A. FAQs > Filing an Appeal against Demand Order (FORM GST APL-01)

Q.1 Who can file an appeal to the Appellate Authority?

Ans. Any taxpayer or an unregistered person aggrieved by any decision or order passed against him by an adjudicating authority, may appeal to the Appellate Authority, within three months from the date on which the said decision or order is communicated to such person.

Q.2 What are the pre-conditions to file an appeal to the Appellate Authority?

Ans. Order must be passed by the adjudicating authority for the taxpayer or an unregistered person to file an appeal to the Appellate Authority.

Q.3 From where can I file an appeal against Demand Order?

Ans. Navigate to Services > User Services > My Applications > Application Type as Appeal to Appellate Authority > NEW APPLICATION button. Select the Order Type as Demand Order from the drop-down list.

Q.4 What are the various Appeal statuses?

Ans.

| S.No. | Description | Status |

| 1 | Appeal Form successfully filed | Appeal Submitted |

| 2 | Appeal Form successfully admitted | Appeal admitted |

| 3 | Appeal Form is Rejected | Appeal Rejected |

| 4 | When Hearing Notice is issued | Hearing Notice issued |

| 5 | When Counter Reply received against notice | Counter reply received |

| 6 | When Show cause notice is issued | Show cause notice issued |

| 7 | Appeal is confirmed/modified/rejected | Appeal order passed |

| 8 | When hearing is adjourned and next date is issued | Adjournment granted |

| 9 | When application is filed for Rectification | Rectification request received |

| 10 | When application for Rectification is rejected | Rectification request rejected |

| 11 | Appeal is order is rectified | Rectification order passed |

Q.5 From where can I view submitted appeal against Demand Order?

Ans. Navigate to Services > User Services > My Applications > Application Type as Appeal to Appellate Authority > From and To Date > SEARCH button.

Q.6 What will happen if do not file appeal within the prescribed period?

Ans. The appellate authority may condone delay for a period of maximum of 1 month, if he is satisfied that the taxpayer was prevented by sufficient cause from presenting the appeal within the aforesaid period of three months and allow it to be presented within a period of one month after the expiry date of filing appeal.

Q.7 When will I get final acknowledgment of the appeal filed?

Ans. Once an appeal against a demand order is filed, an email and SMS is sent to the taxpayer (or an unregistered person, as the case may be) and Appellate Authority.

However, final acknowledgement of the appeal filed is issued, when after electronic filing of appeal, the documents as well as Appeal with verification part is submitted to the Appellate authority, within 7 days from the electronic filing. Thereafter the appeal documents are checked and if found in order, final acknowledgment is issued. The appeal shall be treated to be filed only when the final acknowledgement, indicating the appeal number is issued.

Q.8 Is it necessary to deposit 10% of the disputed tax?

Ans. Minimum of 10% of the disputed tax needs to be paid as pre-deposit (as per law) before filing an appeal. Lower percentage may be declared after approval from the competent authorities.

Q.9 Is it necessary for me to have a DSC for filing the appeal?

Ans. You can file the appeal either through DSC or EVC. DSC is mandatory for companies and LLPs.

Q.10 Whether the balance disputed amount is stayed on filing Appeal?

Ans. Yes, if Appeal filed is admitted, the GST Portal flags the balance disputed amount as non-recoverable.

Q.11 Is it required to provide place of supply wise details for filing the appeal?

Ans. If a taxpayer has admitted any amount related to IGST head, then place of supply is required to be mentioned in the Appeal application. You can add place of supply details for more than one State.

- B. Manual on Filing an Appeal against Demand Order / How do I file an appeal against a Demand Order?

- A. Creating Appeal to Appellate Authority

- B. Upload Annexure to GST APL-01

- C. Disputed Amount/ Payment Details

- D. Pre-deposit % of disputed tax

- E. Utilize Cash/ ITC

- F. Add any Other Supporting Document

- G. Preview the Application and Proceed to File

Page Contents

- B. Manual on Filing an Appeal against Demand Order / How do I file an appeal against a Demand Order?

- A. Creating Appeal to Appellate Authority

- B. Upload Annexure to GST APL-01

- C. Disputed Amount/ Payment Details

- D. Pre-deposit % of disputed tax

- E. Utilize Cash/ ITC

- F. Add any Other Supporting Document

- G. Preview the Application and Proceed to File

B. Manual on Filing an Appeal against Demand Order / How do I file an appeal against a Demand Order?

To file an appeal against a demand order, perform following steps:

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the GST Portal with valid credentials i.e. your User Id and Password.

Steps to file appeal appeal against a Demand Order

1. Creating Appeal to Appellate Authority

2. Upload Annexure to GST APL-01

3. Disputed Amount/ Payment Details

4. Pre-deposit % of disputed tax

5. Utilize Cash/ ITC

6. Add any Other Supporting Document

7. Preview the Application and Proceed to File

A. Creating Appeal to Appellate Authority

3. Click the Services> User Services> My Applications

4. The My Applications page is displayed. Select the Application Type as Appeal to Appellate Authority from the drop-down list.

5. Click the NEW APPLICATION

The GST APL-01: Appeal to Appellate Authority page is displayed.

The GST APL-01: Appeal to Appellate Authority page is displayed.

7. In the Order No field, enter the Order Number issued by adjudicating authority.

8. Click the SEARCH button.

9. The Order Details page is displayed.

10. Select the Category of the case under dispute from the drop-down list.

11. Click the ADD button

Note:

1. Date of Communication and Period of Dispute is displayed on the screen. However, you can edit the same.

2. You can add multiple line items from the Category of the case under dispute drop-down list by clicking the ADD button.

3. You can click the DELETE button to delete the details added.

B. Upload Annexure to GST APL-01

12. Click the click here link to download the Annexure to GST APL-01 Template.

13. The GST APL-01 Template is downloaded. Open the downloaded template.

14. Click the Enable Editing button.

15. Enter the details.

16. Once you have entered the details, click on the File button in top left corner.

17. Click the Save As button.

18. Now select the location to save the file and in the File Name list, type or select a name for the document.

19. In the Save as type list, select PDF.

20. Click the Save button.

Note: You should have a PDF reader installed on your computer to open the PDF file.

21. Click the Choose File button to upload the PDF.

Note: You can upload file with maximum size of upload as 5 MB.

22. Select the PDF file which was saved and click the Open button.

23. The PDF file is uploaded. You can click the DELETE button to delete the uploaded PDF file.

C. Disputed Amount/ Payment Details

24. Click the DISPUTED AMOUNT/PAYMENT DETAILS button to enter disputed amount and payment details.

25. The Disputed Amount/ Payment Details page is displayed.

25. The Disputed Amount/ Payment Details page is displayed.

26 (a). In the Amount under Dispute section, enter the amount which is under dispute. Amount under Dispute cannot be more than Amount of Demand Created.

26 (b). Use the scroll bar to view the Total Amount under dispute.

27 (a). Amount of Demand created and admitted is displayed in this section.

27 (b). Use the scroll bar to view the Total Amount of Demand created and admitted.

D. Pre-deposit % of disputed tax

28. Pre-deposit % of disputed tax field will have 10% as default value.

Note: Minimum of 10% of the disputed amount needs to be paid as pre-deposit before filing an appeal. Lower percentage may be declared here after approval from the competent authorities.

Based on the percentage entered, Details of payment required, Details of payment of admitted amount and pre-deposit and Details of amount payable towards admitted amount and pre-deposit sections are auto-populated.

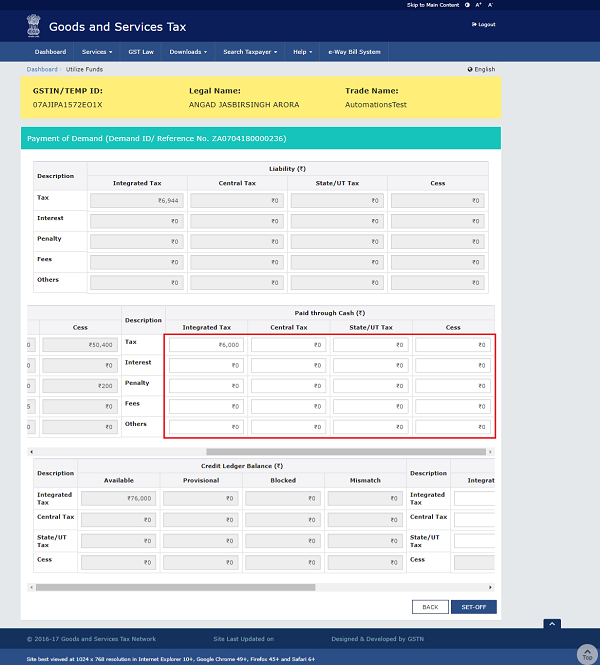

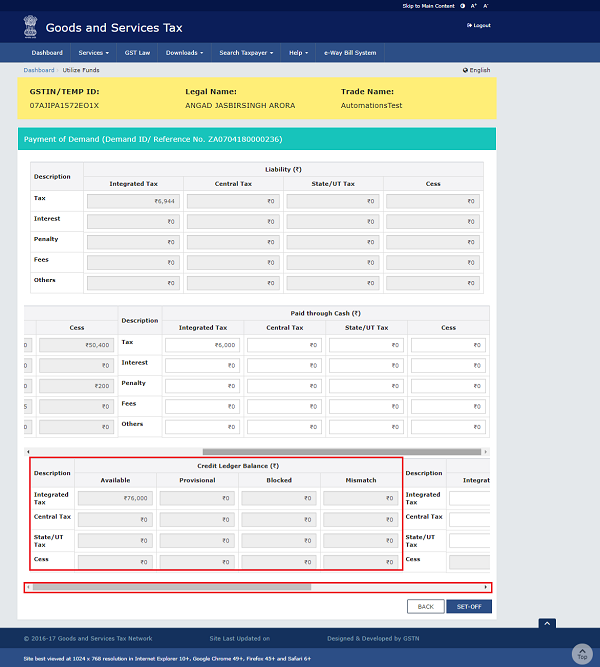

E. Utilize Cash/ ITC

29. Click the UTILIZE ITC/CASH button.

30. Liability, Cash Ledger Balance and Credit Ledger Balance details are displayed.

31 (a) Liability

The liability as on date are shown in below table.

31 (b) Cash Ledger Balance

The cash available as on date are shown in below table.

31 (c) Paid through Cash

Use the scroll bar to move to the right to enter the amount to be paid through cash against that liability.

31 (d) Credit Ledger Balance

The ITC available as on date are shown in below table.

31 (e) Paid through ITC

Use the scroll bar to move to the right to enter the amount to be paid through ITC against that liability.

Note: ITC can be adjusted against Tax liability only.

32. Once you have entered the amount, click the SET-OFF button.

33. A confirmation message is displayed. Click the OK button.

34. A success message is displayed. Payment Reference Number is displayed on the screen. Click the BACK button.

34. A success message is displayed. Payment Reference Number is displayed on the screen. Click the BACK button.

F. Add any Other Supporting Document

35. To upload any other supporting document, enter the document description and click the Choose File button.

Note:

- Only PDF & JPEG file format is allowed.

- Maximum file size for upload is 5MB.

- Maximum 4 supporting documents can be attached in the application. The remaining documents can be handed over in hard copy

36. Select the file to be uploaded and click the Open button.

37. Click the ADD DOCUMENT button to add the uploaded supporting document.

38. The PDF file is uploaded. You can click the DELETE button to delete the uploaded PDF file.

G. Preview the Application and Proceed to File

G. Preview the Application and Proceed to File

39. To preview the Application before filing, Click the PREVIEW button.

40. The PDF file will be downloaded. Open the pdf file and check if all the details are correctly updated.

41. Select the Name of the Authorized Signatory from the drop-down list.

42. Enter the Place where application is filled.

43. Click the PROCEED TO FILE button.

44. Click the PROCEED button.

45. Click the SUBMIT WITH DSC or SUBMIT WITH EVC button.

In case of SUBMIT WITH DSC

a. Select the certificate and click the SIGN button.

In case of SUBMIT WITH EVC

a. Enter the OTP sent on email and mobile number of the Authorized Signatory registered at the GST Portal and click the VERIFY button.

46. A confirmation message is displayed that form has been signed. You can click the DOWNLOAD button to download the acknowledgement receipt.

Once an appeal against a demand order is filed, an email and SMS is sent to the taxpayer (or an unregistered person, as the case may be) and Appellate Authority.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.