Fraudsters and Defaulters Beware! Tax Authorities and Intelligent System Watching You

The government is increasingly looking to check evasion and plug revenue leakages as it’s falling short of its tax collections estimated in the budget. With searches carried out recently in different parts of the country, the directorate general of GST intelligence (DGGSTI) has unearthed cases of fake invoices worth over Rs 10,000 crore in the current fiscal. Scams like issuing fake GST invoices without actual supply of goods for availment of fraudulent input tax credit and also scams like creating fake companies and obtaining fake GST Registration with an aim to pass on Input Tax Credit, Circular Trading, Fraudulent Export & Inverted Tax Refunds etc have mainly come to light. Cases of mismatch over Rs 40 crore are now handed over to the DGGSTI which is a specialized investigation wing whose officers have all India jurisdiction. The rest of the cases will be taken up by the respective Commissionerate’s.

The DGGSTI is now taking up the job to sensitize the income tax department and even banks about such cases. Around 5,000 companies have come under the scanner of tax authorities due to alleged discrepancies between their Goods and Services Tax (GST) filings and Income Tax (I-T) returns. The companies are said to have claimed input tax credit through dummy companies. In their GST filings, they showed transactions between companies that were either unrelated or had no business history. Around 2,000 cases of mismatches have been found in Mumbai alone, followed by Delhi, Kolkata, Hyderabad and Bengaluru. The discrepancies were found after comparing other data as well, such as gross total income, turnover ratio and sales returns provided by GSTN and other sources. Scrutiny notices were sent to some companies for utilising input tax credit to clear the bulk of the GST liabilities. GST authorities started process of blocking input tax credit of about 1,000 taxpayers who have allegedly claimed more credit than they were eligible for.

The Central Board of Indirect Taxes and Customs has asked every Commissionerate to identify top 20 taxpayers who have the highest discrepancy in input tax credit based on the purchase-related GSTR-2A and summary GSTR-3B returns. GSTR 2A is automatically generated for each business on the GST portal, while taxpayers every month file GSTR-3B that also discloses the credit availed. Accordingly, actions are already initiated by all Commissionerate’s to block the input credit for the top 20 taxpayers showing a mismatch between the two returns.

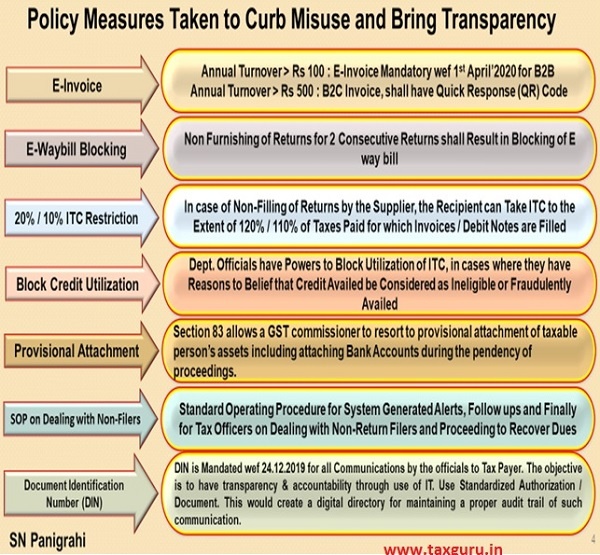

- 1. Policy Measures take in recent times as follows are expected to curb misuse and brings transparency.

- i. E-Invoice

- ii. E-Waybill Blocking

- iii. 20% / 10% ITC Restriction

- iv. Powers of Officials to block credit under Rule 86A

- v. Provisional Attachment

- vi. SOP for Tax Officers on Dealing with Non-Return Filers

- vii. Interception, Inspection, Verification and Detention of Goods in Transit

- viii. No Anticipatory Bail – GST Violators can be Arrested without FIR : SC

- ix. Generation and Quoting of Document Identification Number (DIN)

- 2. Harmonized and standardized the Formats

- 3. Constitution of Grievance Redressal Committees on GST related issues

- 4. AI, Data Analytics to Track GST Evaders, Boost Compliance

- 5. Centre, States Frame Strategy to End GST Woes

Page Contents

- 1. Policy Measures take in recent times as follows are expected to curb misuse and brings transparency.

- i. E-Invoice

- ii. E-Waybill Blocking

- iii. 20% / 10% ITC Restriction

- iv. Powers of Officials to block credit under Rule 86A

- v. Provisional Attachment

- vi. SOP for Tax Officers on Dealing with Non-Return Filers

- vii. Interception, Inspection, Verification and Detention of Goods in Transit

- viii. No Anticipatory Bail – GST Violators can be Arrested without FIR : SC

- ix. Generation and Quoting of Document Identification Number (DIN)

- 2. Harmonized and standardized the Formats

- 3. Constitution of Grievance Redressal Committees on GST related issues

- 4. AI, Data Analytics to Track GST Evaders, Boost Compliance

- 5. Centre, States Frame Strategy to End GST Woes

1. Policy Measures take in recent times as follows are expected to curb misuse and brings transparency.

i. E-Invoice

A system of directly issuing invoices through the GST-network (GSTN) is being worked out. With this, the sale and purchase invoices of a business having a turnover above a certain limit may have to be directly generated through the system. This will ensure easier matching of the purchases and sales of the opposite parties.

ii. E-Waybill Blocking

The government has introduced an important change around the e-way bill generation with an aim to crack down on GST non-filers and evaders. With effect from December 1st, 2019, the blocking and unblocking of the e-way bill generation facility has been implemented on the e-way bill portal. E-way bill generation has been barred for taxpayers who haven’t filed their returns for the previous two consecutive periods.

iii. 20% / 10% ITC Restriction

The government has capped the ITC that a registered person can claim, unless the entire eligible amount is backed by relevant invoices or debit notes. Sub-rule (4) to Rule 36 restricting input tax credit (“ITC”) has been inserted with effect from 09.10.2019 vide Notification No. 49/2019 – Central Tax dt. 09.10.2019. Said sub-rule reads as under:

“(4) Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37, shall not exceed 20 per cent of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub-section (1) of section 37.”

Circular No. 123/42/2019– GST; 11th November, 2019 has been issued to clarify the new provision. Further the 20% cap was reduced to 10% vide Notification No. 75/2019 – CT dt.26.12.19 if invoices or debit notes are not reflected in GSTR-2A.

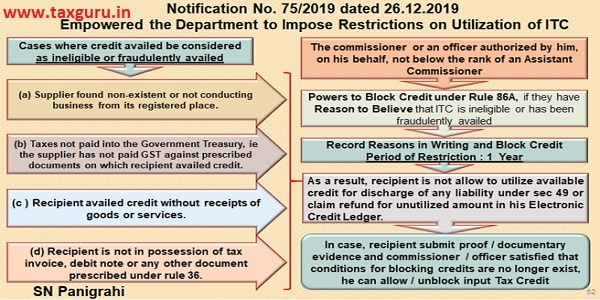

iv. Powers of Officials to block credit under Rule 86A

Blocking Utilization of Tax Credits if credits are ineligible or fraudulently availed

Government vide Notification No. 75/2019 dated 26.12.2019 inserted Rule 86A indicating conditions of use of amount available in Electronic Credit Ledger. Department officials now have authority to block the utilization of tax credits if the registered person has availed credit which are ineligible or fraudulently availed. The rationale of blocking the credit is clearly to plug cases of fake credits.

v. Provisional Attachment

Section 83 of CGST Act, allows a GST commissioner to resort to provisional attachment of taxable person’s assets during the pendency of proceedings in instances like:

> Failure of a registered person to furnish periodic returns or obtaining registration under the GST Act despite falling within the prescribed registration thresholds.

> Default in paying tax after cancellation of registration.

> Suppression of transactions in supply of goods or services.

> Fraudulent or excess availment of input tax credit with an intent to evade tax or gain undue advantage.

Coercive steps like blocking input credit of taxpayers are being taken by the departmental officials on the pretext of valid reasons to suspect fraud or tax evasion, despite the Bombay High Court’s judgment in case of Kaish Impex that has quashed the order to attach bank accounts, saying Attach Bank Accounts Sparingly.

> Under the CGST Act, a tax officer must frame an opinion before exercising powers of provisional attachment.

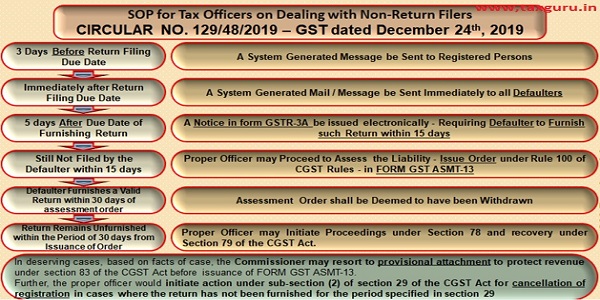

vi. SOP for Tax Officers on Dealing with Non-Return Filers

The tax officers have been following divergent practices when it comes to the appropriate procedure to be followed in case of non-furnishing of returns by a registered person (“defaulter”) under section 39 or 44 or 45 of the Central Goods and Services Tax Act, 2017. The CBIC vide CIRCULAR NO. 129/48/2019 – GST dated December 24th, 2019 has provided the following guidelines as under to ensure uniformity in implementation of provisions of law across field formations.

vii. Interception, Inspection, Verification and Detention of Goods in Transit

When the goods are in movement, a proper officer may intercept or inspect any vehicle that is carrying goods. A vehicle may be intercepted either for verification of documents or inspection of goods. He shall verify all the documents that the transporter is carrying including an E-way bill, invoice etc

Trade is Warned to be extra careful about Required Documents to Accompany Movement of Goods. Department Officials are very Vigilant these Days (Specially this being Last Quarter) to Recover Revenue Deficit.

Moreover, Traditional Business Habits (Like Month End Billings without Movement of Goods, Current E-Waybill with Corresponding Invoice of Very Old Date, Movement of Goods without Proper Documents, Multiple Trips of Goods Delivery with Same Documents etc… etc…) need to Change to become Compliant with Law, otherwise should be prepared to face severe consequences.

viii. No Anticipatory Bail – GST Violators can be Arrested without FIR : SC

Goods and Services Tax (GST) defaulters may face arrest as the Supreme Court suggested to high courts not to grant anticipatory bail in such cases.

The apex court reminded them that it had upheld a Telangana high court decision not to grant bail to such defaulters. A division bench of the Telangana HC had on April 18 upheld the authority and power of the Commissioner of Central Goods and Services Tax (CGST) to arrest, and rejected any interim relief to people who were accused of violating the CGST Act, 2017.

The SC, on May 27, had dismissed an appeal against the Telangana HC order. The Centre had argued that CGST officers were not police and hence not required to follow the provisions of Criminal Procedure Code, which mandates filing of FIR prior to arrest.

Explaining the procedure under CGST Act, the Centre in its appeal said the law terms GST violations as a cognisable offence and provides power to the GST commissioner to arrest a person on the basis of “reasons to believe” that a person has committed the offence under Section 132 of the CGST Act

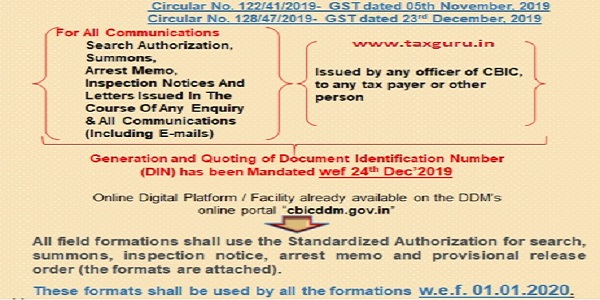

ix. Generation and Quoting of Document Identification Number (DIN)

Use of CBIC-DIN was made compulsory from 24th Dec’2019 vide Circular No. 122/41/2019- GST dated 05th November, 2019 & Circular No. 128/47/2019- GST dated 23rd December, 2019, and no communication without bearing the DIN generated from the system will be valid.

Following are the cases for which the DIN has been mandated now:

- search authorization,

- summons,

- arrest memo,

- inspection notices and

- letters issued in the course of any enquiry

by any officer of CBIC, to any tax payer or other person

The objective is to have transparency and accountability in indirect tax administration through widespread use of information technology. This would create a digital directory for maintaining a proper audit trail of such communication. Further, it would also provide the recipients of such communication a digital facility to ascertain their genuineness.

The online digital platform / facility already available on the DDM’s online portal “cbicddm.gov.in” for electronic generation of DIN has been suitably enhanced to enable electronic generation of DIN in respect of all forms of communication (including e-mails) sent to tax payers and other concerned persons.

2. Harmonized and standardized the Formats

The Board also felt it necessary to harmonize and standardize the formats of search authorizations, summons, arrest memos, inspection notices etc. issued by the GST/ Central Excise / Service Tax formations across the country.

The standardized documents have since been uploaded by DDM and are ready to be used. When downloaded and printed, these standardized documents would bear a pre-populated DIN thereon. Accordingly, the Board directs that all field formations shall use the standardized authorization for search, summons, inspection notice, arrest memo and provisional release order (the formats are attached). These formats shall be used by all the formations w.e.f. 01.01.2020

GST Council in its 38th meeting held on 18.12.2019 has decided that a structured grievance redressal mechanism should be established for the taxpayers under GST to tackle grievances of taxpayers on GST related issues of specific/ general nature. GST Council has accordingly approved constitution of ‘Grievance Redressal Committee’ at Zonal / State level consisting of both Central Tax and State Tax officers, representatives of trade and industry and other GST stakeholders. Vide F. No. 20/10/16/2018-GST (Pt. I); Dated 24th December, 2019, guidelines for Constitution of the Committee, Functions and Mandate of the Committee, Periodicity of Meeting of the Committee, Mechanism of Working of the Committee are circulated and accordingly committees are being formed.

4. AI, Data Analytics to Track GST Evaders, Boost Compliance

The government plans to increase the use of artificial intelligence and data analytics to track down tax evaders, and improve compliance with the Goods and Service Tax in order to augment revenue and to streamline the GST system and plug leakages due to fraud. Government notified various changes to GST rules to prevent frauds and fake invoicing, besides setting up grievance cells to ensure that genuine taxpayers are not harassed and the overall tax base increases.

Government is deliberating on a mechanism and machinery for disseminating inter-departmental data among various agencies, including the GSTC, CBDT, CBIC, FIU, DoR, DGGI and State Tax Administrations, in order to achieve efficiency in curbing evasion and augment revenue collection.

5. Centre, States Frame Strategy to End GST Woes

The Centre and States have joined hands to formulate a nine-point strategy to streamline the Goods & Services Tax (GST) and plug revenue leakage. These include linking foreign exchange remittances with IGST refund for risky and new exporters, investigation of fraudulent ITC cases by the IT department, a single bank account for foreign remittance receipt, and refund disbursement, beside others.

It was also decided to constitute a Committee of Centre and State officers to examine and implement quick measures in a given time frame to curb fraudulent refund claims, including the inverted tax structure refund claims, and GST evasion. The Committee will come out with a detailed SoP (Standard Operating Procedure), which may be implemented across the country.

All major cases of fake Input Tax Credit, export/ import fraud and fraudulent refunds will also be compulsorily investigated by the investigation wing of the Income Tax Department.

Access to banking transactions, including bank account details by the GST system, in consultation with RBI and NPCI, was also explored. Aligning the GST system with the FIU (Financial Intelligence Unit) for the purpose of getting bank account details and transactions and PAN-based banking transactions, was also considered.

Sharing data of cases involving evasion, and fraudulent refund detected by CBIC with CBDT and vice-versa, so that fraudsters could be properly profiled was also taken up.

A self-assessment declaration will be prescribed with suitable amendments in GSTR Forms in case of closure of businesses. The Centre and states have agreed to undertake verification of unmatched Input Tax Credit availed by taxpayers.

And a lot many measures are being explored with the help of Advanced IT and Artificial Intelligence (AI).

Though these Restrictive and Corrective measures are being taken affect the Genuine Tax Payers, these are welcome to clean up the System and make the tax payers compliant with law.

So, Fraudsters and Defaulters Beware! Tax Authorities & Intelligent System Watching You.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST & Foreign Trade Consultant, Practitioner, International Corporate Trainer & Author. Author is Available for Corporate Trainings & Consultancy and Can be reached @ snpanigrahi1963@gmail.com