opt for composition scheme:

a) ……..

b) ……..

c) ……..

he is not engaged in making any supply of goods or services through an electronic commerce operator who is required to collect tax at source under section 52

e) ……..

f) ……..

Impact and Analysis:

It is proposed that only supplier of services through Electronic Commerce operator would be ineligible for composition scheme u/s 10(1) & S. 10(2A). Thus, a person who is supplying goods through ECO would now be eligible to opt for composition scheme.

2. Non-Payment of Invoice value to supplier, Input Tax Credit shall be paid instead of addition in output tax liability [Clause 129 of Finance Bill]:

When a recipient is unable to pay to its supplier within 180 days from invoice date, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability paid by him, along with interest thereon.

Impact and Analysis:

Earlier, due to wordings “added in output tax liability”, the increased liability can be paid through input tax credit. The new wordings call for payment of input tax credit availed; however, one can take a view that, payment would mean through cash or input tax credit.

3. Amount of Invoice Value shall be payable to Supplier [Clause 129 of Finance Bill]

As per 3rd proviso to Section 16 of CGST Act, the recipient shall be entitled to avail of the credit of input tax on payment made by him to supplier of the amount towards the value of supply of goods or services or both along with tax payable thereon.

Impact and Analysis:

The proposed amendment would not have major impact. However, if recipient discharges the amount to the person whom supplier is liable to pay would be the matter of discussion. For Example, “A” is the recipient; “B” is the supplier; C is the supplier of “B”. In the instant case, if A discharges liability amount to Mr. C on instruction of “A” would amount to non-payment.

4. Insertion of exclusions in Exempt Supply for the purpose of reversal of Input Tax Credit [Clause 130 of Finance Bill]

As per section 17(3) of CGST Act, as per explanation provided therein, for purposes of this sub-section, the expression ‘‘value of exempt supply’’ shall not include the value of activities or transactions specified in Schedule III, except those specified in paragraph 5 of the said Schedule.

(i) the value of activities or transactions specified in paragraph 5 of the said Schedule; and

(ii) the value of such activities or transactions as may be prescribed in respect of clause (a) of paragraph 8 of the said Schedule.

Impact and Analysis:

As per Para 8(a) of Schedule III of CGST Act, sale of warehoused goods to any person before clearance for home consumption are not supply under GST. However, the said sale shall be included for the purpose of input tax credit reversal u/r 42 & Rule 43 of CGST Rules.

5. No Input Tax Credit of CSR Expenditure [Clause 130 of Finance Bill]

As per proposed amendment, input tax credit shall not be available in respect of goods or services or both received by a taxable person, which are used or intended to be used for activities relating to his obligations under corporate social responsibility referred to in section 135 of the Companies Act, 2013.

Impact and Analysis:

As per section 16 of CGST Act, 2017, input tax credit incurred for furtherance of business would be allowed. furtherance of business would imply advancement or promotion of business. Any activity carried on with a purpose to achieve business objectives, business continuity and stability would per se amount to an activity in course or furtherance of business.

The Hon’ble CESTAT Mumbai, in the case of Essel Propack Limited vs Commissioner of CGST states that “CSR is not only a holistic approach but it has integrated the core business strategy since it addresses the wellbeing of all stake holders and not just companies’ shareholders. It enhances the reputation of company, its goodwill by creating a positive image and branding benefits that continue to exist for companies who operate CSR programmes.” The essence of the above discussion would indicate that CSR is not a charity any more since it has got a direct bearing on the manufacturing activity of the company.

Thus, all the ambiguities are now kept at a rest and it has been decided to amend section 17(5) of CGST Act so as to disallow the input tax credit of CSR expenditure.

6. Section 23 (Exemption from Registration) shall now override Section 24 as well [Clause 131 of Finance Bill]

As per section 23 of CGST Act, which states, notwithstanding anything to the contrary contained in sub-section (1) of section 22, a person shall not be liable for registration in certain cases. However, now section 23 is non-obstante to section 24 as well.

Impact and Analysis:

This will have major impact on Industries. Let us consider an example of a person who is supplying healthcare services and importing consultancy services. As per section 23 of CGST Act, he was not liable for registration, however, section 24 mandates for compulsory registration as he has imported services (person liable to pay tax under reverse charge).

Earlier, the view was taken that as section 23 overrides only section 22 and not section 24, the said person was unable to take advantage of section 23 as section 24 has mandatorily asked for registration. However, now the said person can be exempt from registration as section 23 is having overriding effect over section 22 & section 24.

7. Filing of GSTR – 1 & GSTR – 3B, GSTR – 9 & GSTR – 8 till 3 years from due date to file such return [Clause 132, 133, 134, 135 of Finance Bill]:

A registered person shall not be allowed to furnish the details of outward supplies under section 37(1), 39(1), 44, 52 for a tax period after the expiry of a period of three years from the due date of furnishing the said details:

However, on the recommendations of the Council, by notification, subject to such conditions and restrictions as may be specified therein, allow a registered person or a class of registered persons to furnish the details of outward supplies for a tax period said sections, even after the expiry of the said period of three years from the due date of furnishing the said details.

Impact and Analysis:

The proposed amendment has set an upper time limit to file GSTR – 1, GSTR – 3B, GSTR – 9 & GSTR – 8 i.e., up to 3 years from due date of filing return. Earlier, only till September of Next financial year, the system was opened, due to which at the time of assessment of recipient, if supplier has not filed its GSTR – 1, recipient has to suffer. As per section 73 of CGST Act, 2017; time limit to complete assessment is 3 years from due date to furnish annual return. In line with the said provision, the tax payer is now allowed to furnish the said return not later than 3 years.

8. Provisional Refund 90% of amount gross amount claimed [Clause 136 of Finance Bill]:

As per section 54(6) of CGST Act, notwithstanding anything contained in sub-section (5), the proper officer may, in the case of any claim for refund on account of zero-rated supply of goods or services or both made by registered persons, other than such category of registered persons as may be notified by the Government on the recommendations of the Council, refund on a provisional basis, ninety per cent. of the total amount so claimed, excluding the amount of input tax credit provisionally accepted, in such manner and subject to such conditions, limitations and safeguards as may be prescribed and thereafter make an order under sub-section (5) for final settlement of the refund claim after due verification of documents furnished by the applicant.

Impact and Analysis:

The concept of ITC provisionally accepted has been done away with scrapping of section 41, 42, 43. The new section 41 provides that the taxpayer shall self-assess and claim ITC in GSTR 3B. It further provides that in case the taxpayer has claimed ITC of GST which is not paid/ deposited by the corresponding supplier, than the taxpayer / recipient shall reverse the ITC along with interest. Section 54 has been aligned with the said amendment.

9. Changes in Wordings of Section 56 of CGST Act (Interest on Delayed Refunds) [Clause 137 of Finance Bill]

As per section 56 of CGST Act, if any tax ordered to be refunded under section 54(5) to any applicant is not refunded within sixty days from the date of receipt of application under section 54(1) of that section, interest at such rate not exceeding six per cent. as may be specified in the notification issued by the Government on the recommendations of the Council shall be payable in respect of such refund from the date immediately after the expiry of sixty days from the date of receipt of application under the said sub-section till the date of refund of such tax for the period of delay beyond sixty days from the date of receipt of such application till the date of refund of such tax, to be computed in such manner and subject to such conditions and restrictions as may be prescribed.

10. Insertion of Section 122(1B) – E – Commerce Operators [Clause 138 of Finance Bill]:

Any electronic commerce operator who –

(i) allows a supply of goods or services or both through it by an unregistered person other than a person exempted from registration by a notification issued under this Act to make such supply;

Analysis:

As per section 24 of CGST Act, any person supplying goods through ECO shall be liable for compulsory registration under GST. Further, a supplier of services shall be liable to be registered if his turnover exceeds Rs. 10 lakhs or 20 lakhs.

(ii) allows an inter-State supply of goods or services or both through it by a person who is not eligible to make such inter-State supply; or

Analysis:

As per section 24 of CGST Act, interstate supplier of exempt goods is not liable for registration, thus, he can supply inter-state without any hindrance of this section.

(iii) fails to furnish the correct details in the statement to be furnished under sub-section (4) of section 52 of any outward supply of goods effected through it by a person exempted from obtaining registration under this Act, shall be liable to pay a penalty of

♦ Ten thousand rupees, or

♦ An amount equivalent to the amount of tax involved had such supply been made by a registered person other than a person paying tax under section 10, whichever is higher.

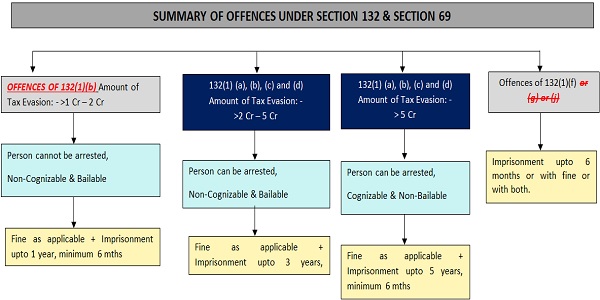

11. Amendment in provisions relating offences u/s 132 [Clause 139 of Finance Bill]

As per Section 132(1) the person who commits, or CAUSES TO COMMIT AND RETAIN THE BENEFITS arising out of, any of the following offences shall be punishable: –

(a) Supplies without issue of any invoice with the intention to evade tax;

(b) Issues any invoice or bill without supply leading to wrongful availment or utilisation of input tax credit or refund of tax;

(c) Avails input tax credit using the invoice or bill referred to in clause (b) or fraudulently avails input tax credit without any invoice or bill.

(d) Collects any amount as tax but fails to pay the same to the Government beyond a period of 3 months from the date on which such payment becomes due. [S. 132(1)(d)].

(e) Evades tax or fraudulently obtains refund and where such offence is not covered under clauses (a) to (d);

(f) Falsifies or substitutes financial records or produces fake accounts or documents or furnishes any false information with an intention to evade payment of tax due under this Act;

(g) Obstructs or prevents any officer in the discharge of his duties

(h) Acquires possession of, or in any way concerns himself in transporting, removing, depositing, keeping, concealing, supplying, or purchasing or in any other manner deals with, any goods which he knows or has reasons to believe are liable to confiscation

(i) Receives or is in any way concerned with the supply of, or in any other manner deals with any supply of services which he knows or has reasons to believe are in contravention of any provisions of this Act or the rules made thereunder;

(j) Tampers with or destroys any material evidence or documents;

(k) Fails to supply any information or (unless with a reasonable belief, the burden of proving which shall be upon him, that the information supplied by him is true) supplies false information

(i) Attempts to commit, or abets the commission of any of the offences mentioned in clauses (a) to (k) clauses (a) to (f) and clauses (h) and (i) of this section,

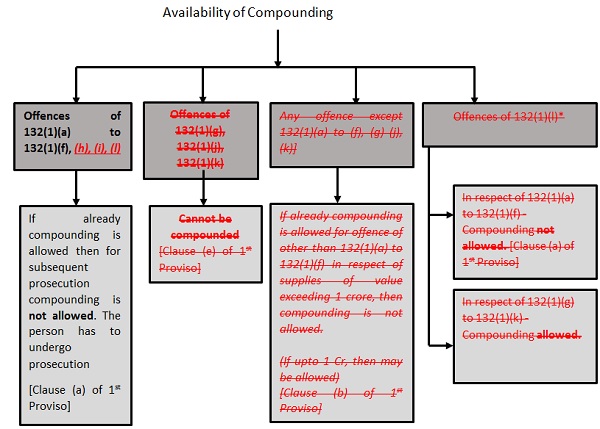

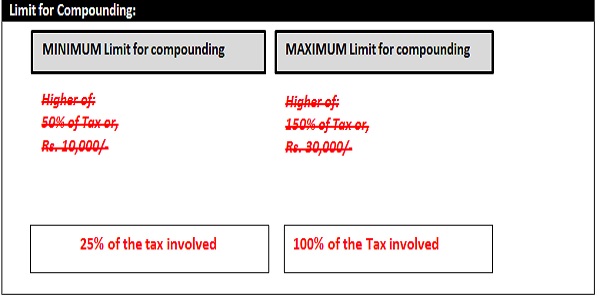

12. Amendments in Compounding of Offences [Clause 140 of Finance Bill]

|

Other cases where compounding is not allowed |

| A person who has been accused of committing an offence under clause (b) of sub-section (1) of section 132 [Clause (c) of 1st Proviso] |

| A person who has been convicted for an offence under this Act by a court [Clause (d) of 1st Proviso] |

| Any other class of persons or offences as may be prescribed [Clause (f) of 1st Proviso] |

13. Consent Based Sharing of Information [Clause 141 of Finance Bill]

As per proposed Section 158A.

(1) Notwithstanding anything contained in sections 133, 152 and 158, the following details furnished by a registered person may, subject to the provisions of subsection (2) and on the recommendations of the Council, be shared by the common portal with such other systems as may be notified by the Government, in such manner and subject to such conditions as may be prescribed, namely: –

(a) particulars furnished in the application for registration under section 25 or in the return filed under section 39 or under section 44;

(b) the particulars uploaded on the common portal for preparation of invoice, the details of outward supplies furnished under section 37 and the particulars uploaded on the common portal for generation of documents under section 68

(c) such other details as may be prescribed.

(2) For the purposes of sharing details under sub-section (1), the consent shall be obtained, of

(a) the supplier, in respect of details furnished under clauses (a), (b) and (c) of sub-section (1); and

(b) the recipient, in respect of details furnished under clause (b) of sub-section (1), and under clause (c) of sub-section (1) only where such details include identity information of the recipient, in such form and manner as may be prescribed.

(3) Notwithstanding anything contained in any law for the time being in force, no action shall lie against the Government or the common portal with respect to any liability arising consequent to information shared under this section and there shall be no impact on the liability to pay tax on the relevant supply or as per the relevant return.”

14. Retrospective exemption to certain activities and transactions in Schedule III [Section 142 of Finance Bill]

In Schedule III to the CGST Act, paragraphs 7 and 8 and the Explanation 2 thereof (as inserted vide section 32 of Act 31 of 2018) shall be deemed to have been inserted therein with effect from the 1st day of July, 2017. It is to be noted that refund shall be made of all the tax which has been collected, but which would not have been so collected, had subsection (1) been in force at all material times.

15. Change in Definition of Non – Taxable online recipient [Clause 143 of Finance Bill]:

The new definition of non-taxable online recipient would read as, “non-taxable online recipient” means any unregistered person receiving online information and database access or retrieval services located in taxable territory.

Explanation: For the purposes of this clause, the expression “unregistered person” includes a person registered solely in terms of clause (vi) of section 24 of the Central Goods and Services Tax Act, 2017’.

Impact & Analysis:

♦ The definition removes the Government, local authority, governmental authority from the ambit of NTOR.

♦ Earlier any unregistered person taking OIDAR services for other than business purpose was covered, however, now all unregistered persons are covered in definition of NTOR.

♦ As per NN 10/2017 – Integrated Tax Rate, import of services by other than NTOR is taxable under reverse charge mechanism. Thus, unregistered business entities importing OIDAR services would no more be compulsorily liable for registration to pay tax under reverse charge.

16. Change in Definition of OIDAR services:

“Online information and database access or retrieval services” means services whose delivery is mediated by information technology over the internet or an electronic network and the nature of which renders their supply essentially automated and involving minimal human intervention and impossible to ensure in the absence of information technology and includes electronic services such as,

(i) advertising on the internet;

(ii) providing cloud services;

(iii) provision of e-books, movie, music, software and other intangibles through telecommunication networks or internet;

(iv) providing data or information, retrievable or otherwise, to any person in electronic form through a computer network;

(v) online supplies of digital content (movies, television shows, music, and the like);

(vi) digital data storage; and

(viii) online gaming;

17. Removal of Proviso to Section 12(8) of IGST Act [Clause 144 of Finance Bill]:

As per proviso to section 12(8) of IGST Act, where the location of supplier and recipient is in India, and destination of goods is outside India, the place of supply of goods transportation services would be outside India. The said provision was made without giving any thought to benefit the industry. Since, it would not be treated as export because supplier is in India and is not receiving foreign exchange. Further, the same was not even taxable as Place of supply was outside India.

The said proviso caused many hardships in interpretation of law, accordingly, it is hereby proposed to remove the said proviso.

OTHER UPDATES ON INDIRECT TAXES

REDUCTION IN CUSTOM DUTY:

Reduced the number of basic customs duty rates on goods, other than textiles and agriculture, from 21% to 13%. Basic Customs Duty on Kitchen, Chimney Increased from 7.5% to 15% and that on heat coils reduced from 20% to 15%.

In the last financial year, marine products recorded the highest export growth benefitting farmers in the coastal states of the country. To enhance the export competitiveness of marine products, particularly shrimps, duty is being reduced on key inputs for domestic manufacture of shrimp feed.

India is a global leader in cutting and polishing of natural diamonds, contributing about three-fourths of the global turnover by value. Finance Minister proposed to reduce basic customs duty on seeds used in their manufacture.

Some of the other key reductions are:

The basic customs duty on crude, glycerine is proposed to be reduced to 2.5%. Extend customs duty cut on imports of parts of mobile phones by 1 year.

Reduction of customs duty on open cells of TV panels to 2.5%.

INCREASE IN CUSTOM DUTY:

The basic customs duty rate on compounded rubber is being increased from 10 per cent to 25 per cent or 30/kg whichever is lower’, at par with that on natural rubber other than latex, to curb circumvention of duty.

National Calamity Contingent Duty (NCCD) on specified cigarettes was last revised three years ago. This is proposed to be revised upwards by about 16 per cent. The import duty on silver bars is to be increased to align it with gold, platinum.