The process of preparing and filing of annual return in GSTR 9 for FY 2018-19 under GST has started and there have been a number of doubts arising as to how to reconcile the output tax liability under various tables pertaining to the FY 2018-19, because the GSTR 3B filed for 2018-19 contains rectifications for the FY 2017-18 also and there would be certain liability excess/short declared in GSTR 3B filed for 2018-19 which might have been rectified in the GSTR 3B for the period April 2019 to September 2019. These issues have arisen because the GSTR 3B once filed cannot be rectified and any correction if required needs to be done in subsequent returns within the time limit prescribed under Section 39(9) and other relevant provisions as allowed vide Circular No. 26/26/2017-GST, dated 29-12-2017

There may be various types of issues arising in the reconciliation/ its presentation in the GSTR 9, especially because the monthly returns for FY 2018-19 contained rectifications pertaining to FY 2017-18, but there is no table/ column or part for mentioning the same for reconciliation in the GSTR 9 of FY 2018-19. This problem may arise while filing GSTR 9 for subsequent years also if and until the Forms remain unchanged. Let’s discuss issues being faced.

Page Contents

- Q 1. What are the timelines & filing requirements for GSTR 9 & GSTR 9C for FY 2018-19?

- Q 2. How to report Sales for FY 2018-19 reported in GSTR 3B in FY 2018-19 or during April-19 to Sept-19?

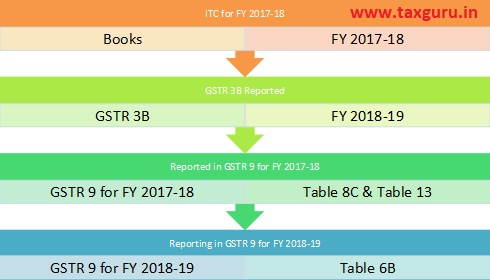

- Q 3. How to report Input Tax Credit (ITC) for FY 2018-19 reported in GSTR 3B in FY 2018-19 or during April-19 to Sept-19?

- Q 4. How to report Input Tax Credit Reversal (ITC Reversal) for FY 2018-2019 reported in GSTR 3B in FY 2018-2019 or during April-2019 to Sept-19?

- Q 5. How to report Sales for FY 2017-2018 reported in GSTR 3B in FY 2018-2019?

- Q 6. How to report Input Tax Credit for FY 2017-2018 reported in GSTR 3B in FY 2018-2019?

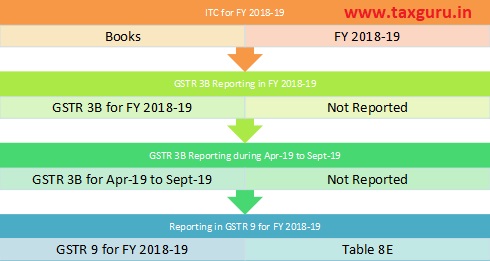

- Q 7. How to report Input Tax Credit for FY 2018-19, but never reported in GSTR 3B till Sept-2019?

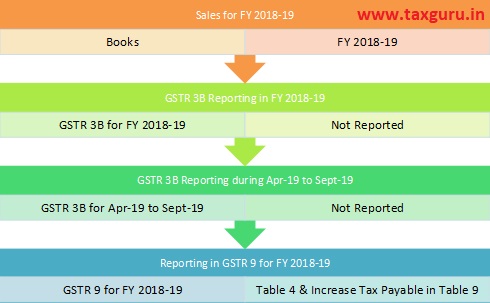

- Q 8. How to report Sales for FY 2018-19, but never reported in GSTR 3B till Sept-2019?

- Q 9. Whether there is auto-population in GSTR 9 of FY 2018-19, relating to figures reported in GSTR 9 for FY 2017-18, relevant to FY 2018-19?

- Q 10. Simplified GSTR 9 form with optional tables applicable for FY 2018-19?

- Q 11. Whether data for GSTR-3B will prevail over GSTR-1 for reporting in GSTR-9?

- Q 12. How to start preparing/ reconciling for GSTR 9 for FY 2018-19?

Q 1. What are the timelines & filing requirements for GSTR 9 & GSTR 9C for FY 2018-19?

Ans:

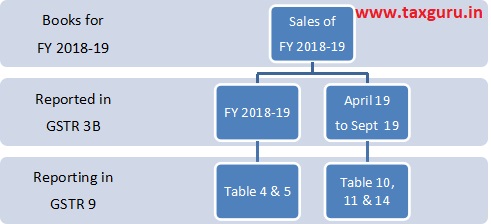

Q 2. How to report Sales for FY 2018-19 reported in GSTR 3B in FY 2018-19 or during April-19 to Sept-19?

Ans:

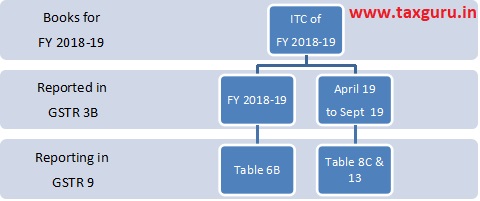

Q 3. How to report Input Tax Credit (ITC) for FY 2018-19 reported in GSTR 3B in FY 2018-19 or during April-19 to Sept-19?

Ans:

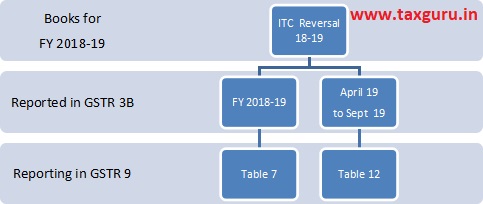

Q 4. How to report Input Tax Credit Reversal (ITC Reversal) for FY 2018-2019 reported in GSTR 3B in FY 2018-2019 or during April-2019 to Sept-19?

Ans:

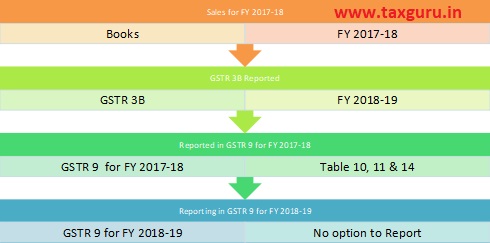

Q 5. How to report Sales for FY 2017-2018 reported in GSTR 3B in FY 2018-2019?

Ans:

Note: No option has been provided in GSTR 9 for FY 2018-19 to report such Sales which belong to FY 2017-18, but reported in GSTR 3B during FY 2018-19. (Table 4 for FY 2018-19 should contain figures of Supplies during FY 2018-19 only.)

Q 6. How to report Input Tax Credit for FY 2017-2018 reported in GSTR 3B in FY 2018-2019?

Ans:

Note: In GSTR 9 for FY 2018-19, there is no option to bifurcate ITC for FY 2017-2018 (availed in GSTR 3B for FY 2018-2019) & ITC for FY 2018-2019 (availed in same year i.e. GSTR 3B for FY 2018-2019)

Q 7. How to report Input Tax Credit for FY 2018-19, but never reported in GSTR 3B till Sept-2019?

Ans:

Note: Such ITC will become Lapse, hence can’t be availed

Q 8. How to report Sales for FY 2018-19, but never reported in GSTR 3B till Sept-2019?

Ans:

Note: File DRC-03 for Additional Tax Liability

Q 9. Whether there is auto-population in GSTR 9 of FY 2018-19, relating to figures reported in GSTR 9 for FY 2017-18, relevant to FY 2018-19?

Ans: No such facility has been provided by government. Table 8C, Table 10 to Table 14 from FY 2017-18, have no auto-population/reporting in GSTR 9 of FY 2018-19

Q 10. Simplified GSTR 9 form with optional tables applicable for FY 2018-19?

Ans: Yes, Simplified GSTR 9 introduced vide notification no.56/2019-CT dated 14/11/2019, to report clubbed/merged figures in few tables (like Table 5D, 5E & 5F – Single merged figure can be reported in Table 5D) and option regarding not to report figures in few of Tables like Table 15 to Table 18, applicable for both FY 2017-18 & FY 2018-19.

Q 11. Whether data for GSTR-3B will prevail over GSTR-1 for reporting in GSTR-9?

Ans: As per clarifications/press release, Irrespective of when the supply was declared in FORM GSTR-1, the principle of declaring a supply in Pt. II or Pt. V is essentially driven by when tax was paid through FORM GSTR-3B in respect of such supplies. Hence for the purpose of Reporting in GSTR 9, data as reported in GSTR 3B will prevail over GSTR 1.

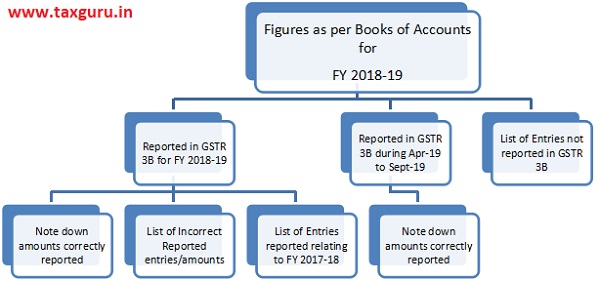

Q 12. How to start preparing/ reconciling for GSTR 9 for FY 2018-19?

Ans: Start with preparing reconciliation in following manner:-

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Article Contributed by: CA. Sagar Gambhir | FCA, DISA (ICAI) | casagargambhir@gmail.com

Author Bio

Show Wrong excess amount in Table 6M “Any other ITC availed but not specified above”

(Not in 6B Breakup)

and reverse the same through DRC 03. (also increase Tax Payable in Table 9)

in 2018-19 wrongly shown purchase( IGST ) as CGST and SGST, ITC EXCESS, HOW CAN I RETURN this input tax and how it show in GSTR9