FICCI conducted a survey of enterprises on completion of one year of GST implementation, seeking their views on impact of this major reform, besides gauging insights and views on some of the key issues and challenges that were or are being faced by enterprises post implementation of GST.

Key findings of the Survey

Page Contents

- Overall Impact

- Impact on Sales and Profits

- Impact on Employment

- Supply Chain

- Transition to GST

- GSTN Portal

- Compliance Issues

- E-way Bill

- Interaction with GST Authorities

- GST Refund

- Authority for Advance Ruling

- Tariff Rationalization

- Reverse Charge Mechanism

- Other miscellaneous findings

- Key suggestions

- Other suggestions

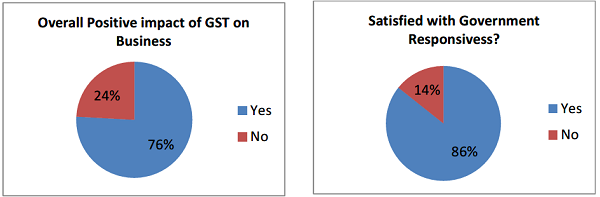

Overall Impact

After one year of the implementation of the Goods and Services Tax, survey findings reveal that most respondents are happy with the implementation of this reform, with 76% respondents stating that GST has a positive impact on their businesses.

Furthermore, the survey reveals that the government has been fairly responsive to suggestions and queries of the industry, with 86% respondents stating that the government has taken adequate steps regarding change in rates and providing clarity on various issues through rules, notifications, issuing FAQs and guidelines.

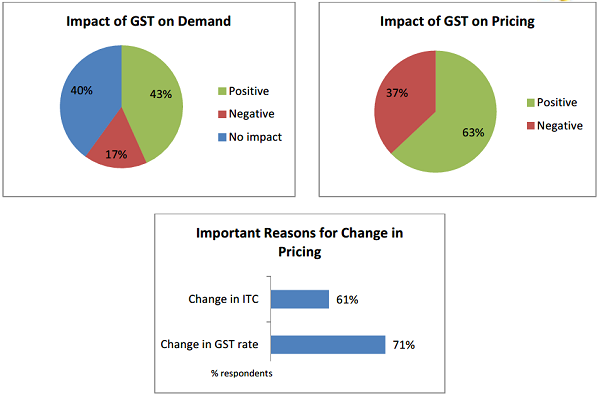

Impact on Sales and Profits

Impact on Sales and Profits

43% respondents to the survey stated that GST had positively impacted the demand for their goods and services. While 40% stated that there was no impact on the demand, only 17% said that the tax had a negative effect on the demand of their products.

In terms of impact on pricing, 63% of the respondents stated that the introduction of GST had impacted pricing positively, while the remaining 37% stated otherwise. The survey shows that the pricing of participating enterprises in the survey has been impacted primarily due to change in GST rate and change in Input Tax Credit, with 71% and 61% respondents respectively stating the same.

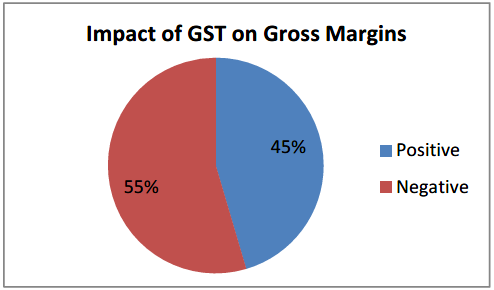

In terms of impact on margins, 55% of survey respondents mentioned that GST implementation has impacted their gross margin negatively, while 45% said that their margins were impacted positively. Out of the respondents citing a negative impact on gross margins, 58% respondents said that the key reason for same was their inability to recover increased tax from the customer.

Impact on Employment

Impact on Employment

64% respondents stated that there was no impact on employment under GST. However, other respondents cited a positive impact on employment and mentioned that their demand for workforce had increased mainly due to the extensive return filing process under GST, reconciliation of inputs in the GST portal, e-way bill generation, etc. While GST opened up accountancy jobs, respondents also said that as margins improved, it enabled companies to focus on operations, encouraging improved recruitments in operations.

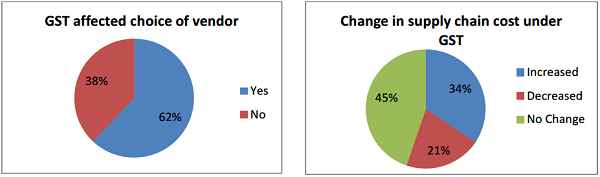

Supply Chain

62% respondents said that GST has affected their choice of vendors or transporters.

In terms of changes in supply chain costs, 21% respondents said that there was a fall in their supply chain cost under GST, while 45% said that there was no change. 34% respondents said that supply chain costs had increased.

Transition to GST

80% respondents to the survey mentioned that transition to GST from the old system of tax was difficult for them, whereas 20% said that it was smooth.

In-fact, 67% respondents found the time for transitioning to be insufficient.

![]()

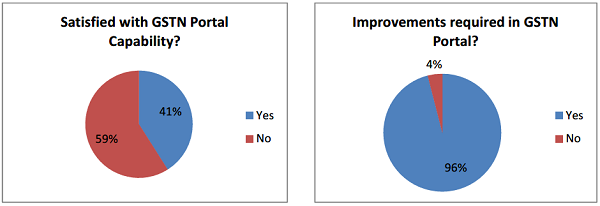

GSTN Portal

59% of the respondents mentioned that they were not satisfied with the capability of the GSTN portal. In fact, 96% respondents felt that improvements were required in the working of the portal.

The following suggestions were made for the improvement of the GSTN Portal:

- Increase bandwidth and server capacity to enable assessees to post data and file returns on the portal on the due date without undue hassles. It has been observed that the system normally collapses on or near the due date of filing the return.

- Respondents suggested that the procedure of filing returns and compliance should be simplified.

- The GSTN portal should be more user-friendly and have an interactive interface, for e.g. 2A report generated by the portal does not give detailed analysis of vendor/invoice wise reconciliation and matching of purchase transactions uploaded in GSTN.

- The Tax Department should circulate guidelines for new updates and new utilities related to the GSTN portal to tax payers for procedural changes in return filing well in advance.

- There is late/incorrect reflection of data on the portal regarding returns filed and tax payments made. Appropriate action should be taken on this account.

- There should be options to make corrections after submission of return in case of errors.

- Grievances raised in the GSTN portal are closed without addressing the issue properly. Steps should be taken to improve the effectiveness of resolving the issues.

- It has been reported that filing of returns through digital signature leads to constant errors. Appropriate measures should be taken to take care of this situation.

- 24 X 7 helpdesk service should be provided.

- Data download is not available from the portal over a certain maximum number of line items; this should be improved.

- A central return mechanism should be introduced for entities with pan-India operations so that return filing is streamlined.

- Payments made to the bank take a lot of time to reflect in the electronic ledger. These need to be made more efficient.

- Issues relating to transitional credit not being credited properly to the electronic ledger should be looked into and addressed.

- Systems should be fully tested before implementation of any change made in any process relating to GST.

- Offline utilities to file return should be improved.

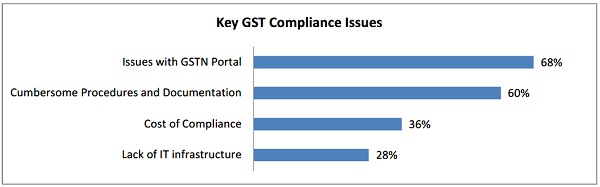

Compliance Issues

The respondents were asked to highlight the key compliance issues they faced under the GST regime. Issues with the GSTN portal remains on the top of concerns of businesses, with 68% of respondents stating the same. 60% respondents mentioned cumbersome procedures and documentation as a key issue, 36% mentioned cost of compliance and 28% mentioned lack of IT infrastructure as key issues.

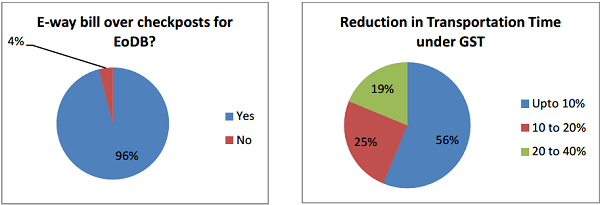

E-way Bill

96% respondents mentioned that as far as ease of doing business is concerned, e-way bill mechanism in lieu of check-post is more effective. 64% respondents to the survey cited a reduction of transportation time under the GST regime. Out of the respondents who cited a reduction in transportation time, 56% respondents cited reduction by up to 10%, 25% respondents stated 10-20% and 19% stated a reduction in transportation time by 20-40%.

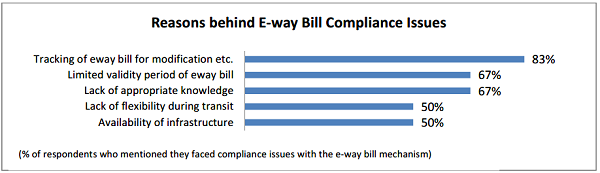

Nevertheless, 24% respondents mentioned that they faced compliance issues with the e-way bill mechanism. Out of such respondents that faced issues, 83% cited tracking of e-way bill for modification as an important reason, 67% each cited limited validity period and lack of appropriate knowledge respectively, and 50% each cited lack of flexibility and availability of infrastructure

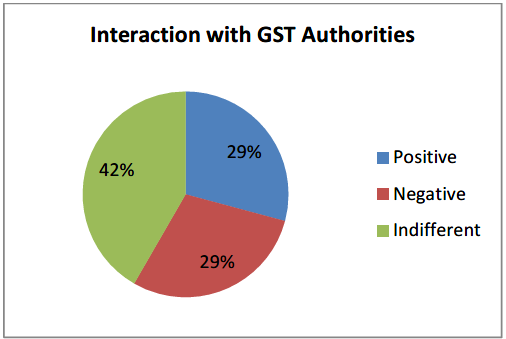

Interaction with GST Authorities

There was a mixed response with respect to respondents’ interaction with GST authorities. 29% of the respondents stated that their experience of interaction with the GST authorities was positive, while an equal number of respondents said that their experience was negative. 42% respondents said that they were indifferent about their experience of interaction with the authorities.

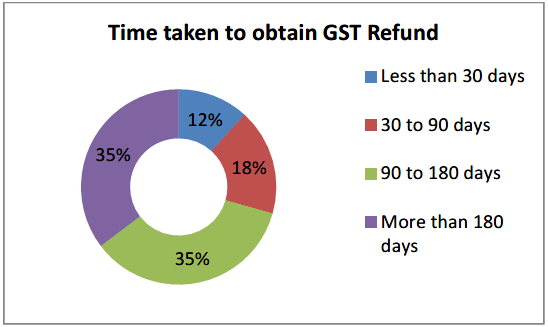

GST Refund

71% respondents mentioned that they faced issues in claiming refund of GST. The important reasons cited were significant efforts in follow up for processing of claims, technical issues in the GSTN portal, mismatch between relevant GSTR and shipping bill leading to the inconvenience in claiming of refunds.

70% respondents mentioned that it took more than 90 days from date of submission of application to obtain GST refund; half of these respondents mentioned that it took more than 180 days. 18% mentioned that it took 30-90 days while 12% stated that it took less than 12 days from the date of submission to obtain the refund.

Authority for Advance Ruling

Amongst suggestions received from the respondents, one suggestion was to overhaul the mechanism of Authority for Advance Ruling (AAR) under the GST regime. AAR should not comprise of revenue officers. To achieve the intended objectives of advance ruling mechanism, an independent high level Central body (similar to the one under the erstwhile indirect tax regime) be constituted as ‘Authority of Advance Ruling’ under the GST regime.

Tariff Rationalization

71% respondents felt that there was a need to reduce tariffs of GST in their sector of business. Respondents suggested tariff rationalization on the following commodities:

- EPC projects pertaining to setting up of Solar Power Generation Plants

- Automobile tyres

- Agricultural implements

- Garments

- Electrical Goods

- Steel

- Alcoholic beverages (to be included under GST)

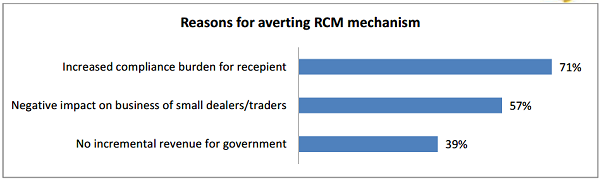

Reverse Charge Mechanism

89% respondents were not in favour of reverse charge mechanism on purchases from unregistered dealers. Of these, 71% respondents stated that it would lead to increased compliance burden for the recipient, 57% stated that it would have a negative impact on business of small dealers and 39% said it would lead to no incremental revenue for the government.

Other miscellaneous findings

Other miscellaneous findings

- 53% respondents felt that the new central incentive scheme in lieu of excise area based exemption is not good enough to compensate the price advantage available prior to July 1, 2017.

- 63% respondents stated that the proposed further changes in return filing process are premature and the authorities should wait till completion of first annual return before implementing any changes in the compliance framework.

- 68% respondents feel that matching of ITC is useful to the taxpayer as it can avoid disputes in future.

Key suggestions

The respondents have identified key areas where the GST law could be made more tax payer friendly. The respondents have also made relevant suggestions towards the same.

Other suggestions

Other suggestions

- It has been observed that the staff at GST Suvidha Kendras are not fully equipped to resolve issues. They should be adequately trained to ensure that the GST Suvidha Kendras become an effective issue resolution mechanism.

- Minimise the number of returns to be filed.

- ITC flow should be seamless and the recipient of goods/services should not be penalized for non-payment of taxes by supplier.

- Rationalise levy of compensation cess.

- Separate documents to be abolished (like generation of invoices for RCMs) and internal documentation mentioned by the assesse should be relied upon.

- Clarifications given by AAR to be made easily available on GSTN portal for easy reference.

- Refund under Budgetary Support Scheme should be allowed on a provisional basis with a CA certificate in order to reduce working capital blockage.

- Shipping bill wise details are not available to assessee for refund received through bank due to which assessees are facing issues in reconciliation. Necessary steps to resolve this issue must be taken.

- Refund on units in fiscal benefit locations and exports with payment of IGST to be fast-tracked and process for the same to be simplified.

- ITC should be allowed on all business expenses without any restrictions. ITC should be allowed on the basis of scanned copy of invoice/documents.

- Refund Procedure including submission of documents should be made online.

- Converge the existing band of GST rates to fewer rates which would reduce complexity and eventually lead to simplification.

- Remove original invoice reference against credit note/debit note. One credit/debit note should be allowed to be issued against multiple original invoices.

- Rationalise rate under GST regime for goods falling under 28% rate category.

- Clarifications should be provided by the government regarding treatment of trade offers under the GST regime.

The bills allowing the Input Tax Credit availability to the Registred dealer are received late. Say for example, tender cost sent by draft, incurring 18% GST.

In order to avoid last minute rush, crashing of GST site, or personal problem, filing of GST return within around 12th of next month is better.

The input tax credit should be allowed to be claimed up to 3 months of the date of the bill.